Desperate Chinese Property Developers Resort to Bizarre Marketing Tactics

The country’s real-estate slump is getting worse—and looks set to drag on for years

3 min

3 min

China’s real-estate crisis has dragged down the economy, caused massive layoffs and pushed multibillion-dollar companies to the point of collapse.

Economists think it is about to get worse.

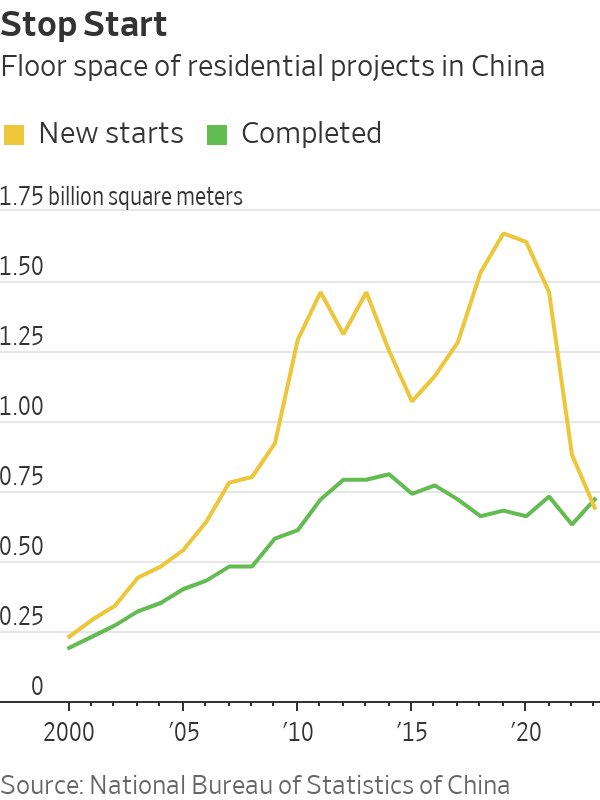

Sales of newly built homes in China fell 6% last year, returning to a level not seen since 2016, according to China’s statistics bureau. Secondhand home prices in its four wealthiest cities—Beijing, Shanghai, Guangzhou and Shenzhen—declined by between 11% and 14% in December from the year before, according to the broker Centaline Property.

Developers are starting fewer projects. Homeowners are paying back their mortgages early and borrowing less. Once-thriving property companies are stuck in protracted negotiations with foreign investors, following defaults on about $125 billion of overseas bonds between 2020 and late 2023, according to figures from S&P Global Ratings.

Chinese developers and local governments are so desperate to attract home buyers that some have resorted to bizarre marketing strategies.

A property company in Tianjin ran a video advertisement featuring the slogan “buy a house, get a wife for free.” It was a play on words, using the same Chinese characters as the phrase “buy a house, and give it to your wife”—but presented in a sentence structure typically used to offer freebies for home buyers. In September, the company was fined $4,184 for the ad.

A residential compound in eastern China’s Zhejiang province promised last year to give home buyers a 10-gram gold bar.

Earlier this month, Sheng Songcheng, former head of the statistics department at the People’s Bank of China, told a local conference that the housing downturn would last another two years. He thinks new-home sales will fall more than 5% in both 2024 and 2025.

Wall Street economists are also ringing alarm bells about how long the real-estate slump will last.

“Not too many people are buying, can buy or want to buy,” said Raymond Yeung, chief China economist at ANZ. He said there had been a fundamental shift in the way Chinese people view the property sector, with housing no longer seen as a safe investment.

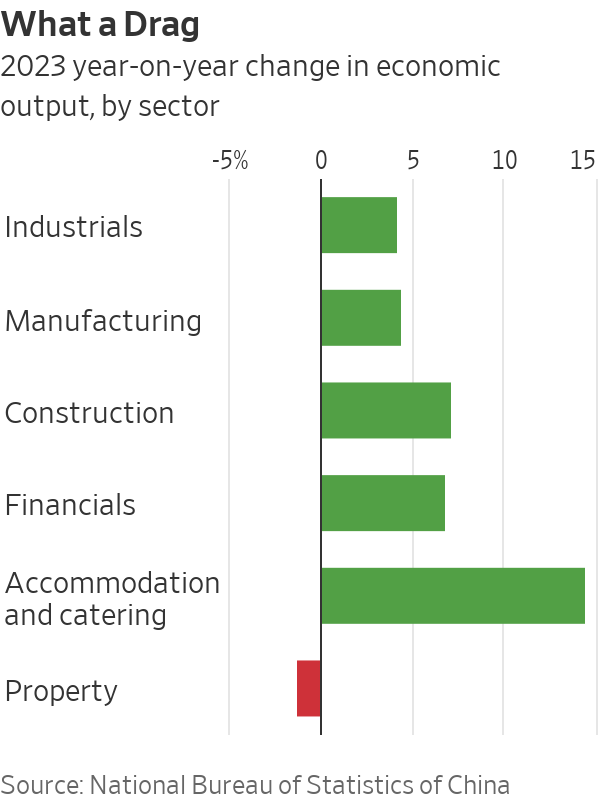

China’s real-estate sector and related industries once accounted for around a quarter of gross domestic product and the sector’s slump has been a significant drag on the world’s second-largest economy. That has increased calls for Beijing to do more to prop up the sector, but so far Chinese officials have stuck to piecemeal policies rather than introducing a landmark stimulus package.

A number of economists are making comparisons to Japan, which spent decades trying to rebound from a crash in real-estate and stock prices. China’s stock market is in a years-long slump.

China’s central bank can help make the situation less painful, but it will need to be aggressive, said Li-gang Liu, head of Asia Pacific economic analysis at Citi Global Wealth Investments. The central bank still has policy room and could take one big step to make a significant impact, he said.

Liu Yuan, head of property research at Centaline, said that without the government’s help, new-home prices will need to drop by another 50% from current levels before they reach a bottom. This is based on the assumption that the tipping point will only come when it is cheaper to buy than to rent houses, Liu said.

China’s real-estate downturn has claimed dozens of victims. More than 50 developers—mostly privately owned—have defaulted on their debt. Developers still have millions of unfinished homes that were sold but not delivered. Chinese authorities have set aside billions of dollars to help builders complete apartments but the logjam is growing.

The crisis has drained the coffers of some Chinese local governments, which previously relied on land sales as a main source of income. Economists estimate they have hidden debt worth anything from $400 billion to more than $800 billion. To quiet talk of potential defaults, the central government has set up debt-swap programs to help some of them refinance.

Some economists are optimistic. In the first half of this year, buyers of secondhand homes will gradually return to the new-home market and prop up the sector, said Helen Qiao, chief China economist at Bank of America. “Things will slowly get better from here,” Qiao said.

But most are still expecting more pain, and investors are bearish. A benchmark of Hong Kong-listed property stocks had fallen for four years in a row before the start of this year. Since Jan. 1, it is down another 15%.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

Australia’s housing affordability crisis is being fuelled by chronic undersupply, planning delays and rising development costs, as politicians continue to focus on the wrong solutions.

3 min

Australia’s housing crisis will not be solved by first-home buyer incentives or tax changes alone, with leading property figures warning governments must tackle supply constraints if affordability is to improve.

Speaking at the Kanebridge Quarterly Property Leadership Summit in Sydney last week, expert project marketing specialist Sam Elbanna, property investor and fund manager Paul Miron and property consultant Karla McNeice said that a lack of housing supply remained the central issue facing the market.

Elbanna, Director of CPM Realty with more than 30 years’ experience in project sales, argued that successive governments had focused too heavily on stimulating demand rather than addressing the barriers preventing new housing from being delivered.

“The misconception is that politicians think the way to solve the housing crisis is to drive demand,” he said.

“The reality is that’s not the way. This is a supply-side problem, and it needs to be solved on the supply side.”

Drawing on his experience in project sales, Elbanna said policies designed to help first-home buyers often had unintended consequences, pointing to previous grants that ultimately flowed through to higher property prices.

Instead, he said developers were facing increasing red tape, approval delays and rising costs, which were discouraging new housing supply.

“In the absence of stock, demand exceeds supply,” he said.

Miron, a Co-Founder and Fund Manager of Msquared Capital, said the housing debate had become overly focused on tax policy while overlooking broader structural issues.

He argued that affordability challenges stemmed from a combination of factors, including planning constraints, supply shortages, migration levels and interest rates.

“No-one can be 100 per cent certain on the real reason for property prices is going up,” he said.

“The reason why property prices are higher is a combination of interest rates, lack of supply, migration, vacancy rates and maybe taxes play a role.”

Miron was critical of recent federal housing policy changes, warning they could reduce the number of new homes being built and further constrain supply that was even highlighted in the budget.

He also highlighted the importance of the property sector to the broader economy, noting that residential real estate and related industries employed more than one million Australians.

McNeice, who advises developers on sales strategy and market intelligence, said understanding buyers had become increasingly important as affordability pressures intensified.

While affordability remained a major consideration, she said today’s buyers were focused on value rather than simply price.

“People are looking for value for money,” she said.

She said buyers were increasingly evaluating factors such as transport connections, walkability, nearby amenities and flexible living spaces that could accommodate changing family needs.

“What infrastructure is going on? Can I walk to the shops? Can I meet people at the local cafe?” she said.

The panel also discussed the mounting pressures facing developers, with Elbanna arguing that many projects become financially unviable from the moment a site is purchased.

“The viability of a development happens at the moment the site is bought,” he said.

He said rising construction costs, higher interest rates and overly optimistic feasibility assumptions had left some developers exposed as market conditions changed.

While acknowledging the growing number of smaller and first-time developers entering the market, Elbanna said property development required expertise across finance, construction, marketing and legal disciplines.

“It is actually a business that requires a level of expertise,” he said.

Looking ahead, the panel agreed opportunities remained in the market despite current challenges.

Miron said property should continue to be viewed as a long-term investment and cautioned against trying to time short-term market movements.

McNeice said success would increasingly depend on identifying projects that genuinely met changing buyer expectations.

Elbanna said affordable housing remained achievable, but developers needed to deliver more than just homes.

“We can provide affordable housing in this country,” he said.

“But we’ve got to wrap that affordable housing with the things that people want.”

As Australia’s housing affordability debate intensifies, the panellists agreed on one point: without a meaningful increase in housing supply, demand-side measures alone are unlikely to solve the nation’s property challenges.

By improving sluggish performance or replacing a broken screen, you can make your old iPhone feel new agai

A divide has opened in the tech job market between those with artificial-intelligence skills and everyone else.