Not Even Molten Lava Can Cool This Hot Housing Market

The eastern section of Hawaii’s Big Island continues to attract home buyers searching for a cheap piece of paradise

5 min

5 min

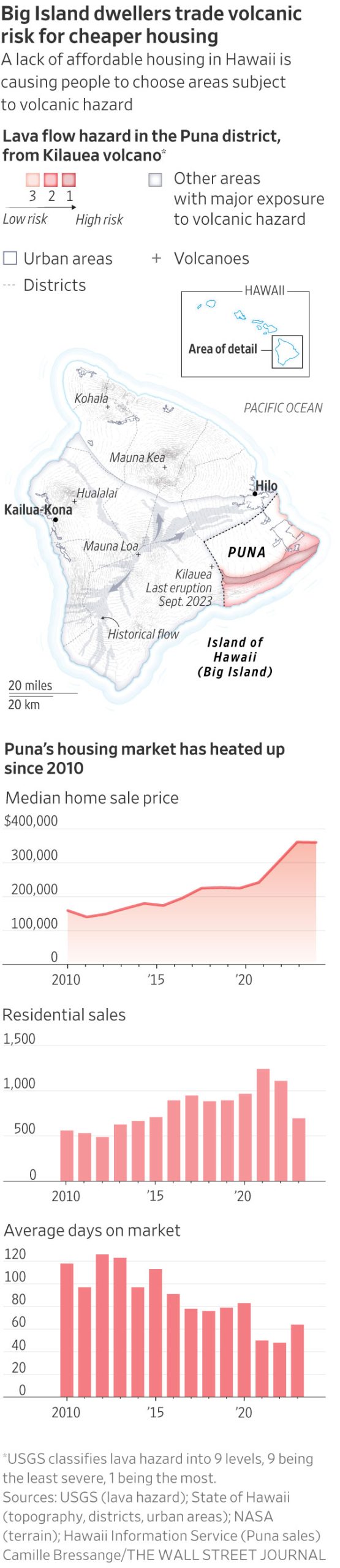

PUNA, Hawaii—In 2018, a large volcanic eruption spewed lava, rock and ash into the middle of a subdivision here, gobbling up more than 700 homes and displacing thousands of residents in a slow-motion disaster. Today, it is Hawaii’s fastest-growing region.

Land in an active lava zone, it turns out, is relatively cheap. Lured by a shot at attainable homeownership in paradise, island dwellers and mainland transplants alike have been flocking to this area in the shadow of Kilauea, driving up prices in the Puna District. Still, the area remains one of the last affordable refuges on the cheapest island in Hawaii, America’s most expensive state.

“In terms of the last bastion of affordability, Puna is it,” said Jared C. Gates, a Realtor who was raised on Oahu and came to the Big Island for college in the 1990s. He purchased his first home in 2005, a modest fixer-upper in Puna, on his salary as a waiter.

Over the past few years, he has been getting more business in Leilani Estates, the neighbourhood where the 2018 eruption began.

None of the homes that were inundated by lava have been rebuilt. Many homeowners have sold their properties to neighbours or the county in a federally funded buyback program, but that land remains vacant for now. The land has been so transformed that it is hard for remaining owners to know even where their property begins and ends.

“It took out roughly a third of the subdivision; totally surreal,” Gates said last fall. “And houses are selling there again.”

Among Gates’s listings that day was a three-bedroom, two-bath home with lush landscaping, two blocks from the mile-wide lava field where heat and steam still radiate from vents in the petrified landscape. “It’s a beaut,” he said. “It will sell.”

Three weeks later it did, for $325,000, cash.

The story of how serene-looking slices of suburbia came to inhabit an active volcanic rift zone is well-known here. In the 1960s, land speculators—aided by a new county government hungry for tax revenue—bought thousands of acres and carved it into lots of an acre or more that were snapped up by investors.

There were virtually no requirements that developers pave roads, place utility lines or build other essential infrastructure. To this day, there is no wastewater treatment plant or hospital. Many of the district’s 51,000 residents rely on filtered rainwater and cesspools to dispose of sewage.

Early buyers included Native Hawaiians looking for an affordable place to call home and mainland hippies intent on off-grid living. As home prices rose in Hawaii and across the nation, however, more working families and mainland retirees went hunting for deals on the Big Island.

County Councilwoman Ashley Kierkiewicz, who represents Puna, said rush-hour traffic on the rural, two-lane highway that connects Puna to Hilo, the county seat roughly 20 miles away, is so bad that she leaves her home 1.5 hours early to get to work.

County officials say rules tied to federal funding bar local government from building affordable housing in lava zones 1 and 2, which are the riskiest and make up most of lower Puna. State law also prohibits them from spending most local money on private subdivisions, meaning that roads are largely maintained by owner associations.

Hawaii County Mayor Mitch Roth said that while the county has added a new firehouse, police station and park facilities there in recent years, the county has limited funds to make major investments in high-risk areas.

“Are we going to invest public money in a high-risk place…knowing that whatever you build could be taken out by lava at any time?” said Roth.

The lack of some modern conveniences has scarcely slowed the flow of newcomers.

Like many places in the U.S., an influx of remote workers during the pandemic has helped send the housing market here into overdrive.

Among the recent arrivals are David Booth and his partner, Juan Polanco. The former Phoenix residents had been brainstorming tropical locations where they could slash their living expenses and ease into retirement.

“The attraction to the Big Island was affordability,” said Booth, 61, who now works remotely. He and Polanco, 59, paid cash for a 1,500-square-foot home that had been split into three units with separate entrances. “You can’t have this on any other island for this price point.”

The property sits on a 1-acre lot in Hawaiian Paradise Park, a subdivision located in the less-risky lava zone 3. Homes with repeated sales in the neighbourhood have seen a nearly 800% appreciation in price since 2000, according to data from the University of Hawaii Economic Research Organization.

Properties in lava zones 1 and 2—some with sweeping oceanfront views—were far cheaper, Booth said. In the end, the risk of losing their nest egg to a natural disaster, and the difference in insurance rates, were deal breakers.

They are getting used to bringing in their drinking water and dealing with vicious fire ants. The slow-paced lifestyle and prospect of early retirement are worth it, he said.

They have listed the two other units as vacation rentals, and their first guests arrive next week.

“We are overwhelmed with the amount of beauty here and just how much more relaxed we feel,” said Booth. “We’re building a whole new life here.”

Three years ago, Travis Edwards, 48, was driving delivery trucks and living with his mother in Southern California’s Inland Empire.

He was sick of the traffic, wildfires and car thefts, he said. Upon retiring, his mother sold her house and paid cash for a 1-acre lot with two units in Leilani Estates, surrounded by avocado and citrus trees. Lava insurance rates in lava zone 1, the riskiest area that encompasses the entire subdivision, were so high that they simply stopped paying for it, he said.

He mostly shrugs off the dangers, reasoning that they would be reckoning with fires and earthquakes on top of a lower quality of life back in Southern California.

“It’s just paradise,” said Edwards, who now drives limousines part-time. “The rest of the world doesn’t exist when you’re here.”

Rising prices on the east side have left Puna native Chantel Takabayashi feeling stuck. A single mother of three, she works 16 hours a day as a state prison guard in Hilo. She would like to buy a home closer to work and better schools but has been priced out of most neighbourhoods she has considered.

“I make pretty decent money and I work long, endless hours, and I still can’t afford better housing,” she said.

Liz Fusco, who manages more than 100 rental properties for Hilo Bay Realty in Pahoa, said that during the pandemic, she saw three-bedroom homes in parts of Puna that once fetched $1,500 a month rent for as much as $2,300.

Most of the applicants were mainlanders, she said, with stellar rental histories, plenty of income and pristine credit. Units that would typically take more than a month to rent were getting leased in three days.

Tina Garber, who has lived in the Puna area for 21 years, has been displaced twice in the past 18 months after the homes she was renting went up for sale.

Currently, she is paying $750 a month—three-quarters of her monthly income as a housecleaner—for a 400-square-foot studio surrounded on three sides by cooled lava. Her landlord just told her it will be listed for sale in April.

“People that come over here with money, they do not realise that it is so hard to make it here,” Garber said. “They think, ‘Oh, a good deal in Hawaii.’ But it puts a lot of pain and suffering on local folks.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

Margot Robbie may have travelled from a Queensland farm to the highest reaches of Hollywood, but a reported $28 million property deal suggests the Gold Coast has never lost its hold on her. The Australian actor and producer is believed to be the mystery buyer of Redwood, a seven-acre Currumbin Valley estate transformed into the …

Continue reading “Margot Robbie Reportedly Behind $28 Million Currumbin Valley Homecoming”

Artificial intelligence is making it easier than ever to build a business without building a team. As AI takes over coding, customer support, marketing, administration, and other day-to-day tasks, a growing number of solo founders are scaling startups to millions in revenue with few—or even no—employees. While the trend is lowering barriers to entrepreneurship, it is also reshaping hiring, raising questions about the future of work and how businesses will grow in the AI era.

5 min

Ben Broca launched a company last December that offers AI tools to entrepreneurs. He’s already added 10,000 paying customers and is on track to bring in $10 million in revenue this year.

One thing he hasn’t added: any other employees.

The 40-year-old is part of a class of entrepreneurs who are launching, and then often running, new companies on their own. Artificial intelligence tools answer Broca’s emails, help write and debug code, field requests from customers, sign up new subscribers and grant refunds when issues arise.

Broca relishes his ability to make whatever decisions he wants on his own, often from his sun-drenched Sausalito, Calif., living room. “I think compromises make lukewarm results,” he said.

Once upon a time, running a business of a certain size required a team. AI is turning that assumption upside down, and more aspiring entrepreneurs are going it alone.

An analysis by the payments company Stripe shows there are thousands of solo operators on the company’s platform that are generating over $1 million in revenue, with their ranks doubling between 2023 and 2025. The number of solo operators crossing the $10 million threshold nearly tripled in that same span.

In the past, people without business contacts or particular savvy might not have known how to get their ideas off the ground, said Ernie Tedeschi, Stripe’s chief economist. “Now, AI can be a built-in business partner,” he said.

AI’s ability to handle various administrative tasks makes it potentially useful for launching solo businesses in many fields. But the technology’s ability to also handle key tasks in tech, like coding, make that field a particular hot spot.

Analyzing Census Bureau data, Bank of America Institute economist Taylor Bowley found that among all industries, new business applications in the information sector have seen the biggest percentage increase—nearly 45%—over the past year. At the same time, the rate of information-sector applicants saying they plan to hire workers has experienced the sharpest decline of any measured industry.

This Census dataset doesn’t track solo-operated businesses. But the numbers broadly show—in tech and beyond—that applications are flat among businesses likely to hire workers, but generally rising elsewhere. Economists say that’s a strong sign that solo operators are on the upswing.

“The bar for getting started has never been lower,” said Julian Weisser, who runs a San Francisco-based accelerator for solo founders working in tech. The accelerator—which offers founders seed money and mentorship in exchange for an equity stake—attracted 4,500 applicants for 10 slots made available in its most recent cycle, nearly five times the number it drew when it launched last May.

Going it alone with AI can still be surprisingly expensive. Broca said he was losing money on many customers’ accounts while paying to access Anthropic’s Claude to run his clients’ requests—that AI company, as well as others, charges based on usage. He has since switched to free open-source AI models from China.

Broca said he has raised $30 million from investors and, at the same time, has saved millions in salary since he hasn’t needed a team of software engineers.

Another risk: If it’s easy for one entrepreneur to launch an AI-assisted business, copying them can be easy, too. This creates anxiety for founders like Troy Johnston, who runs an AI-assisted business alone in Orlando, Fla.

“Everybody has the sword and we all have the ability to unsheathe Excalibur now,” said Johnston, 40, who used AI to code an app that helps people get the most out of credit card benefits. The company makes around $3,000 a month in profit, with no employees, and is continuing to grow.

What one-person businesses will mean for the labor market remains to be seen. Polling has shown Americans are worried that AI will replace jobs, and top economists are wrestling with that possibility, too. But AI is also creating lots of new jobs, and the go-it-alone entrepreneurs show how the technology can both open doors and limit employment opportunities.

“If everyone’s hiring less, but you get four times more firms, what does that do to head count?” said Rembrand Koning, an associate professor at Harvard Business School who studies entrepreneurship. He co-authored a recent study that found that among 50,000 startups the researchers examined, those focused on AI tended to operate with 25% fewer employees.

Koning also believes a soft hiring environment that’s left some people mired in long job searches has encouraged more to try their hand at launching businesses.

Some founders cite different motives. “It’s a perfect storm of post-pandemic burnout and a re-evaluation of one’s priorities, and also booming AI and a sense of what’s possible,” said Samir Ahmad, 39, who lives in Breinigsville, Pa.

Two years ago, Ahmad decided to leave the corporate job he had worked at Verizon for almost two decades to start a solo coaching and consulting business. He had been seeing social-media posts touting the ease and virtues of AI, which he used to chart a business plan and help with marketing. “It was like my chief of staff, a second in command,” he said.

The business ultimately petered out within months, though, and Ahmad is now back to a full-time corporate role with a utility company.

For Claire Vo, 41, AI helped her turn a passing impulse into a business. She was working full-time as a tech executive when she tapped AI in late 2023 to help code an app that would help her manage documentation and design for new products, with customers ranging from financial services to healthcare firms.

“I was copying and pasting from ChatGPT,” said Vo, who lives in San Francisco.

She put the app online for $1 a month, and within weeks people downloaded it thousands of times. Nearly three years later, Vo’s company—which she ran solo for nine months before hiring an engineer—now has 100,000 users and is on track to make seven figures in profit this year. AI handles the company’s marketing, sales and customer support.

While AI is a shortcut, Vo said her network and credibility in the industry were key. “I think people over-index on how easy AI is and under-index on how much I did to get to this point,” she said.

Three completed developments bring a quieter, more thoughtful style of luxury living to Mosman, Neutral Bay and Crows Nest.

A long-standing cultural cruise and a new expedition-style offering will soon operate side by side in French Polynesia.