Desperate Chinese Property Developers Resort to Bizarre Marketing Tactics

The country’s real-estate slump is getting worse—and looks set to drag on for years

3 min

3 min

China’s real-estate crisis has dragged down the economy, caused massive layoffs and pushed multibillion-dollar companies to the point of collapse.

Economists think it is about to get worse.

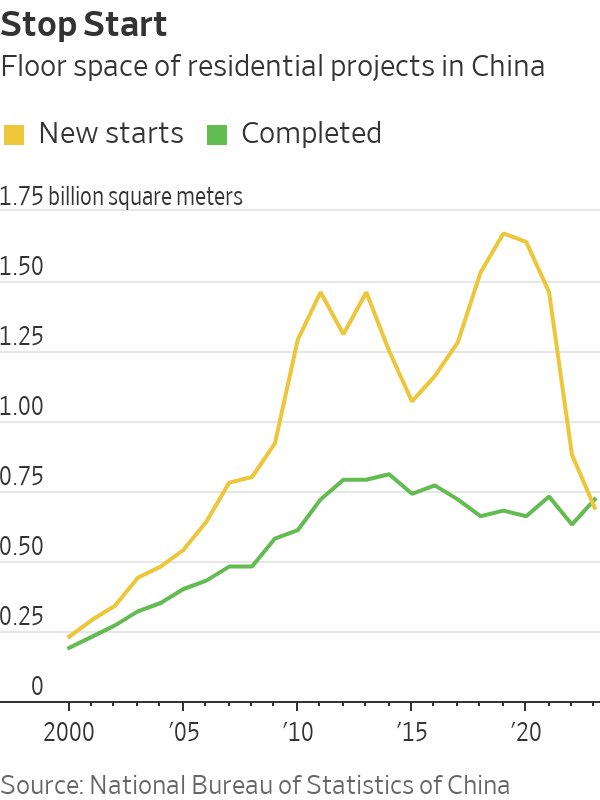

Sales of newly built homes in China fell 6% last year, returning to a level not seen since 2016, according to China’s statistics bureau. Secondhand home prices in its four wealthiest cities—Beijing, Shanghai, Guangzhou and Shenzhen—declined by between 11% and 14% in December from the year before, according to the broker Centaline Property.

Developers are starting fewer projects. Homeowners are paying back their mortgages early and borrowing less. Once-thriving property companies are stuck in protracted negotiations with foreign investors, following defaults on about $125 billion of overseas bonds between 2020 and late 2023, according to figures from S&P Global Ratings.

Chinese developers and local governments are so desperate to attract home buyers that some have resorted to bizarre marketing strategies.

A property company in Tianjin ran a video advertisement featuring the slogan “buy a house, get a wife for free.” It was a play on words, using the same Chinese characters as the phrase “buy a house, and give it to your wife”—but presented in a sentence structure typically used to offer freebies for home buyers. In September, the company was fined $4,184 for the ad.

A residential compound in eastern China’s Zhejiang province promised last year to give home buyers a 10-gram gold bar.

Earlier this month, Sheng Songcheng, former head of the statistics department at the People’s Bank of China, told a local conference that the housing downturn would last another two years. He thinks new-home sales will fall more than 5% in both 2024 and 2025.

Wall Street economists are also ringing alarm bells about how long the real-estate slump will last.

“Not too many people are buying, can buy or want to buy,” said Raymond Yeung, chief China economist at ANZ. He said there had been a fundamental shift in the way Chinese people view the property sector, with housing no longer seen as a safe investment.

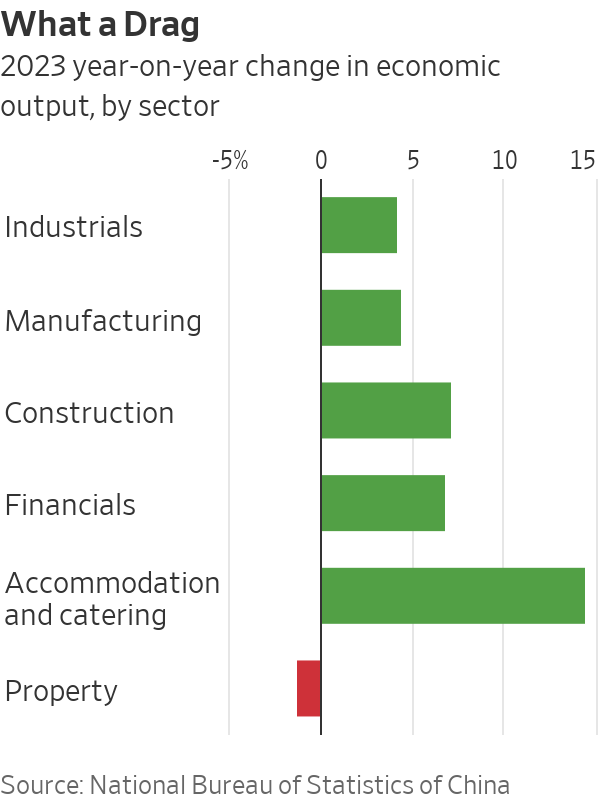

China’s real-estate sector and related industries once accounted for around a quarter of gross domestic product and the sector’s slump has been a significant drag on the world’s second-largest economy. That has increased calls for Beijing to do more to prop up the sector, but so far Chinese officials have stuck to piecemeal policies rather than introducing a landmark stimulus package.

A number of economists are making comparisons to Japan, which spent decades trying to rebound from a crash in real-estate and stock prices. China’s stock market is in a years-long slump.

China’s central bank can help make the situation less painful, but it will need to be aggressive, said Li-gang Liu, head of Asia Pacific economic analysis at Citi Global Wealth Investments. The central bank still has policy room and could take one big step to make a significant impact, he said.

Liu Yuan, head of property research at Centaline, said that without the government’s help, new-home prices will need to drop by another 50% from current levels before they reach a bottom. This is based on the assumption that the tipping point will only come when it is cheaper to buy than to rent houses, Liu said.

China’s real-estate downturn has claimed dozens of victims. More than 50 developers—mostly privately owned—have defaulted on their debt. Developers still have millions of unfinished homes that were sold but not delivered. Chinese authorities have set aside billions of dollars to help builders complete apartments but the logjam is growing.

The crisis has drained the coffers of some Chinese local governments, which previously relied on land sales as a main source of income. Economists estimate they have hidden debt worth anything from $400 billion to more than $800 billion. To quiet talk of potential defaults, the central government has set up debt-swap programs to help some of them refinance.

Some economists are optimistic. In the first half of this year, buyers of secondhand homes will gradually return to the new-home market and prop up the sector, said Helen Qiao, chief China economist at Bank of America. “Things will slowly get better from here,” Qiao said.

But most are still expecting more pain, and investors are bearish. A benchmark of Hong Kong-listed property stocks had fallen for four years in a row before the start of this year. Since Jan. 1, it is down another 15%.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

3 min

Ophora Tallawong has launched its final release of apartments, positioning itself as one of the last opportunities for buyers to secure a new Sydney home below $700,000.

The project, located in one of the city’s fastest-growing corridors, is offering rare buyer protections at a time when affordability is tightening and competition for quality stock is intensifying.

According to JLL’s Q2 2025 Apartment Market Overview, Sydney’s median apartment price has already climbed to $795,000, setting a record.

With interest rates now on a downward trend and supply still heavily constrained, experts warn that today’s price brackets may not exist next year.

Ronnie Rahme, Development Manager at KDMC, said buyers were responding to the combination of quality and value.

“You simply don’t see this level of finish at these price points anymore,” Rahme said. “That’s why demand has been so strong for this final release.”

Dr Andrew Wilson, Chief Economist at My Housing Market, says the economic drivers are clear. “High rents and higher prices continue to provide clear incentives for first-home buyers and investors chasing solid investment returns,” he told Kanebridge News.

“New government initiatives to support first-home buyers will also act to place upward pressure on prices.”

The bigger picture

JLL’s research reinforces that point. While over 15,700 apartments are expected to be delivered nationally this year, a 40% uplift on 2024, Sydney remains undersupplied, with demand continuing to outpace completions.

The report also notes that reductions in the RBA cash rate are expected to further fuel buyer activity, with constrained supply continuing to push prices higher into 2026.

With construction costs soaring, Government contributions climbing, and interest rates remaining high, projects are harder than ever to bring to market, putting upward pressure on newly completed apartments.

The pipeline of new supply is shrinking as developers delay or abandon projects that no longer stack up financially.

According to JLL’s overview, only 2,554 completions are forecast for Sydney this year – against annual demand exceeding 30,000 dwellings.

At the same time, population growth, rental demand, and first-home buyer incentives are intensifying competition for limited stock. The imbalance between constrained supply and resilient demand is leaving new apartments scarcer and more expensive across Sydney.

Ophora: Last Chance In Sydney’s northwest

Developed by KDMC and designed by Architex, the $50 million project has launched its final release, with limited availability of 81 brand-new residences from just $545,000 for a one-bedroom, or $695,000 for a two-bedroom, which is far below Sydney’s median and significantly cheaper than nearby competition.

The five-storey development at 37 Reis St, Tallawong, combines affordability with premium inclusions more often seen in luxury builds: ducted air-conditioning, timber floors, premium finishes, fridge cavities with water plumbing, video intercom systems, fibre internet, EV charging, landscaped gardens and a rooftop terrace with sweeping views.

It also comes with something almost unheard of at this price point, a 10-year Latent Defects Insurance (LDI) policy. Typically reserved for multimillion-dollar projects, LDI guarantees structural integrity for a decade and is only awarded to developers with a strong building track record.

SHC Insurance Brokers founder Stefan Hicks acknowledged the rarity of obtaining LDI, particularly for entry-level residential apartment complexes like Ophora.

“Gaining LDI is no mean feat. It’s offered selectively to developers and builders with a quality building history, and it requires both parties to employ an independent inspection service throughout construction,” he said.

“While this insurance is well-established around the world in about 40 countries, in Australia, we’re typically seeing high-end buildings covet LDI. The fact that Ophora has joined this exclusive list of quality-assured builds is a coup for entry-level home buyers.”

Raising the standard for affordable luxury

Rahme says the KDMC team wanted to set a new benchmark.

“Our mission with Ophora has always been clear: to raise the standard of what buyers should expect, regardless of budget,” he said.

“We’ve delivered a collection of apartments with finishes and features you’d usually only find in luxury projects, and we’ve backed it with one of the most stringent insurances available in the market. That gives buyers peace of mind that their investment is protected for the long term.

“People are walking through and realising you simply don’t see this level of quality at these price points anymore, as it’s effectively replacement cost in 2025.

“With rates coming down and limited competition, buyers and investors are moving quickly because they know the window won’t stay open. Investors, who have recently purchased at Ophora, have reported a strong rental demand, with minimum rental yields exceeding five per cent.”

Developments like Ophora, move-in ready, competitively priced and backed by rare structural protections (LDI), may represent the last chance for buyers to secure a sub-$700,000 apartment in Sydney.

View Ophora on cpmrealty.com.au

To arrange a private viewing or request more information, contact Sam Elbanna from CPM Realty: 0411 222 260

From Italian vegetable-tanned leather to real-world training insight, Australian brand PK9 Gear is redefining what luxury means for discerning dog owners.

As housing drives wealth and policy debate, the real risk is an economy hooked on growth without productivity to sustain it.