Buildings Are Empty, Now They Have to Go Green

Rising rates, falling occupancy and new carbon taxes hit building owners

4 min

4 min

Their buildings echo with empty offices, their borrowing costs have soared, and now owners of buildings in cities across the U.S. are facing a new tax on their carbon emissions.

Cities are toughening their climate standards and are beginning to tax buildings that don’t meet the new requirements. Landlords are left with a difficult choice between paying for expensive upgrades to reduce emissions or paying the tax.

In New York City, which has one of the first and most expensive carbon taxes, landlords of large buildings (including owners of residential buildings) beginning next year will face a $268 fine for every ton of carbon dioxide emitted beyond certain limits.

“If you’re under cash flow pressure due to lack of tenancy, adding a tax on top of that isn’t a good sign,” said Bank of America CMBS Strategist Alan Todd. “It would be potentially pretty painful.”

The Wall Street Journal tallied the potential impact of the taxes on buildings that borrowed funds from Wall Street investors by issuing mortgage-backed bonds. The Journal also looked at properties owned by three of the country’s largest publicly traded landlords. The tax bill for 128 properties analyzed could add up to more than $50 million during the first five-year enforcement period, which begins in 2024, according to the Journal’s analysis of Department of Building data and financial disclosures.

Fines for the same buildings could jump to $214 million if their landlords don’t meet the city’s emissions standards during the period between 2030 and 2034, the Journal’s analysis shows. The Real Estate Board of New York, an industry group, and engineering consulting firm Level Infrastructure said that more than 13,000 properties could face fines totaling about $900 million annually.

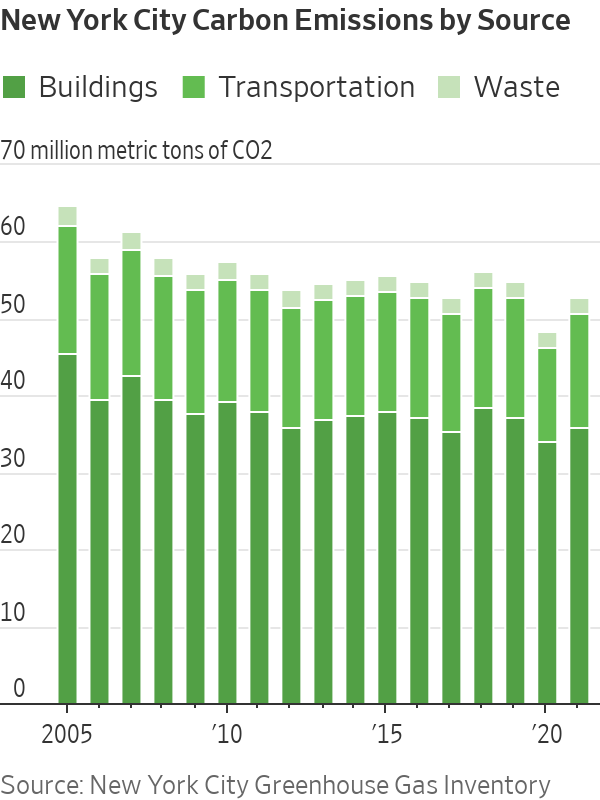

Buildings are by far New York City’s largest source of carbon emissions, which come from the fossil fuels used to heat and to provide air conditioning for them.

More than a dozen local laws regulating buildings’ carbon footprints from Chula Vista, Calif., to Boston have gone into effect since 2021 or will come online by 2030, according to carbon accounting firm nZero. Compliance also begins next year for buildings in Denver, while St. Louis properties face penalties beginning in 2025. Four other laws from Cambridge, Mass., to Reno, Nev., will go into effect in 2026.

The impact of the emissions laws initially will be small but will come on top of other, more costly problems faced by landlords. The law, based on New York’s current projections, would cost the 51-story skyscraper at 277 Park Ave. in Manhattan just $1.3 million in fines in 2024. The revenue of the building, owned by private landlord The Stahl Organization, was $129 million last year.

The building’s vacancy rate has jumped from about 2% in 2014 to 25% currently, according to commercial property data provider Trepp. JP Morgan Chase accounts for about half of the building’s space, but its lease expires in 2026. The bank is constructing a nearby tower that aims to produce net-zero carbon emissions and is scheduled to be completed in 2025. It wouldn’t comment on its leasing plans.

Stahl’s $750 million mortgage on the building is scheduled to mature next August. Stahl is now faced with potentially higher rates if it takes out a new loan, the loss of its biggest tenant and fines for carbon emissions.

Stahl declined to comment.

Shares of the three big landlords whose properties were analysed by the Journal are trading at near historic lows. Shares of Vornado Realty Trust and SL Green, each of which has about 30 New York City office buildings, are down by roughly two-thirds since before the pandemic. Boston Properties Inc., one of the country’s largest office building owners, shares are down more than 50% from before the pandemic.

SL Green faces a potential carbon-tax liability of up to $6.6 million by 2030, according to the Journal’s analysis. The company declined to comment. More than 80 other properties financed using mortgage-backed bonds reviewed by the Journal could have a nearly $27 million carbon-tax bill by 2030.

The costly upgrades needed to comply with the law will hit some properties when they are on the block or when they are trying to attract tenants, who know they will effectively be paying for any improvements. “Tenants are looking to be in a building that is greener,” said Brendan Schmitt, partner in law firm Herrick’s Real Estate Department.

The new laws coincide with big government spending on climate. Landlords can get generous subsidies for projects that reduce emissions.

Ironically, landlords are also benefiting from emptier buildings, which burn less fossil fuel. New York City says about 11% of buildings covered under the law are projected to face penalties using the latest energy data, down from 20% using earlier data.

The city’s law was passed in 2019 and included a $268 fine for every ton of CO emitted by buildings over 25,000 square feet exceeding limits. Landlords will be required to report emissions to city officials starting in 2025 with penalties based on 2024 energy use.

Some big landlords are facing fines in multiple jurisdictions including Boston Properties, which will likely get hit on properties it owns in Boston, New York and Washington, D.C. The company’s eight New York City offices could face a $2.3 million dollar tax bill by 2030, according to city data.

Ben Myers, senior vice president of sustainability at Boston Properties, said complying with local building standards is important. “We have made energy efficiency a priority,” he said.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

International AI strategist Justin Kabbani will headline the Kanebridge Property Summit in Sydney on June 18, with tickets selling fast.

Scotch whisky expert, luxury hospitality strategist and Keeper of the Quaich inductee Ross Blainey is bringing a new philosophy of luxury experiences to Citizen Kanebridge.

International AI strategist Justin Kabbani will headline the Kanebridge Property Summit in Sydney on June 18, with tickets selling fast.

2 minArtificial intelligence is rapidly reshaping business, investment and competitive advantage, and now Australia’s property industry is being told it cannot afford to sit on the sidelines.

International keynote speaker and AI strategist Justin Kabbani will headline the Kanebridge Property Summit at RACA Sydney on June 18, bringing rare insight into how forward-thinking property professionals can use AI to move faster, make smarter decisions and gain a serious edge in an increasingly competitive market.

Tickets to the exclusive summit are already selling fast.

Having worked with global brands including Uber, PepsiCo, Mattel and Destination NSW, Kabbani has become one of the leading voices on how businesses can turn AI from a buzzword into a genuine commercial advantage.

Known for his high-energy and highly practical presentations, Kabbani cuts through the hype surrounding AI and focuses on what actually matters: productivity, growth, leadership and real-world business results.

His keynote will explore how AI is already transforming industries globally, and what property developers, investors, agents and business leaders need to understand now to avoid being left behind.

Importantly, the session is designed to be practical, not theoretical.

Attendees will hear how AI can be applied across marketing, sales, operations and decision-making to improve efficiency, sharpen strategy and create new competitive advantages in a rapidly changing business environment.

The summit will also feature an exclusive roundtable bringing together leading property and finance experts for a candid, off-the-record Q&A exploring the forces shaping investment, development and wealth creation across Australia’s prestige property market.

The event follows the success of last year’s sold-out summit and will once again be hosted by respected MC John Alten.

With AI becoming one of the biggest disruptors facing business, the June 18 summit is expected to attract strong interest from property professionals, investors and business leaders looking to stay ahead of the curve.

The followings are included in every ticket:

- Full access to keynote sessions and the interactive roundtable.

- Premium selection of canapés and beverages throughout the evening.

- Complimentary annual digital subscription to two leading publications (Wall Street Journal and Kanebridge Quarterly), providing essential coverage of local and global markets, property trends and investment strategy.

Tickets are limited and selling quickly and you can buy here.

The pandemic-fuelled love affair with casual footwear is fading, with Bank of America warning the downturn shows no sign of easing.

An opulent Ryde home, packed with cinema, pool, sauna and more, is hitting the auction block with a $1 reserve.