Is Germany’s Economic Model Truly Kaputt?

4 min

4 min")

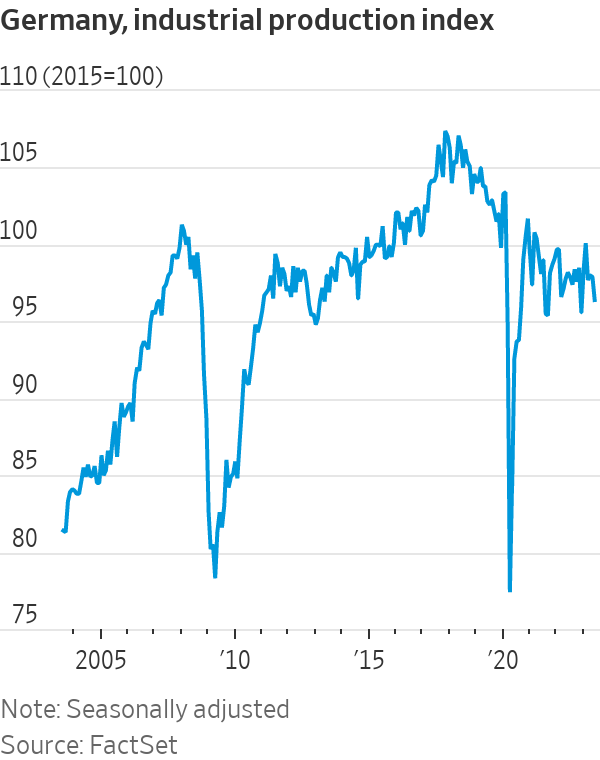

More than two decades after Germany was famously called “the sick man of the euro” by The Economist magazine, investors must wonder if the country’s industrial heart is once again critically weak. This week brought more dismal German economic data: Industrial production fell 1.5% in June from the previous month, worse than analysts expected. Though figures released on Friday showed a rise in exports, the volume of goods Germany sends abroad is still close to lows plumbed in the 2009 global financial crisis.

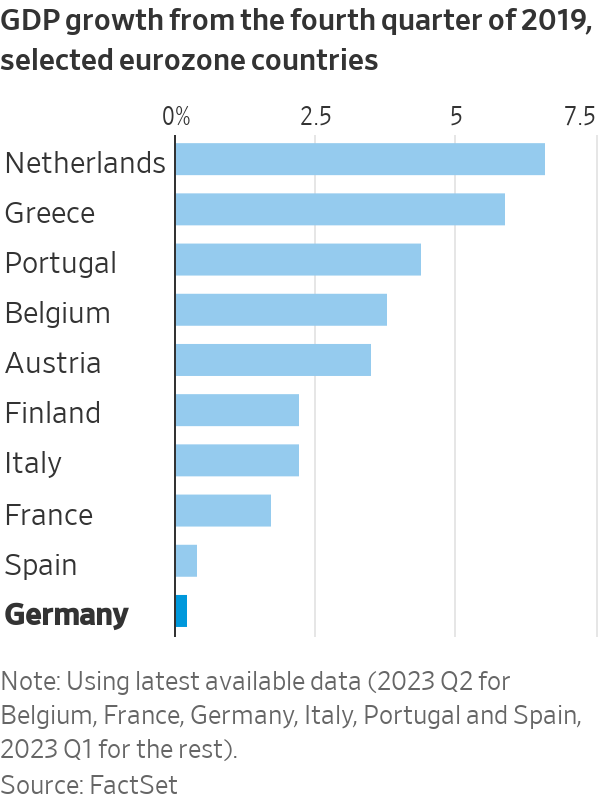

German gross domestic product has clocked three quarters of negative or zero growth , making the country the worst performer among major eurozone nations since 2019. Previously it was the top performer. How long this “slowcession” lasts is a crucial question for picking stocks in Europe. Despite the recent economic reversal, the DAX has been by far the best equity index in the eurozone over 20 years, returning almost 360%.

By comparison, investing in long-stagnant Italy yielded a paltry 140% return. German industrial output has been in decline since 2018, when global vehicle sales fell for the first time in almost a decade. A postpandemic rebalancing of spending toward services has made the situation worse. Growth in China, the fourth-largest market for German exporters, has slowed.

On Thursday, shares in Siemens —the largest industrial firm in Europe—fell 5% after it cited these two factors as the cause of a fall in orders during the second quarter. Some of the grit that has gotten into the German economic machine might be hard to dislodge . Chinese carmakers have turned from partners into fierce competitors as Volkswagen , BMW and Mercedes-Benz play catch-up in electric-vehicle technology.

It isn’t just China that is seeking to substitute imports for domestic products; the Biden administration is copying Beijing’s playbook. There is also energy. At the same time as German industry has lost Russia as its main source of cheap gas, Berlin has closed the country’s last three nuclear power plants. Angst has gripped German officials and executives in an echo of worries voiced at the start of the millennium, when unemployment surged and globalisation ravaged factories.

Back then, the response was a policy package that prioritised international competitiveness, incentivising the creation of low-pay “minijobs.” The government embraced fiscal austerity and nudged unions to push for wage restraint. The result was a 20-year decline in unemployment and a current-account surplus that reached an eye-watering 8% of GDP even as the U.S. ran huge deficits. Many economists praised German labor flexibility and fiscal austerity.

Conversely, critics pointed out that surpluses made most households worse off, and that Germany’s factory-job losses were just as large as America’s. Politics aside, it was largely a fortuitous jump in foreign demand that drove growth, allowing the nation to solidify gains in industries where it already had an advantage.

“Over the last 20 years, Germany always had an external sugar daddy: China, the eurozone and then the U.S.,” said Carsten Brzeski , chief economist at ING.

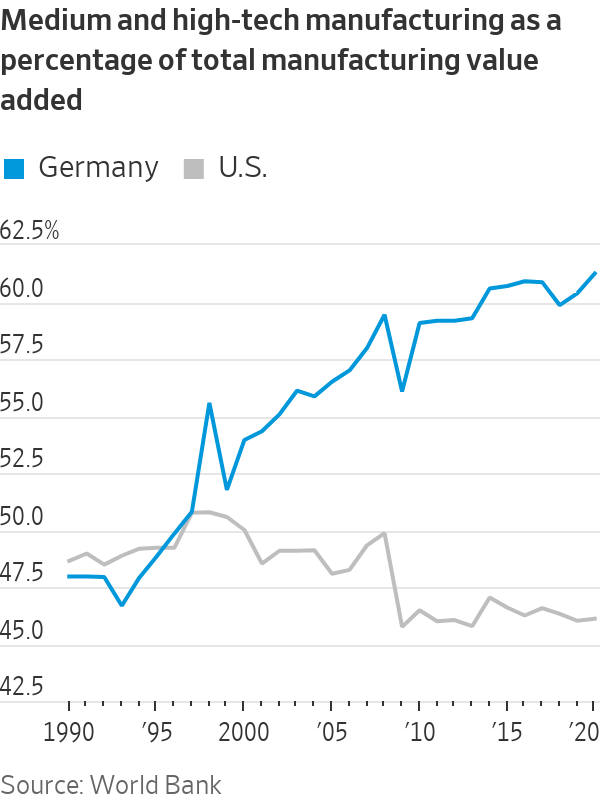

The flaw in this model was that it outsourced economic policy, leading to problematic dependencies on geopolitical rivals. It also fostered an excessive focus on old winners at the expense of new digital technologies and renewable energy. Bearish investors are right that it will take years to rectify these problems, particularly given the complexity of consensus-based German politics. Yet the German export-led model also got a lot right. As in China or South Korea, it channeled demand toward higher-productivity, higher-wage firms.

Unlike in the U.S., German manufacturing became more complex. That allowed the country’s industrial base to survive better than in other Western countries. In a world where nations are scrambling to reshore industries, Germany already has them. The readiest answer to its growth challenge isn’t to turn away from manufacturing but to double down by taking a page from Chinese and now U.S. industrial policy.

The German government is already doing this with semiconductors as part of the European Chips Act. Back in June, it signed off on 10 billion euros (around $11 billion) in subsidies for American chip maker Intel to build two plants, and earlier this week it committed €5 billion to help Taiwan’s TSMC set up a factory with local partners like Infineon.

A similar approach is needed to upgrade the country’s power generation and transmission and accelerate the transformation of carmakers and other industrial incumbents. Long-term energy guarantees could stem cost swings in the meantime. Given its political influence over the European Union, it seems hard to imagine that the bloc’s green-economy push could somehow leave Germany in a less dominant position . Historically, this is one patient that always leaves the hospital.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

The Federal Budget may have softened some of its proposed tax reforms, but it has exposed a bigger issue: too many families are relying on wealth structures that no longer reflect the realities of modern life.

3 min

For many Australians, the 2026 Federal Budget initially felt like a direct challenge to the way wealth is created, held and transferred between generations.

The headlines were immediate: changes to capital gains tax, reforms to discretionary trusts, restrictions on negative gearing and increased scrutiny of investment structures. Unsurprisingly, affluent families, business owners and investors began asking the same question:

Is the way we hold our wealth still fit for purpose?

In recent days, the government has announced several significant amendments following industry consultation and public feedback, including exempting testamentary trusts from the proposed 30 per cent minimum tax and expanding capital gains tax concessions for small businesses.

The backdown is welcome. But it also highlights something much bigger.

This Budget has accelerated a conversation that many Australian families have been postponing for years.

The conversation is not really about tax. It is about wealth stewardship.

For decades, Australians have built wealth through businesses, property, investments and careful long-term planning. Yet many families have not revisited the legal structures surrounding those assets in years, sometimes decades.

We often see clients who have spent years building significant wealth, only to discover their legal arrangements no longer reflect their current circumstances.

Their children are now adults. They may own multiple properties.

They may have sold a business, entered a second marriage, become grandparents or accumulated digital assets that did not exist when their original estate plans were prepared.

The trust that distributes income may need to be reconsidered. The bucket company may no longer be so attractive.

The Budget has simply exposed a reality that already existed: wealth structures cannot remain static while life continues to evolve.

Importantly, trusts themselves are not the issue.

Trusts are legitimate planning tools that provide flexibility, protection and continuity. When used appropriately, they allow families to adapt to changing circumstances over time.

And neither is tax the issue, really. Getting the fundamentals right is more important for long-term, sustainable wealth than a few favourable tax treatments around the edges.

The real issue is complacency.

Too often, families create structures and assume the job is done. It isn’t.

Estate planning is no longer a document you sign once and file away in a drawer. It is an ongoing process that should evolve alongside your life.

We are also seeing a broader shift in how Australians define wealth itself. It is no longer just the family home and an investment portfolio.

Modern wealth includes businesses, digital assets, cryptocurrency, intellectual property, frequent flyer points and increasingly complex family arrangements.

At the same time, Australians are living longer than ever before, meaning wealth may need to support multiple generations simultaneously. This creates new responsibilities and new risks.

How do you help your children enter the property market without exposing family wealth to relationship breakdowns?

How do you structure wealth so that it remains a source of opportunity rather than future conflict?

These are the questions families should be asking now.

The recent debate surrounding testamentary trusts also serves as an important reminder that policy decisions can have unintended consequences for vulnerable Australians. It is encouraging that the government has listened to feedback and clarified its position.

But the lesson remains: the wealth landscape is changing.

Increasingly, governments, regulators and tax authorities are paying closer attention to how wealth is held and transferred. That means families cannot afford to adopt a “set-and-forget” approach to their structures.

The families who will be best placed for the future are not necessarily those with the greatest wealth.

They are the families with the greatest clarity. Clarity around ownership, succession and governance. And clarity around how wealth will transition from one generation to the next.

Ultimately, preserving wealth is not about avoiding change.

It is about preparing for it.

Because the greatest risk is not change itself.

It is losing the ability to respond to it.

Anthony Hunt is Co-Founder of Wealth Lawyers and former COO of Westpac Private Bank. He advises business owners, investors and affluent Australian families on wealth protection, succession planning and intergenerational wealth transfer

A haven for hedge-fund titans and Hollywood grandees, Greenwich is one of the world’s most expensive residential enclaves, where eye-watering prices meet unapologetic grandeur.

Travellers are swapping traditional sightseeing for immersive experiences, with Africa emerging as a must-visit destination.