Chronic Wildfires Are Impacting California Home Values

Report by the San Francisco Fed shows small increase in premiums for properties further away from the sites of recent fires

3 min

3 min

Wildfires in California have grown more frequent and more catastrophic in recent years, and that’s beginning to reflect in home values, according to a report by the San Francisco Fed released Monday.

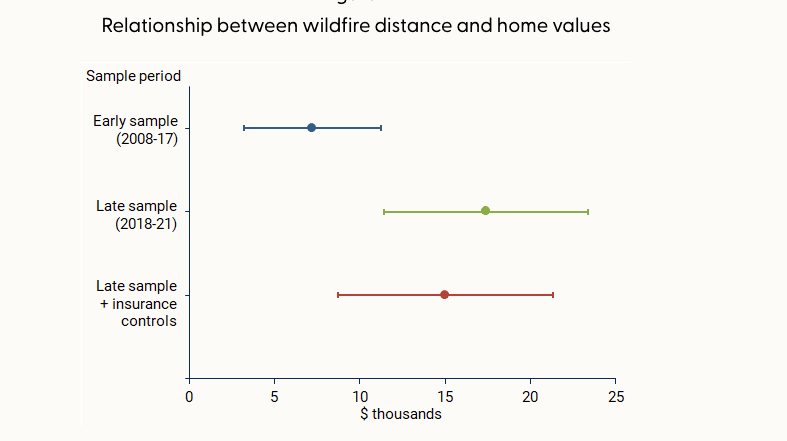

The effect on home values has grown over time, and does not appear to be offset by access to insurance. However, “being farther from past fires is associated with a boost in home value of about 2% for homes of average value,” the report said.

In the decade between 2010 and 2020, wildfires lashed 715,000 acres per year on average in California, 81% more than the 1990s. At the same time, the fires destroyed more than 10 times as many structures, with over 4,000 per year damaged by fire in the 2010s, compared with 355 in the 1990s, according to data from the United States Department of Agriculture cited by the report.

That was due in part to a number of particularly large and destructive fires in 2017 and 2018, such as the Camp and Tubbs fires, as well the number of homes built in areas vulnerable to wildfires, per the USDA account.

The Camp fire in 2018 was the most damaging in California by a wide margin, destroying over 18,000 structures, though it wasn’t even in the top 20 of the state’s largest fires by acreage. The Mendocino Complex fire earlier that same year was the largest ever at the time, in terms of area, but has since been eclipsed by even larger fires in 2020 and 2021.

As the threat of wildfires becomes more prevalent, the downward effect on home values has increased. The study compared how wildfires impacted home values before and after 2017, and found that in the latter period studied—from 2018 and 2021—homes farther from a recent wildfire earned a premium of roughly $15,000 to $20,000 over similar homes, about $10,000 more than prior to 2017.

The effect was especially pronounced in the mountainous areas around Los Angeles and the Sierra Nevada mountains, since they were closer to where wildfires burned, per the report.

The study also checked whether insurance was enough to offset the hit to values, but found its effect negligible. That was true for both public and private insurance options, even though private options provide broader coverage than the state’s FAIR Plan, which acts as an insurer of last resort and provides coverage for the structure only, not its contents or other types of damages covered by typical homeowners insurance.

“While having insurance can help mitigate some of the costs associated with fire episodes, our results suggest that insurance does little to improve the adverse effects on property values,” the report said.

While wildfires affect homes across the spectrum of values, many luxury homes in California tend to be located in areas particularly vulnerable to the threat of fire.

“From my experience, the high-end homes tend to be up in the hills,” said Ari Weintrub, a real estate agent with Sotheby’s in Los Angeles. “It’s up and removed from down below.”

That puts them in exposed, vegetated areas where brush or forest fires are a hazard, he said.

While the effect of wildfire risk on home values is minimal for now, it could grow over time, the report warns. “This pattern may become stronger in years to come if residential construction continues to expand into areas with higher fire risk and if trends in wildfire severity continue.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

The influencer and fitness entrepreneur is offloading the four-bedroom Main River residence she has called home since 2020 following her split from ex-husband Matt Zukowski.

< 1 min

Fitness entrepreneur and social media personality Tammy Hembrow has put her Broadbeach Waters mansion on the market, ending a six-year stint in the riverfront home she has regularly featured in content shared with her millions of followers.

Hembrow bought the property in June 2020 for $2.88 million.

Sitting on an oversized 979sqm allotment with north-east orientation and more than 30 metres of river frontage, the double-storey residence is set behind security gates at the end of a quiet cul-de-sac.

The home has been a fixture of Hembrow’s online presence for years, serving as the backdrop to family life and business updates for the mother-of-three, who also lived there with her former husband, Love Island Australia star Matt Zukowski, before the pair separated in mid-2025 following a brief marriage.

Inside, the residence centres on an open-plan kitchen, lounge and dining area that opens onto the pool and alfresco entertaining space, designed to make the most of the Gold Coast’s indoor-outdoor lifestyle.

Upstairs, the master suite includes a walk-through robe, dedicated dressing room and ensuite, alongside two further bedrooms, while a fourth bedroom downstairs offers separate access for guests or extended family. A multi-purpose room adds flexibility for use as a media room, home office or children’s retreat.

Outdoor features include a tiled pool, built-in barbecue and bar area, firepit and private boat ramp — amenities suited to the waterfront entertaining lifestyle the Broadbeach Waters pocket is known for.

The property is being marketed by Jay Helprin of Ray White through an expressions of interest campaign, with private inspections only and no scheduled public opens.

Hembrow, who built her public profile from 2014, documenting her fitness journey through three pregnancies, went on to launch fitness app TammyFit, which has since been downloaded more than a million times.

Three completed developments bring a quieter, more thoughtful style of luxury living to Mosman, Neutral Bay and Crows Nest.

Rugged coastal drives and fireside drams define a slow, indulgent journey through Scotland’s far north.