London’s Canary Wharf Takes Brunt of Real-Estate Pain

Empty offices, remote working and corporate tenants fleeing to buzzier areas hit the 30-year-old business district

4 min

4 min

LONDON—Three decades ago, London remade a derelict shipping yard at Canary Wharf into a forest of glass-and-concrete skyscrapers in a bid to mimic U.S. financial hubs.

Now the 128-acre banking district east of central London is suffering a problem also plaguing U.S. cities: emptying office buildings.

Last month, HSBC Holdings, the U.K.’s largest financial firm, said it was leaving its 1.1-million-square-foot headquarters, known as the HSBC Tower, for a smaller building in central London. The move followed a decision by law firm Clifford Chance to relocate to central London and major office-space downsizings by Barclays and Société Générale, among others.

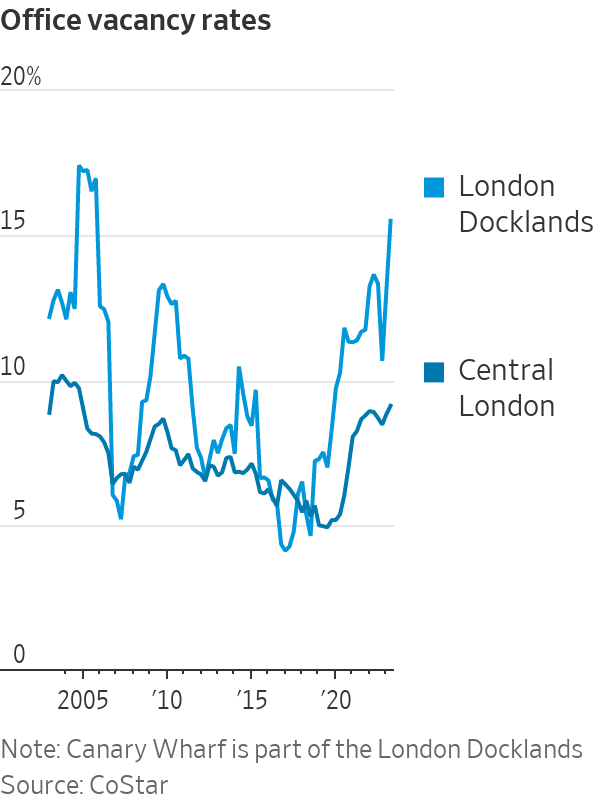

Already, Canary Wharf and its surrounding area have an availability rate of 17.1%, roughly the size of an empty Empire State Building, compared with 10.7% for central London, according to data provided by UBS.

Bonds for Canary Wharf Group—the company that owns most of the buildings in the area—are trading at a deep discount, with yields over 16%. Moody’s lowered its credit rating to junk last month.

The troubles at Canary Wharf show how the rapid rise of remote work has reverberated unevenly across global property markets. While the hollowing out of skyscrapers has become a familiar theme in U.S. cities since the pandemic, Europe’s office market has held up relatively well, as workers have been far more eager to return to the office.

But London has some problems that are familiar to American real estate.

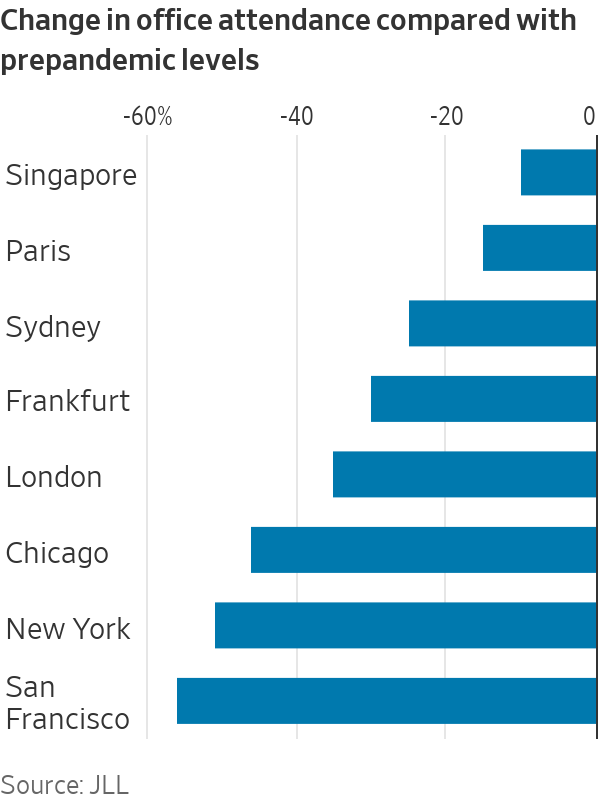

The return-to-office rate for London stood at 65% in February, a figure that put it between New York City, which stood at 49%, and Paris, which was at 85%, according to JLL, a property-services company.

Canary Wharf has caught the brunt of the problems in London’s office market.

Work-from-home and the cost of upgrading old office space to meet environmental regulations “puts Canary Wharf at a disadvantage,” said Zachary Gauge, head of European real-estate research at UBS.

Canary Wharf was a byproduct of a changing London economy in the 1980s. Transformations in global shipping decimated the city’s sprawling blue-collar dockyards, the West India Docks. Margaret Thatcher’s government deregulated the financial industry in a move known as the “big bang,” and banks were hungry for towers that were larger than low-slung London’s standard fare.

While it wasn’t a great property investment—the original developer went bankrupt—skyscrapers sprouted through the 1990s and Canary Wharf became a rare slice of Manhattan in London.

Canary Wharf attracted tenants from London’s traditional financial district, known as the City of London, which lies several miles west. It became a global byword for urban renewal. Former New York Mayor Michael Bloomberg made it his go-to analogy when promoting plans for Hudson Yards in the late 2000s.

“Canary Wharf beat out the City in the 1990s and 2000s because it catered to American firms who wanted high-rise buildings for high-skilled labor,” said Anthony Breach, an analyst at the Centre for Cities, a think tank.

A generation later, its towers are far from new, while sleek modern skyscrapers have shot up in the buzzier streets of the City and other parts of central London.

“High rates of work from home means that employers need to offer some desirability and vibrancy to bring workers back,” said Marie Dormeuil, an analyst at Green Street, a commercial-real-estate advisory firm.

Top-end commercial-property rents in London’s more fashionable West End rose 8% a year over the past three years, buoyed by hedge funds and private-equity firms piling into Georgian townhouses, while rents in Canary Wharf have mostly stayed the same, according to Green Street. Average office-space rent in Canary Wharf is $69 a square foot, compared with $95 in the City and more than $165 in the West End, according to data from Knight Frank, a U.K. real-estate brokerage.

With most of the district held by Canary Wharf Group—a joint venture between Qatar’s wealth fund and private-equity giant Brookfield—or by the Qatari fund directly, the development has space for long-term planning. “The Canary Wharf Group is very good at making its own weather,” said Tony Travers, who directs the London School of Economics’ London centre.

Shobi Khan, Canary Wharf Group’s chief executive, has outlined a plan for a “Canary Wharf 3.0” that would thrive off of residential rents, entertainment offerings and biotech.

The group plans to construct a 750,000-square-foot life-sciences centre, which it says will be the largest commercial lab in Europe. Rents in the sector can bring in a 70% premium compared with office space, according to Savills, a British real-estate-services company.

As for the residential sector, 3,500 people inhabit the group’s 2,200 units there, compared with zero tenants three years ago. Two thousand more units are under construction.

A combination of high-end retailers, restaurants and music and arts festivals have brought in extra revenue. Foot traffic on evenings and weekends is up by 50% compared with pre pandemic levels, according to data from the city’s transport authority.

But a full makeover will be a difficult task to pull off. Higher interest rates and lower revenue mean that Qatar and Brookfield may need to put up more cash to cover the costs of refurbishment and construction.

Another risk: Fewer financiers and lawyers could mean little demand for the stores and amenities. “You could see a downward spiral as people start to leave,” said Breach, the think tank analyst.

The developers will likely need to lure in lots of people like Justin Walker, a tax accountant who works in JPMorgan Chase’s office there.

“I hated how sterile Canary Wharf looked when I first got here,” he said, “But, the place has grown on me, it’s more residential now, and a lot more vibrant.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Automobili Lamborghini and Babolat have expanded their collaboration with five new colourways for the ultra-exclusive BL.001 racket, limited to just 50 pieces worldwide.

As housing drives wealth and policy debate, the real risk is an economy hooked on growth without productivity to sustain it.

Italian wines are emerging as a serious contender for Australian collectors, offering depth, rarity and value as French benchmarks continue to climb.

2 min

From office parties to NYE fireworks, here are the bottles that deserve pride of place in the ice bucket this season.

Here’s how they are looking at artificial intelligence, interest rates and economic pressures.