Beautiful one day, pricey the next

Low vacancy rates and rising rents make life tough on tenants in the Sunshine State while investors see strong capital growth

2 min

2 min

Renters in Queensland are experiencing the greatest rental pressure in the country, new data shows.

The Rental Pain Index released by content and research provider Suburbtrends shows the Sunshine State has seen the highest average rental increase in 12 months across the country at 16.33 percent.

“The significant increase in rental prices over the past year in Queensland is a clear contributor to the heightened rental pain felt by residents,” said founder of Suburbtrends, Kent Lardner. “Similar trends are observed in South Australia and Western Australia, where rental prices have risen by approximately 15.95 percent and 15.37 percent, respectively.”

The findings are the result of analysis of the top 25 rental results in each state comparing advertised rentals, vacancy rates and average rent increases over a 12 month period. It also examines average rents as a percentage of income.

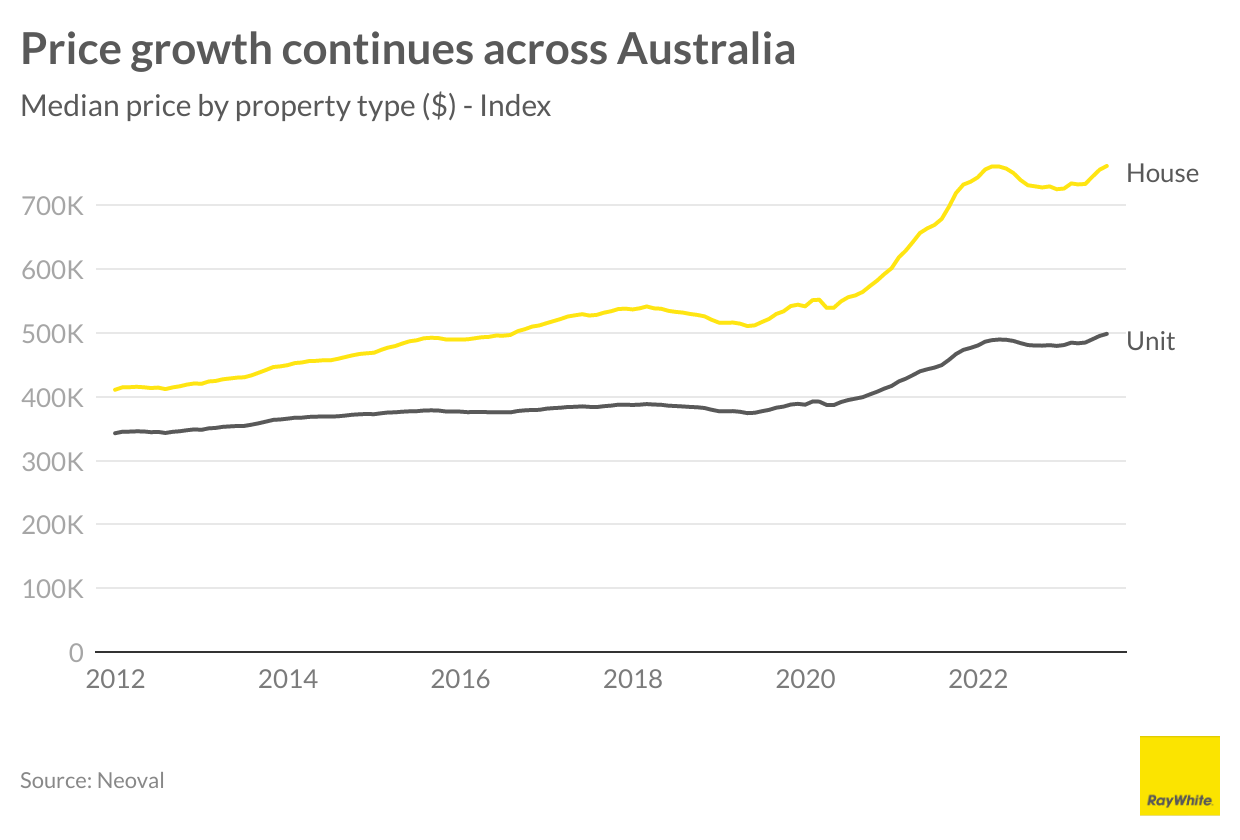

The report comes on the back of data released by Ray White Real Estate which reveals that unit prices in Brisbane are growing at a faster pace than houses.

Ray White chief economist Nerida Conisbee said unit price growth has kept pace with that of houses, with apartment prices now back to their 2022 peak. She attributed the recent downturn in apartment prices to the lockdown lifestyle of the pandemic.

“Apartment living wasn’t much fun during lockdowns. Living in smaller spaces with restricted movement was difficult and a lot of the best things about urban living were not available,” Ms Conisbee said.

“Now that things are pretty much back to normal, apartment living is again attractive. Most of us are going back to the office more frequently and all the best things about living in higher density suburbs are back.

“We have moved quickly from a situation where there were too many apartments to not enough. Demand is exceeding supply, driving up prices and rents.”

Ms Conisbee noted that demand for apartments would continue to outstrip supply as building approvals were at their lowest point in more than a decade while construction costs were at record highs.

She said the future of the Australian residential market was apartment living, which is not reflected in current housing stock around the country.

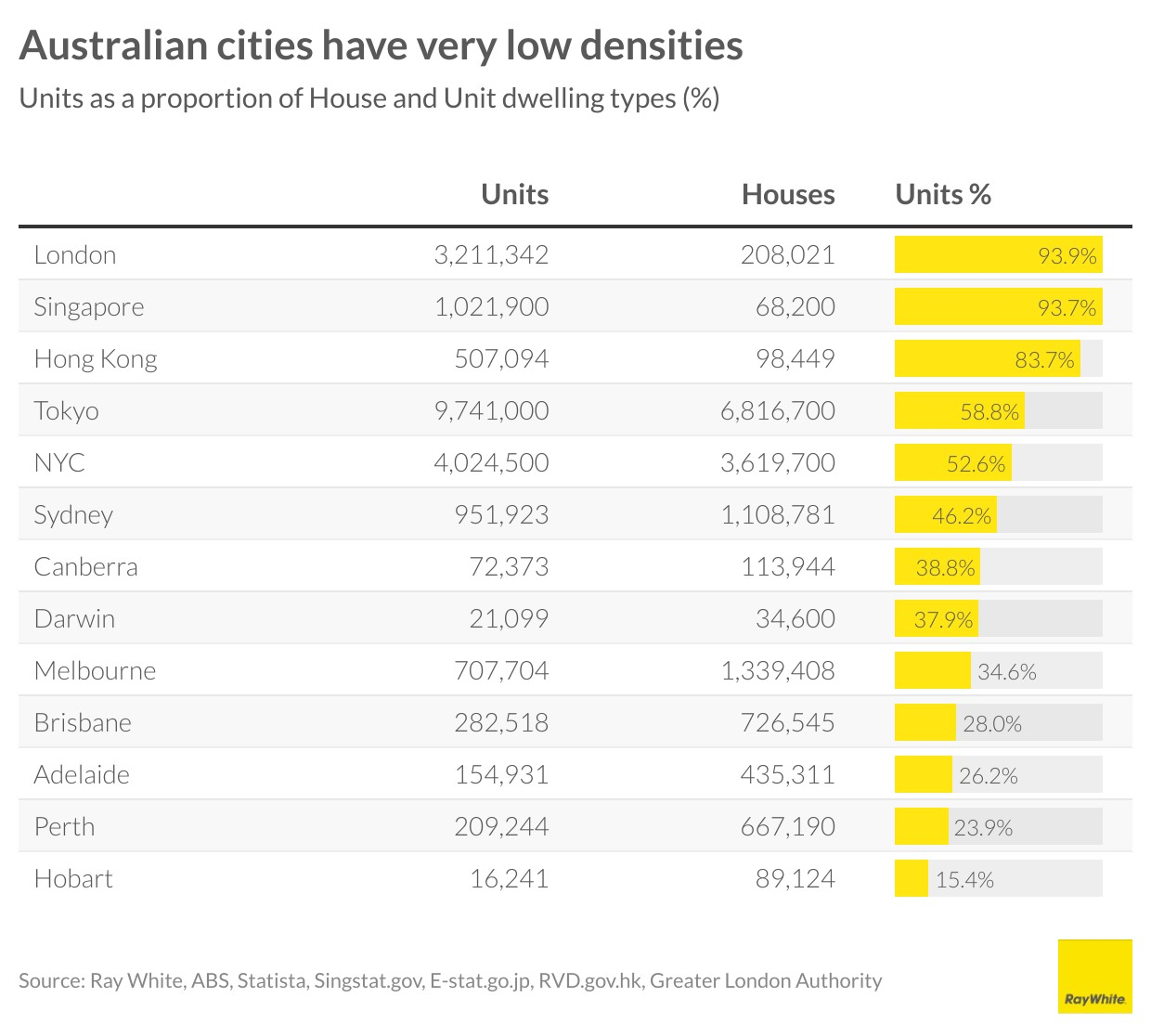

“Australia has extremely low density relative to other major cities,” Ms Conisbee said. “Sydney is our highest density city but half of all homes are still detached houses. In Hobart, just 15 percent of homes are attached or apartments.”

Automobili Lamborghini and Babolat have expanded their collaboration with five new colourways for the ultra-exclusive BL.001 racket, limited to just 50 pieces worldwide.

As housing drives wealth and policy debate, the real risk is an economy hooked on growth without productivity to sustain it.

Strong consumer spending and tight supply have driven retail to the top of commercial property, but signs of pressure are starting to emerge.

2 min

Australia’s retail property sector entered 2026 as the strongest performing commercial asset class, but rising geopolitical risks and cost pressures are beginning to test its resilience, according to new research from Knight Frank.

The latest Australian Retail Review shows the sector rode a wave of consumer spending and constrained supply through 2025, delivering total returns of 9.2 per cent and driving transaction volumes up 43 per cent year-on-year to $14.4 billion.

That momentum carried into early 2026, with around $3.6 billion in deals recorded in the first quarter alone.

“Retail clearly emerged as the standout commercial property performer in 2025,” said Knight Frank Senior Economist, Research & Consulting Alistair Read.

“Improving household spending, limited new supply and stronger leasing fundamentals combined to drive better income growth and renewed investor confidence in the sector.”

Spending rebound drives retail strength

A lift in household spending has been central to the sector’s performance. Consumer spending rose 4.6 per cent year-on-year to February 2026, supported by easing inflation and improving real incomes.

That shift flowed directly into retailer performance, with average EBIT margins across major retailers rising to 8.9 per cent in the first half of 2026, their strongest level in several years.

“Stronger consumer spending was critical in restoring momentum to the retail sector,” Mr Read said.

“Retailers have generally been better able to absorb costs, rebuild margins and support sustainable rental outcomes, particularly in higher-quality centres.”

Improved trading conditions also pushed leasing spreads up 4.2 per cent in 2025, reinforcing income growth and supporting capital values.

Geopolitical tensions begin to bite

But the outlook has become more complicated. The report warns that escalating conflict in the Middle East and its impact on fuel prices, supply chains and interest rates could weigh heavily on consumer spending.

“Higher fuel prices, flow-on cost pressures across supply chains, and recent interest rate increases are collectively squeezing household budgets, and early consumer sentiment data suggests confidence is already softening,” Mr Read said.

“While household balance sheets remain generally resilient, heightened uncertainty over future costs is likely to weigh on spending — particularly in discretionary categories — in the months ahead.”

The impact is already being felt in investment activity. While the year began strongly, transaction volumes slowed in March as investors paused amid the uncertainty.

“Early indicators suggest elevated uncertainty has already begun to affect the market. While retail investment enjoyed its strongest start to a year in a decade, with nearly $3 billion transacted by the end of February, activity stalled in March, as investors took a pause amid elevated uncertainty,” Mr Read said.

Solid foundations support medium-term outlook

Despite the near-term headwinds, Knight Frank maintains that the sector’s underlying fundamentals remain strong. Limited new supply, high construction costs and population growth are expected to continue supporting rental growth over the medium term.

“Retail has entered this period of uncertainty from a position of strength,” Mr Read said.

“Supply-side constraints, population growth and improving income fundamentals remain powerful structural supports for the sector.”

The report highlights several trends shaping the year ahead, including steady yields as interest rates rise, mounting pressure on tenant margins, continued outperformance of prime centres, the growing need for logistics integration, and risks linked to underinvestment in capital expenditure.

For now, retail remains a sector with momentum, but one increasingly at the mercy of forces far beyond the shopping centre.

From warmer neutrals to tactile finishes, Australian homes are moving away from stark minimalism and towards spaces that feel more human.

A divide has opened in the tech job market between those with artificial-intelligence skills and everyone else.