Where Are Stocks, Bonds and Crypto Headed Next? Five Investors Look Into Crystal Ball

Equities are often seen as expensive after promising start to 2023

7 min

7 min

A new trading year kicked off just weeks ago. Already it bears little resemblance to the carnage of 2022.

After languishing throughout last year, growth stocks have zoomed higher. Tesla Inc. and Nvidia Corp., for example, have jumped more than 30%. The outlook for bonds is brightening after a historic rout. Even bitcoin has rallied, despite ongoing effects from the collapse of the crypto exchange FTX.

The rebound has been driven by renewed optimism about the global economic outlook. Investors have embraced signs that inflation has peaked in the U.S. and abroad. Many are hoping that next week the Federal Reserve will slow its pace of interest-rate increases yet again. China’s lifting of Covid-19 restrictions pleasantly surprised many traders who have welcomed the move as a sign that more growth is ahead.

Still, risks loom large. Many investors aren’t convinced that the rebound is sustainable. Some are worried about stretched stock valuations, or whether corporate earnings will face more pain down the road. Others are fretting that markets aren’t fully pricing in the possibility of a recession, or what might happen if the Fed continues to fight inflation longer than currently anticipated.

We asked five investors to share how they are positioning for that uncertainty and where they think markets could be headed next. Here is what they said:

‘Animal spirits’ could return

Cliff Asness, founder of AQR Capital Management, acknowledges that he wasn’t expecting the run in speculative stocks and digital currencies that has swept markets to kick off 2023.

Bitcoin prices have jumped around 40%. Some of the stocks that are the most heavily bet against on Wall Street are sitting on double-digit gains. Carvana Co. has soared nearly 64%, while MicroStrategy Inc. has surged more than 80%. Cathie Wood‘s ARK Innovation ETF has gained about 29%.

If the past few years have taught Mr. Asness anything, it is to be prepared for such run-ups to last much longer than expected. His lesson from the euphoria regarding risky trades in 2020 and 2021? Don’t count out the chance that the frenzy will return again, he said.

“It could be that there are still these crazy animal spirits out there,” Mr. Asness said.

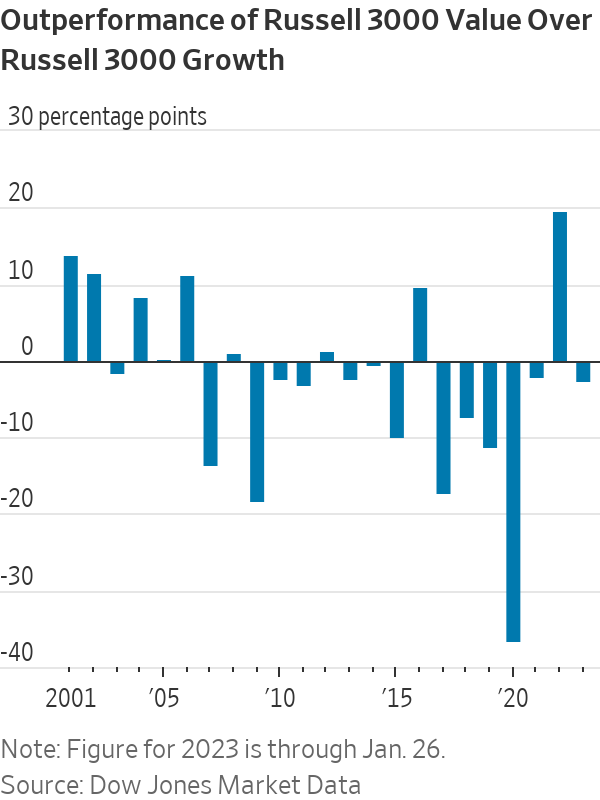

Still, he said that hasn’t changed his conviction that cheaper stocks in the market, known as value stocks, are bound to keep soaring past their peers. There might be short spurts of outperformance for more-expensive slices of the market, as seen in January. But over the long term, he is sticking to his bet that value stocks will beat growth stocks. He is expecting a volatile, but profitable, stretch for the trade.

“I love the value trade,” Mr. Asness said. “We sing about it to our clients.”

—Gunjan Banerji

Keeping dollar’s moves in focus

For Richard Benson, co-chief investment officer of Millennium Global Investments Ltd., no single trade was more important last year than the blistering rise of the U.S. dollar.

Once a relatively placid area of markets following the 2008 financial crisis, currencies have found renewed focus from Wall Street and Main Street. Last year the dollar’s unrelenting rise dented multinational companies’ profits, exacerbated inflation for countries that import American goods and repeatedly surprised some traders who believed the greenback couldn’t keep rallying so fast.

The factors that spurred the dollar’s rise are now contributing to its fall. Ebbing inflation and expectations of slower interest-rate increases from the Fed have sent the dollar down 1.7% this year, as measured by the WSJ Dollar Index.

Mr. Benson is betting more pain for the dollar is ahead and sees the greenback weakening between 3% and 5% over the next three to six months.

“When the biggest central bank in the world is on the move, look at everything through their lens and don’t get distracted,” said Mr. Benson of the London-based currency fund manager, regarding the Fed.

This year Mr. Benson expects the dollar’s fall to ripple similarly far and wide across global economies and markets.

“I don’t see many people complaining about a weaker dollar” over the next few months, he said. “If the dollar is falling, that economic setup should also mean that tech stocks should do quite well.”

Mr. Benson said he expects the dollar’s fall to brighten the outlook for some emerging- market assets, and he is betting on China’s offshore yuan as the country’s economy reopens. He sees the euro strengthening versus the dollar if the eurozone’s economy continues to fare better than expected.

—Caitlin McCabe

Stocks still appear overvalued

Even after the S&P 500 fell 15% from its record high reached in January 2022, U.S. stocks still look expensive, said Rupal Bhansali, chief investment officer of Ariel Investments, who oversees $6.7 billion in assets.

Of course, the market doesn’t appear as frothy as it did for much of 2020 and 2021, but she said she expects a steeper correction in prices ahead.

The broad stock-market gauge recently traded at 17.9 times its projected earnings over the next 12 months, according to FactSet. That is below the high of around 24 hit in late 2020, but above the historical average over the past 20 years of 15.7, FactSet data show.

“The old habit was buy the dip,” Ms. Bhansali said. “The new habit should be sell the rip.”

One reason Ms. Bhansali said the selloff might not be over yet? The market is still underestimating the Fed.

Investors repeatedly mispriced how fast the Fed would move in 2022, wrongly expecting the central bank to ease up on its rate increases. They were caught off guard by Fed Chair Jerome Powell‘s aggressive messages on interest rates. It stoked steep selloffs in the stock market, leading to the most turbulent year since the 2008 financial crisis. Now investors are making the same mistake again, Ms. Bhansali said.

Current stock valuations don’t reflect the big shift coming in central-bank policy, which she thinks will have to be more aggressive than many expect. Though broader measures of inflation have been falling, some slices, such as services inflation, have proved stickier. Ms. Bhansali is positioning for such areas as healthcare, which she thinks would be more insulated from a recession than the rest of the market, to outperform.

“The Fed is determined to win the war since they lost the battle,” Ms. Bhansali said.

—Gunjan Banerji

A better year for bonds seen

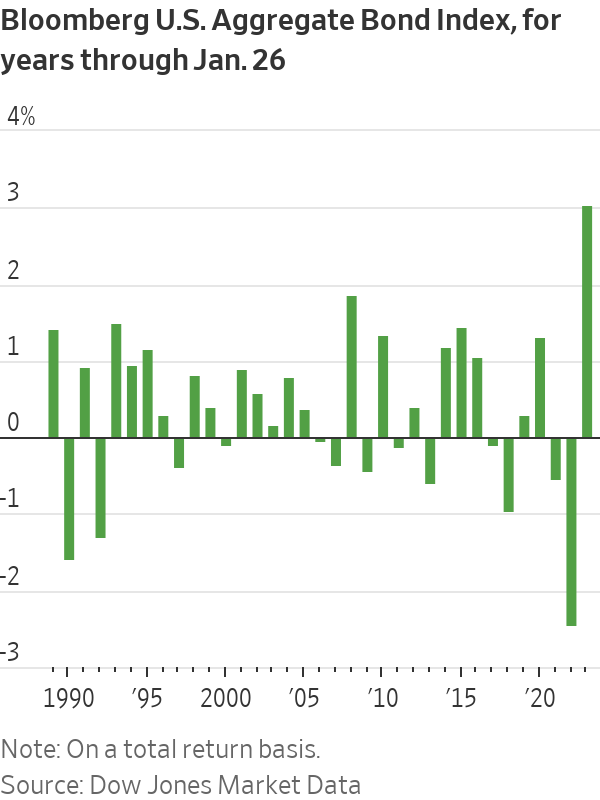

Gone are the days when tumbling bond yields left investors with few alternatives to stocks. Finally, bonds are back, according to Niall O’Sullivan of Neuberger Berman, an investment manager overseeing about $427 billion in client assets at the end of 2022.

After a turbulent year for the fixed-income market in 2022, bonds have kicked off the new year on a more promising note. The Bloomberg U.S. Aggregate Bond Index—composed largely of U.S. Treasurys, highly rated corporate bonds and mortgage-backed securities—climbed 3% so far this year on a total return basis through Thursday’s close. That is the index’s best start to a year since it began in 1989, according to Dow Jones Market Data.

Mr. O’Sullivan, the chief investment officer of multi asset strategies for Europe, the Middle East and Africa at Neuberger Berman, said the single biggest conversation he is currently having with clients is how to increase fixed-income exposure.

“Strategically, the facts have changed. When you look at fixed income as an asset class…they’re now all providing yield, and possibly even more importantly, actual cash coupons of a meaningful size,” he said. “That is a very different world to the one we’ve been in for quite a long time.”

Mr. O’Sullivan said it is important to reconsider how much of an advantage stocks now hold over bonds, given what he believes are looming risks for the stock market. He predicts that inflation will be harder to wrangle than investors currently anticipate and that the Fed will hold its peak interest rate steady for longer than is currently expected. Even more worrying, he said, it will be harder for companies to continue passing on price increases to consumers, which means earnings could see bigger hits in the future.

“That is why we are wary on the equity side,” he said.

Among the products that Mr. O’Sullivan said he favours in the fixed-income space are higher-quality and shorter-term bonds. Still, he added, it is important for investors to find portfolio diversity outside bonds this year. For that, he said he views commodities as attractive, specifically metals such as copper, which could continue to benefit from China’s reopening.

—Caitlin McCabe

Find the fear, and find the value

Ramona Persaud, a portfolio manager at Fidelity Investments, said she can still identify bargains in a pricey market by looking in less-sanguine places. Find the fear, and find the value, she said.

“When fear really rises, you can buy some very well-run businesses,” she said.

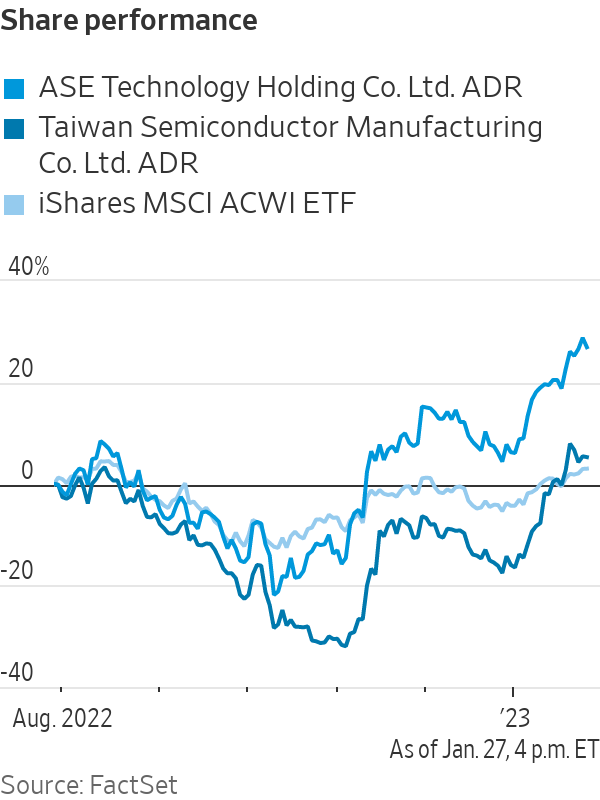

Take Taiwan’s semiconductor companies. Concern over global trade and tensions with China have weighed on the shares of chip makers based on the island. But those fears have led many investors to overlook the competitive advantages those companies hold over rivals, she said.

“That is a good setup,” said Ms. Persaud, who considers herself a conservative value investor and manages more than $20 billion across several U.S. and Canadian funds.

The S&P 500 is trading above fair value, she said, which means “there just isn’t widespread opportunity,” and investors might be underestimating some of the risks that lie in waiting.

“That tells me the market is optimistic,” said Ms. Persaud. “That would be OK if the risks were not exogenous.”

Those challenges, whether rising interest rates and Fed policy or Russia’s war in Ukraine and concern over energy-security concerns in Europe, are complicated, and in many cases, interrelated.

It isn’t all bad news, she said. China ended its zero-Covid restrictions. A milder winter in Europe has blunted the effects of the war in Ukraine on energy prices and helped the continent sidestep recession, and inflation is slowing.

“These are reasons the market is so happy,” she said.

—Justin Baer

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

2 min

2 min

Held by the same family for 26 years, this Harbour Bridge-facing residence at Longueville is the type of property that rarely comes to market. Set on more than 1,100 sqm on one of Sydney’s most tightly held peninsulas, it combines complete privacy with uninterrupted views across the harbour to the city skyline.

It’s the sort of offering where the land is just as important as the home. Positioned directly opposite Aquatic Park with a prized northeast aspect, the residence captures sweeping harbour views from almost every main living space while remaining remarkably secluded from neighbouring properties.

Large picture windows frame the outlook throughout the home, flooding the interiors with natural light and making the harbour the centrepiece of everyday living.

Designed for family living

The home offers multiple living zones, including a formal lounge and dining rooms, a separate family room and an open-plan living and meals area. Blackbutt timber parquetry flooring, high ceilings and ducted reverse-cycle air conditioning feature throughout.

The kitchen sits at the heart of the home, with induction cooking, a generous island bench, and a walk-in pantry, connecting both the formal entertaining areas and the more casual family spaces.

A ground-floor master suite includes a walk-in robe, dressing area and ensuite, while upstairs are three additional bedrooms with built-in robes, together with a spacious home office or study.

The lower ground level adds another layer, with a temperature-controlled cellar and tasting room, plus a flexible gym, wellness or recreation space.

Resort-style setting overlooking Sydney Harbour

Outside, landscaped gardens wrap around a heated swimming pool, an expansive entertaining terrace, and a level lawn, creating a private resort-style setting against the backdrop of Sydney Harbour.

Additional features include a solar system with battery storage, remote lock-up garaging for three vehicles and generous storage throughout.

Beyond the home itself, the location remains one of Longueville’s biggest drawcards. Longueville Ferry Wharf sits around 150 metres away, providing direct access to the CBD while preserving the quiet character of one of Sydney’s most tightly held waterfront suburbs. The property is also within the catchments of Lane Cove Public School and Hunters Hill High School.

Simon Harrison and Kim Walters of Belle Property Lane Cove are marketing the property on a Contact Agent basis.

At a glance

Address: 3 Mary Street, Longueville NSW 2066

Configuration: 4 bedrooms | 3 bathrooms | 3-car garage

Land: Approximately 1,100 sqm

Highlights: Harbour Bridge and city skyline views, northeast aspect, heated pool, cellar, solar with battery storage

Held: First time offered in 26 years

Price: Contact Agent

Agents: Simon Harrison and Kim Walters, Belle Property Lane Cove

This article is produced by the Kanebridge Media editorial team. Property information has been supplied by the listing agent. Buyers should conduct their own due diligence before relying on any information contained in this article. Enquiries: propertyconcierge@kanebridge.com.au.

High-end homeowners are choosing to upgrade rather than relocate, investing in bespoke design, premium finishes and long-term lifestyle value.

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.