The Robots Are Coming—to Collaborate With You

Doosan Robotics’ blockbuster IPO—the biggest in Korea this year—shows that the robot stock craze has well and truly arrived

2 min

2 min

Our future looks increasingly robotic—whether we like it or not. But the investment craze in robotics stocks may already be getting ahead of itself.

The latest example: South Korea’s Doosan Robotics, whose shares nearly doubled in value on their first day of trading Thursday. The company, which is part of the conglomerate Doosan Group, raised around $300 million from an initial public offering, making it Korea’s biggest IPO this year so far.

Doosan makes collaborative robots, or cobots, designed to work together with humans on factory floors. Such robotic helpers are most suitable for smaller companies that may not be ready to automate their whole production line but use cobots to automate processes better done by machines. Apart from its heavy-duty industrial robots, Doosan also makes variants that can serve coffee—and beer.

Doosan isn’t the only robotics company looking frothy of late. Shares of its smaller peer Rainbow Robotics, which is backed by Samsung Electronics, have more than quadrupled this year. Samsung raised its stake in Rainbow to 15% in March.

To be fair, there are plenty of good reasons to be optimistic about industrial robots. Poor demographics and poisonous immigration politics in most advanced economies will mean weak labor-force growth in the future. Robots rarely go on strike. And in the U.S., the enormous surge in manufacturing investment—courtesy of the Inflation Reduction Act and other industrial policy bills—means demand for manufacturing workers could remain strong for quite a while. Reshoring to advanced economies is another tailwind for robotics.

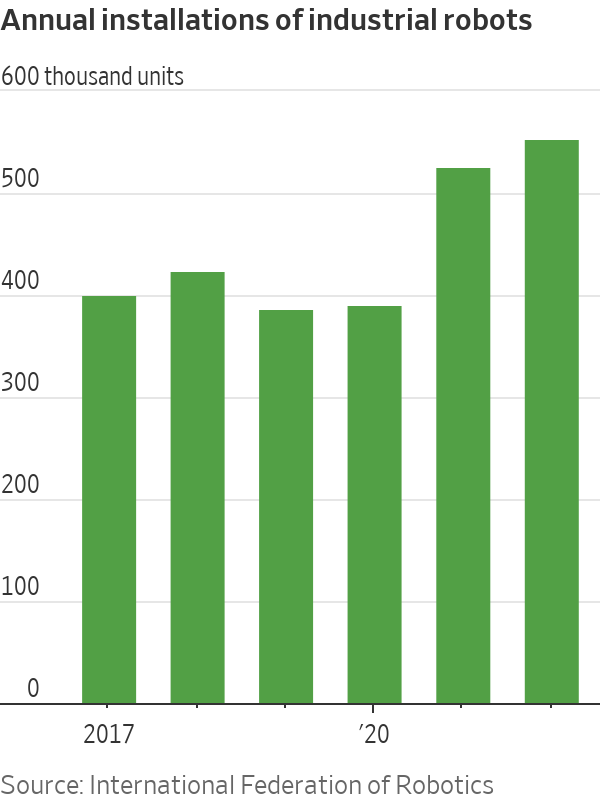

In 2022, almost 60% of Doosan’s sales came from North America and Europe. Though cobots are still a small part of the overall robot market—accounting for 7.5% of industrial robots installed in 2021, according to the International Federation of Robotics—shipments have been growing faster than the market as a whole. Installations for all industrial robots grew 5% year on year to a record high in 2022.

The company is the seventh-largest maker of cobots globally, according to its prospectus. But since the top two companies, Denmark’s Universal Robots and Japan’s Fanuc, dominate the sector with nearly half of the market, Doosan’s market share amounted to only 3.6%.

Doosan has been growing fast: Its sales more than doubled to around 45 billion won, the equivalent of $33 million, in 2022 from 2020. But it isn’t cheap. With a market capitalisation of around $2.5 billion, Doosan now trades at 74 times last year’s revenue. Fanuc trades at just 4.7 times revenue. Doosan is also unprofitable, though its chief executive expects it to move into the black next year.

The robot craze, like the artificial-intelligence craze, is grounded in real technological trends—and demographic ones too. But like human workers, not all robot firms are created equal. Jumping aboard the robot stock bandwagon at any price might not serve investors over the long run.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The federal budget has rattled property investors. But the biggest mistake isn’t the tax changes, it’s the conclusion many are drawing from them.

2 min

The recent budget has forced a reckoning for property investors.

Negative gearing now restricted to new residential builds, the CGT discount gone and on paper, the numbers look different.

And many investors are responding by pivoting toward yield, prioritising cash flow over capital growth in a way that property strategists say misses the point entirely.

“The debate has shifted to yield versus growth as if they are opposing forces,” says Abdullah Nouh, founder of Melbourne-based buyers’ agency Mecca Property Group. “But that framing is itself the mistake.”

Nouh, who works with high-net-worth families and investors on long-term acquisition strategy, argues that capital growth remains the primary driver of genuine wealth creation and that the post-budget environment has made quality assets more important, not less.

The numbers make his case plainly. An additional $500 per week in rental income is welcome. A prestige asset appreciating by $1 million over a market cycle is transformative.

These are not equivalent outcomes, and portfolios built around yield at the expense of location and land value tend to generate income while wealth stands largely still.

The more nuanced shift Nouh is seeing among sophisticated investors is a move toward assets where both outcomes can be engineered simultaneously – established homes on substantial land in quality locations, where the existing dwelling can be repositioned, rental returns improved, and the underlying land value compounds independent of what sits on it.

For investors with existing equity, commercial property is also entering the conversation in a more serious way.

Prestige industrial assets, medical centres and long-leased essential retail offer income profiles that residential property in most capital city markets cannot currently match: longer lease terms, tenants covering outgoings, and greater predictability than the residential tenancy cycle.

“The investors who build lasting wealth are rarely the ones who chased yield or growth exclusively,” says Nouh.

“They are the ones who built a strategy they could sustain – one that generated enough income to hold quality assets through multiple cycles while those assets compounded in value.”

The budget has changed the settings. It has not changed the fundamentals.

From Italian vegetable-tanned leather to real-world training insight, Australian brand PK9 Gear is redefining what luxury means for discerning dog owners.

From Tokyo backstreets to quiet coastal towns and off-grid cabins, top executives reveal where they holiday and why stepping away makes the grind worthwhile.