Australian rents soar to record highs as housing crisis bites

The humble share house is back on the table as renters wrestle with rising rental costs

2 min

2 min

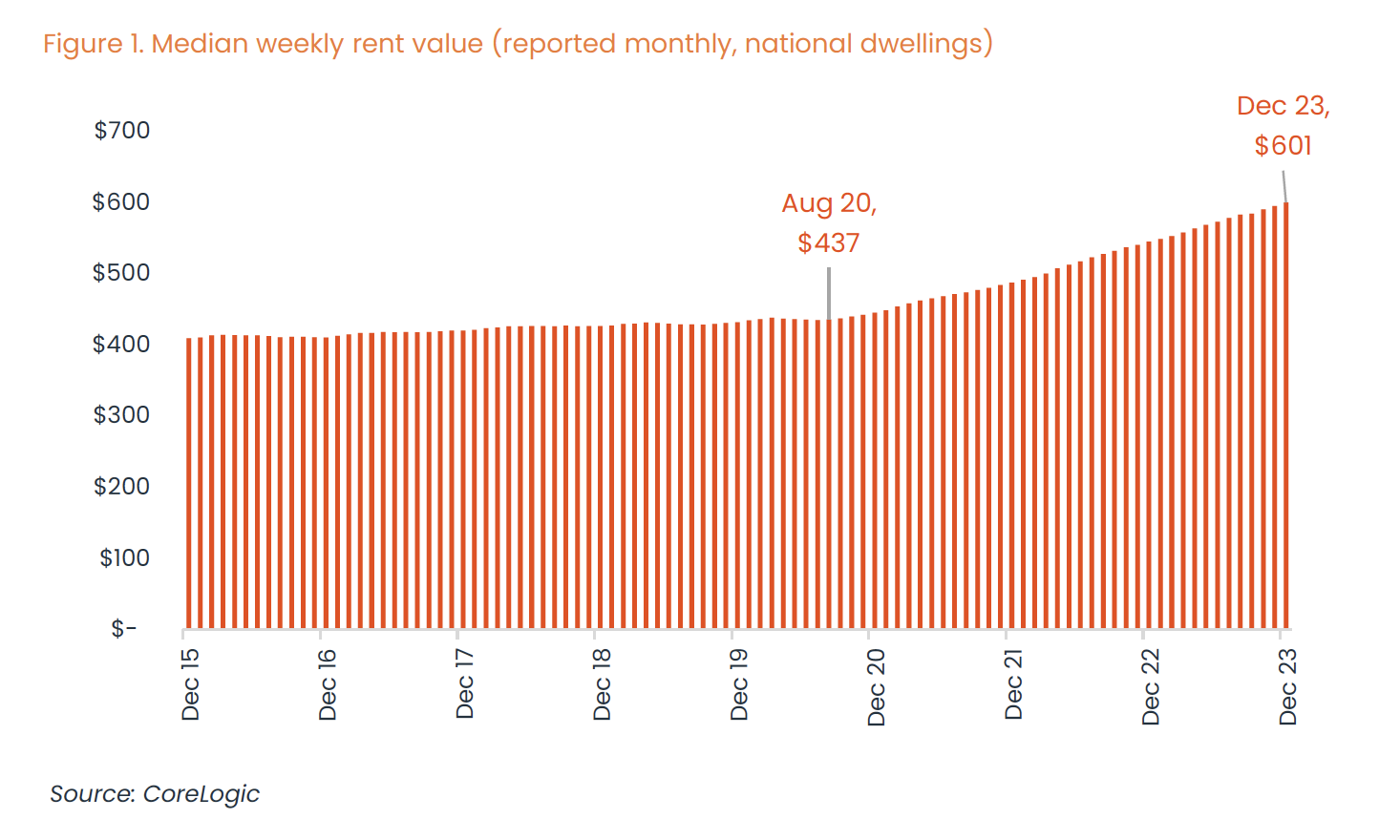

National median rents for Australians have reached record highs, CoreLogic data shows.

The median rent rose to $601 per week in December, or $31,252 a year, and increase of more than $160 since August 2020.

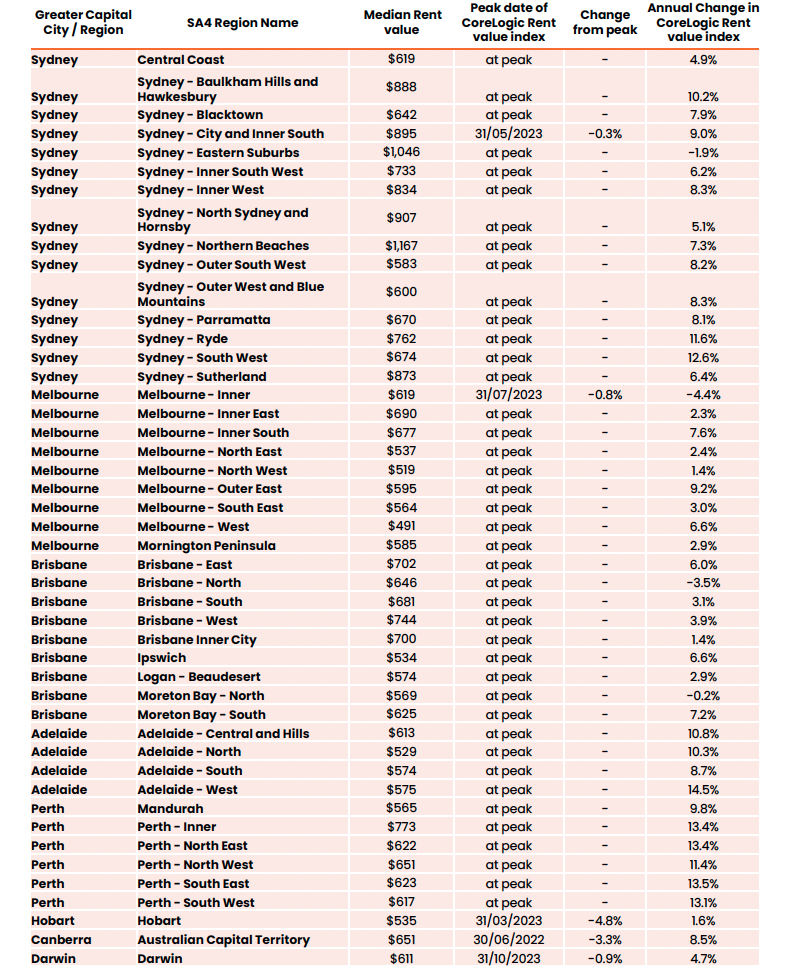

Average rent growths were 9.1 percent over the past three calendar years compared with 2 percent in the 2010s. Sydney recorded the highest median rent at $745 per week, while Hobart was the lowest at $535. Hobart recorded a -3.5 percent drop in median rents. Along with Canberra, which fell -1.9 percent, they were the only markets to experience a decline.

Author of the Rental Market Update and head of research Australia at CoreLogic, Eliza Owen, said factors such as an upswing in migration numbers since 2022 and the overall decline in the average size of households were contributing factors to the rise in prices.

It noted that the reduction in available social housing had placed further pressure on the private rental market, especially at the lower end.

While the figures are alarming to renters, the report noted that the rate of growth has slowed compared with recent years. Last year, rent values rose 8.3 percent, down from 9.6 percent in the year to September 2022. The contrast is even greater in regional areas where rents increased by 4.3 percent last year compared with 13.4 percent in the year to August 2021.

“The easing in rent growth is good news with regard to inflation, but there was a slight pick-up in annual growth once again in the final quarter of 2023,” Ms Owen said in the report. “This ‘re-acceleration’ in rents was most consistent across the capital city house markets, but was also evident in regional rent markets.”

However, she said cost of living pressures were causing some renters to re-think household arrangements.

“As noted in previous quarters, part of the explanation for an uptick in house rent growth may be in part due to households re-grouping into share houses,” Ms Owen said. “Additionally, the premium of house rents over units has narrowed in the past two years, from $63 per week at the median level to $38.

“This ‘catch up’ in unit rents could be making them less appealing, diverting tenants back to houses.”

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

Australia’s housing affordability crisis is being fuelled by chronic undersupply, planning delays and rising development costs, as politicians continue to focus on the wrong solutions.

3 min

Australia’s housing crisis will not be solved by first-home buyer incentives or tax changes alone, with leading property figures warning governments must tackle supply constraints if affordability is to improve.

Speaking at the Kanebridge Quarterly Property Leadership Summit in Sydney last week, expert project marketing specialist Sam Elbanna, property investor and fund manager Paul Miron and property consultant Karla McNeice said that a lack of housing supply remained the central issue facing the market.

Elbanna, Director of CPM Realty with more than 30 years’ experience in project sales, argued that successive governments had focused too heavily on stimulating demand rather than addressing the barriers preventing new housing from being delivered.

“The misconception is that politicians think the way to solve the housing crisis is to drive demand,” he said.

“The reality is that’s not the way. This is a supply-side problem, and it needs to be solved on the supply side.”

Drawing on his experience in project sales, Elbanna said policies designed to help first-home buyers often had unintended consequences, pointing to previous grants that ultimately flowed through to higher property prices.

Instead, he said developers were facing increasing red tape, approval delays and rising costs, which were discouraging new housing supply.

“In the absence of stock, demand exceeds supply,” he said.

Miron, a Co-Founder and Fund Manager of Msquared Capital, said the housing debate had become overly focused on tax policy while overlooking broader structural issues.

He argued that affordability challenges stemmed from a combination of factors, including planning constraints, supply shortages, migration levels and interest rates.

“No-one can be 100 per cent certain on the real reason for property prices is going up,” he said.

“The reason why property prices are higher is a combination of interest rates, lack of supply, migration, vacancy rates and maybe taxes play a role.”

Miron was critical of recent federal housing policy changes, warning they could reduce the number of new homes being built and further constrain supply that was even highlighted in the budget.

He also highlighted the importance of the property sector to the broader economy, noting that residential real estate and related industries employed more than one million Australians.

McNeice, who advises developers on sales strategy and market intelligence, said understanding buyers had become increasingly important as affordability pressures intensified.

While affordability remained a major consideration, she said today’s buyers were focused on value rather than simply price.

“People are looking for value for money,” she said.

She said buyers were increasingly evaluating factors such as transport connections, walkability, nearby amenities and flexible living spaces that could accommodate changing family needs.

“What infrastructure is going on? Can I walk to the shops? Can I meet people at the local cafe?” she said.

The panel also discussed the mounting pressures facing developers, with Elbanna arguing that many projects become financially unviable from the moment a site is purchased.

“The viability of a development happens at the moment the site is bought,” he said.

He said rising construction costs, higher interest rates and overly optimistic feasibility assumptions had left some developers exposed as market conditions changed.

While acknowledging the growing number of smaller and first-time developers entering the market, Elbanna said property development required expertise across finance, construction, marketing and legal disciplines.

“It is actually a business that requires a level of expertise,” he said.

Looking ahead, the panel agreed opportunities remained in the market despite current challenges.

Miron said property should continue to be viewed as a long-term investment and cautioned against trying to time short-term market movements.

McNeice said success would increasingly depend on identifying projects that genuinely met changing buyer expectations.

Elbanna said affordable housing remained achievable, but developers needed to deliver more than just homes.

“We can provide affordable housing in this country,” he said.

“But we’ve got to wrap that affordable housing with the things that people want.”

As Australia’s housing affordability debate intensifies, the panellists agreed on one point: without a meaningful increase in housing supply, demand-side measures alone are unlikely to solve the nation’s property challenges.

Limited to 630 units, Lamborghini’s latest Urus Capsule pushes personalisation further than ever, blending hybrid performance with over 70 bespoke design combinations.

From Tokyo backstreets to quiet coastal towns and off-grid cabins, top executives reveal where they holiday and why stepping away makes the grind worthwhile.