Is China’s Economic Predicament as Bad as Japan’s? It Could Be Worse

From demographics to decoupling, China faces challenges Japan didn’t after its 1980s bubble

4 min

4 min

HONG KONG—Starting in the 1990s Japan became synonymous with economic stagnation, as a boom gave way to lethargic growth, declining population and deflation.

Many economists say China today looks similar. The reality: In many ways its problems are more intractable than Japan’s. China’s public debt levels are higher by some measures than Japan’s were and its demographics are worse. The geopolitical tensions that China is dealing with go beyond the trade frictions Japan once faced with the U.S.

Another headwind: China’s government, which has been cracking down on the private sector in recent years, seems ideologically less inclined than Tokyo was then to support growth.

None of this means China is sure to repeat the years of economic stagnation that Japan is only now showing signs of exiting. It has some advantages that Japan didn’t. Its economic growth in coming years is likely to be well above Japan’s in the 1990s.

Even so, economists say the parallels are a warning for Communist Party leaders in Beijing: If they don’t act more forcefully, the country could get stuck in a protracted period of economic sluggishness similar to Japan’s. Despite piecemeal steps in recent weeks, including modest interest-rate cuts, Beijing has held back on major stimulus to revive growth.

“China’s policy responses so far could put it on track for ‘Japanification,’” said Johanna Chua, chief Asia economist at Citigroup. She believes China’s overall growth prospects could be slowing more sharply than Japan’s.

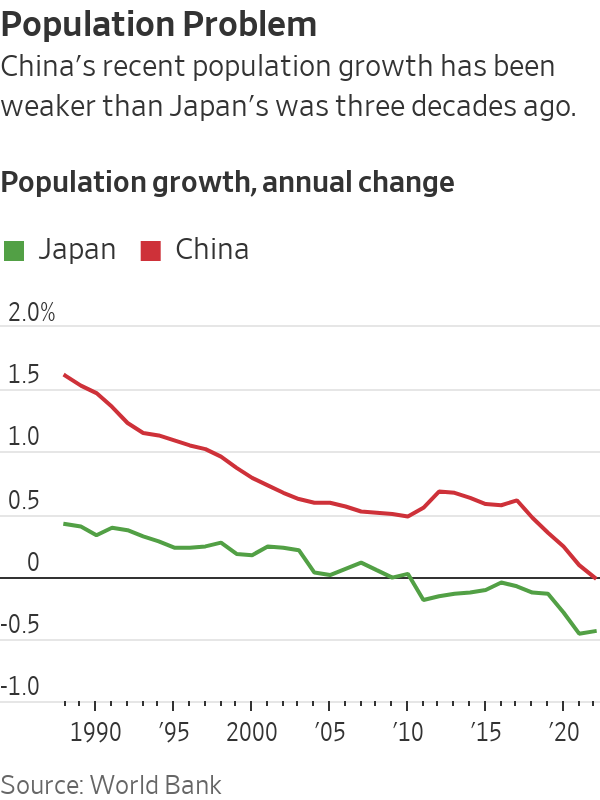

China today and Japan 30 years ago share many similarities, including high debt levels, an aging population and signs of deflation.

During a long postwar economic expansion, Japan became an export powerhouse that American politicians and corporate executives worried would be unstoppable. Then in the early 1990s, real estate and stock market bubbles burst and the economy hit the skids.

Policy makers cut interest rates to virtually zero, but growth failed to rebound as consumers and companies focused on repaying debt to repair their balance sheets instead of borrowing to finance new spending and investment.

Richard Koo, an economist at the research arm of Japanese investment bank Nomura Securities, famously coined the term “balance sheet recession” to describe the phenomenon.

China, too, has seen a property bubble pop after years of extraordinary economic growth. Chinese consumers are now paying off mortgages early, despite government efforts to get them to borrow and spend more.

Private firms are also reluctant to invest despite lower interest rates, stirring anxiety among economists that monetary easing might be losing its potency in China.

By some measures, China’s asset bubbles aren’t as big. Morgan Stanley estimates that China’s ratio of property value to gross domestic product peaked at 260% in 2020, up from 170% of GDP in 2014; home prices have only fallen slightly since the peak, according to official data. China’s equity markets hit a recent peak of 80% of GDP in 2021 and now sit at 67% of GDP.

In Japan, land values as a percentage of GDP reached 560% of GDP in 1990 before falling back to 394% by 1994, Morgan Stanley estimates. The Tokyo Stock Exchange’s market capitalisation rose to 142% of GDP in 1989 from 34% in 1982.

Also in China’s favour, its urbanisation rate is lower, standing at 65% in 2022, versus Japan’s, which was at 77% in 1988. That could give China more potential to raise productivity and growth as people move to cities and take on nonagricultural jobs.

China’s tighter control over its capital markets means the risk of a sharp appreciation of its currency, which would harm exports, is low. Japan had to deal with a sharp increase in its currency several times in recent decades, which at times added to its economic struggles.

“We believe worries on China being trapped in a balance sheet recession are overdone,” economists from Bank of America recently wrote.

Yet in other ways, China’s problems will be harder to tackle than Japan’s.

Its population is ageing faster; it began to decline in 2022. In Japan, that didn’t happen until 2008, nearly two decades after its bubble burst.

Worse, China appears to be entering a period of weaker long-term growth rates before reaching rich-world status, i.e. it is getting old before it gets rich: China’s per capita income was $12,850 in 2022, much lower than Japan in 1991 at $29,080, World Bank data shows.

Then there is the problem of debt. Once off-balance-sheet borrowing by local governments is factored in, total public debt in China reached 95% of GDP in 2022, compared with 62% of GDP in Japan in 1991, according to J.P. Morgan. That limits authorities’ ability to pursue fiscal stimulus.

External pressures also appear to be tougher for China. Japan faced a lot of heat from its trading partners, but as a military ally of the U.S., it never risked a “new Cold War”—as some analysts now describe the U.S.-China relationship. Efforts by the U.S. and its allies to block China’s access to advanced technologies and reduce reliance on Chinese supply chains have sparked a plunge in foreign direct investment into China this year, which could significantly slow growth in the long run.

Many analysts worry Beijing is underestimating the risk of long-term stagnation—and doing too little to avoid it. Moderate cuts to key interest rates, lowering down payment ratios for apartments and recent vocal support for the private sector have done little to revive sentiment so far. Economists including Xiaoqin Pi from Bank of America argue that more coordinated easing in fiscal, monetary and property policies will be needed to put China’s growth back on track.

But President Xi Jinping is ideologically opposed to increasing government support for households and consumers, which he derides as “welfarism.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

Margot Robbie may have travelled from a Queensland farm to the highest reaches of Hollywood, but a reported $28 million property deal suggests the Gold Coast has never lost its hold on her. The Australian actor and producer is believed to be the mystery buyer of Redwood, a seven-acre Currumbin Valley estate transformed into the …

Continue reading “Margot Robbie Reportedly Behind $28 Million Currumbin Valley Homecoming”

Artificial intelligence is making it easier than ever to build a business without building a team. As AI takes over coding, customer support, marketing, administration, and other day-to-day tasks, a growing number of solo founders are scaling startups to millions in revenue with few—or even no—employees. While the trend is lowering barriers to entrepreneurship, it is also reshaping hiring, raising questions about the future of work and how businesses will grow in the AI era.

5 min

Ben Broca launched a company last December that offers AI tools to entrepreneurs. He’s already added 10,000 paying customers and is on track to bring in $10 million in revenue this year.

One thing he hasn’t added: any other employees.

The 40-year-old is part of a class of entrepreneurs who are launching, and then often running, new companies on their own. Artificial intelligence tools answer Broca’s emails, help write and debug code, field requests from customers, sign up new subscribers and grant refunds when issues arise.

Broca relishes his ability to make whatever decisions he wants on his own, often from his sun-drenched Sausalito, Calif., living room. “I think compromises make lukewarm results,” he said.

Once upon a time, running a business of a certain size required a team. AI is turning that assumption upside down, and more aspiring entrepreneurs are going it alone.

An analysis by the payments company Stripe shows there are thousands of solo operators on the company’s platform that are generating over $1 million in revenue, with their ranks doubling between 2023 and 2025. The number of solo operators crossing the $10 million threshold nearly tripled in that same span.

In the past, people without business contacts or particular savvy might not have known how to get their ideas off the ground, said Ernie Tedeschi, Stripe’s chief economist. “Now, AI can be a built-in business partner,” he said.

AI’s ability to handle various administrative tasks makes it potentially useful for launching solo businesses in many fields. But the technology’s ability to also handle key tasks in tech, like coding, make that field a particular hot spot.

Analyzing Census Bureau data, Bank of America Institute economist Taylor Bowley found that among all industries, new business applications in the information sector have seen the biggest percentage increase—nearly 45%—over the past year. At the same time, the rate of information-sector applicants saying they plan to hire workers has experienced the sharpest decline of any measured industry.

This Census dataset doesn’t track solo-operated businesses. But the numbers broadly show—in tech and beyond—that applications are flat among businesses likely to hire workers, but generally rising elsewhere. Economists say that’s a strong sign that solo operators are on the upswing.

“The bar for getting started has never been lower,” said Julian Weisser, who runs a San Francisco-based accelerator for solo founders working in tech. The accelerator—which offers founders seed money and mentorship in exchange for an equity stake—attracted 4,500 applicants for 10 slots made available in its most recent cycle, nearly five times the number it drew when it launched last May.

Going it alone with AI can still be surprisingly expensive. Broca said he was losing money on many customers’ accounts while paying to access Anthropic’s Claude to run his clients’ requests—that AI company, as well as others, charges based on usage. He has since switched to free open-source AI models from China.

Broca said he has raised $30 million from investors and, at the same time, has saved millions in salary since he hasn’t needed a team of software engineers.

Another risk: If it’s easy for one entrepreneur to launch an AI-assisted business, copying them can be easy, too. This creates anxiety for founders like Troy Johnston, who runs an AI-assisted business alone in Orlando, Fla.

“Everybody has the sword and we all have the ability to unsheathe Excalibur now,” said Johnston, 40, who used AI to code an app that helps people get the most out of credit card benefits. The company makes around $3,000 a month in profit, with no employees, and is continuing to grow.

What one-person businesses will mean for the labor market remains to be seen. Polling has shown Americans are worried that AI will replace jobs, and top economists are wrestling with that possibility, too. But AI is also creating lots of new jobs, and the go-it-alone entrepreneurs show how the technology can both open doors and limit employment opportunities.

“If everyone’s hiring less, but you get four times more firms, what does that do to head count?” said Rembrand Koning, an associate professor at Harvard Business School who studies entrepreneurship. He co-authored a recent study that found that among 50,000 startups the researchers examined, those focused on AI tended to operate with 25% fewer employees.

Koning also believes a soft hiring environment that’s left some people mired in long job searches has encouraged more to try their hand at launching businesses.

Some founders cite different motives. “It’s a perfect storm of post-pandemic burnout and a re-evaluation of one’s priorities, and also booming AI and a sense of what’s possible,” said Samir Ahmad, 39, who lives in Breinigsville, Pa.

Two years ago, Ahmad decided to leave the corporate job he had worked at Verizon for almost two decades to start a solo coaching and consulting business. He had been seeing social-media posts touting the ease and virtues of AI, which he used to chart a business plan and help with marketing. “It was like my chief of staff, a second in command,” he said.

The business ultimately petered out within months, though, and Ahmad is now back to a full-time corporate role with a utility company.

For Claire Vo, 41, AI helped her turn a passing impulse into a business. She was working full-time as a tech executive when she tapped AI in late 2023 to help code an app that would help her manage documentation and design for new products, with customers ranging from financial services to healthcare firms.

“I was copying and pasting from ChatGPT,” said Vo, who lives in San Francisco.

She put the app online for $1 a month, and within weeks people downloaded it thousands of times. Nearly three years later, Vo’s company—which she ran solo for nine months before hiring an engineer—now has 100,000 users and is on track to make seven figures in profit this year. AI handles the company’s marketing, sales and customer support.

While AI is a shortcut, Vo said her network and credibility in the industry were key. “I think people over-index on how easy AI is and under-index on how much I did to get to this point,” she said.

In the remote waters of Indonesia’s Anambas Islands, Bawah Reserve is redefining what it means to blend barefoot luxury with environmental stewardship.

A cluster of century-old warehouses beneath the Harbour Bridge has been transformed into a modern workplace hub, now home to more than 100 businesses.