The Home Buyer’s Quandary: Nobody’s Selling

Many are ready to move but don’t want to lose the low-rate mortgages they locked in a few years ago, crimping the supply of homes and keeping prices high

7 min

7 min

Many Americans who want to move are trapped in their homes—locked in by low interest rates they can’t afford to give up.

These “golden handcuffs” are keeping the supply of homes for sale unusually low and making the market more competitive and pricey than some forecasters expected.

The reluctance of homeowners to sell differentiates the current housing market from past downturns and could keep home prices from falling significantly on a national basis, economists say. This could dull the Federal Reserve’s efforts to slow inflation by cooling the economy.

Emily and Isaac Naatz of Cottage Grove, Minn., a suburb of St. Paul, had a baby last year and want a bigger place. They have lived for more than four years in their two-bedroom townhouse, and they now want a three- or four-bedroom house with a yard and space for a home office. “You get four people in here…and it feels like a large crowd,” Mr. Naatz said.

But they locked in a 30-year fixed mortgage rate of 3.4% in 2021—and don’t want to give that up to take on a new mortgage with a rate about 3 percentage points higher, especially when home prices in their area haven’t come down much.

The type of home they would want to buy would cost them about $1,100 a month more than they currently pay, Mr. Naatz said. “I don’t feel comfortable paying what I still think is an inflated price for a home, and on top of it paying twice the interest rate,” he said.

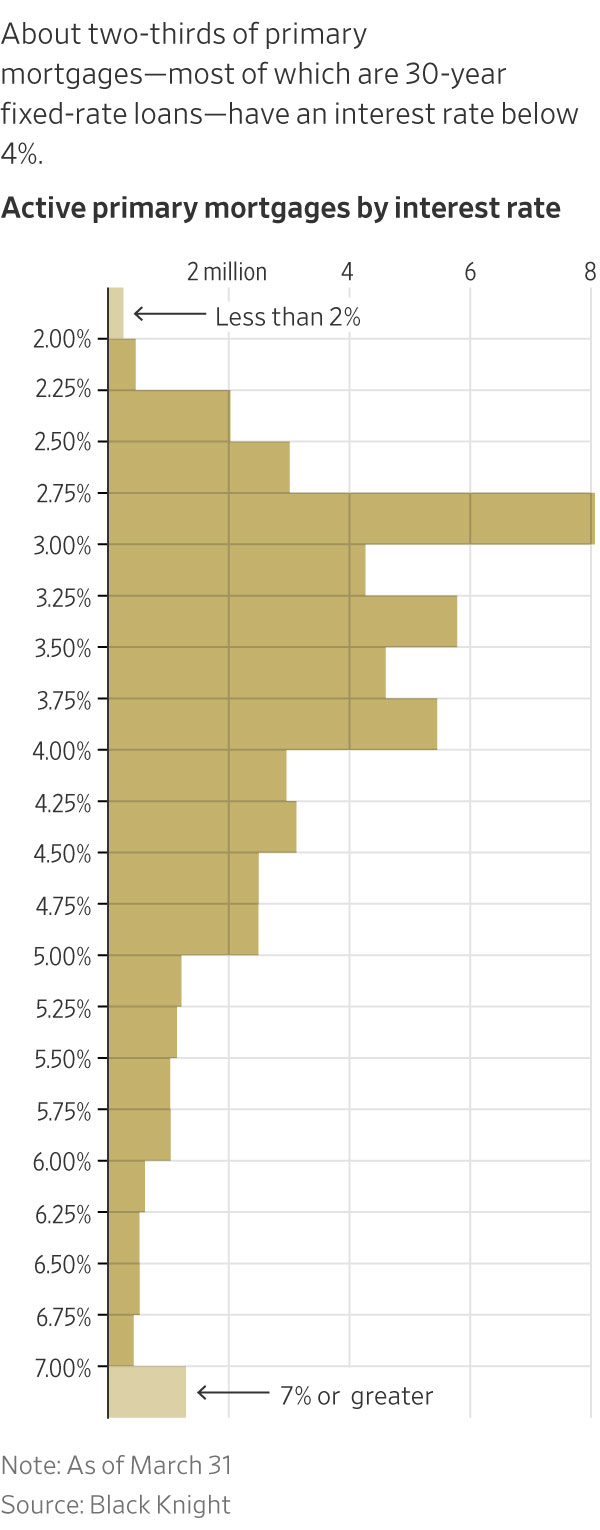

As of March 31, nearly two-thirds of primary mortgages had an interest rate below 4%, according to mortgage-data firm Black Knight. About 73% of primary mortgages have fixed rates for 30 years, Black Knight data show. The average rate for a new 30-year fixed mortgage was 6.39% in the week ended May 4, according to Freddie Mac.

The mortgage-rate factor is leaving some people in houses that aren’t a good fit, whether it’s a growing family without enough bedrooms or ageing homeowners with too much space, or dissuading people from relocating for jobs or other opportunities. Some people that wanted to sell in 2022 or 2023 shelved their plans.

As current homeowners stay put, “the movement up the ladder is sort of grinding to a halt,” said Sam Khater, chief economist at Freddie Mac. “It’s getting much harder for first-time home buyers to jump into the market because of the lack of supply.”

Half the listings

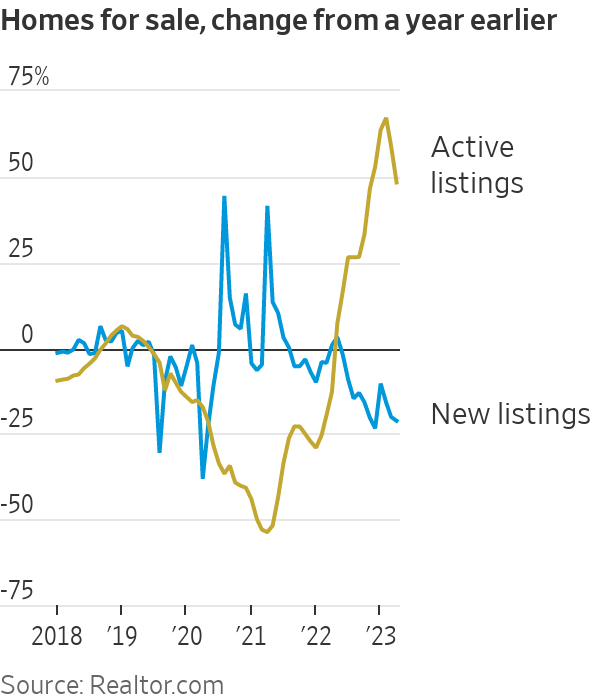

In April, there were about half as many homes for sale as in April 2019, though there were more listings than in April 2022, when they were near record lows, according to Realtor.com.

The number of homes newly listed on the market in April fell about 21% from a year earlier, an indication that sellers are holding back even during the normally busy spring home-buying season.

The constrained inventory is a key reason why home prices haven’t fallen much, even though higher mortgage rates have pushed many buyers to the sidelines.

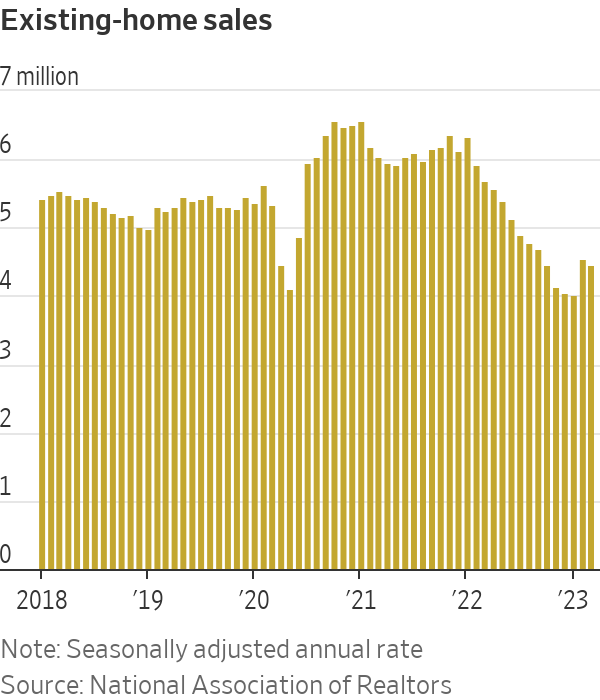

The median existing-home sale price in March slid 0.9% from a year earlier, according to the National Association of Realtors. Existing-home sales, meanwhile, fell 22% in March from a year earlier.

It’s a “unique market condition,” said Lawrence Yun, NAR’s chief economist. “Sales are down and even prices are down in some areas, yet from a buyer’s perspective it’s hard to get that home, because they are competing with other buyers.”

Frenzied bidding wars are still common in parts of the country, especially for moderately priced homes that appeal to first-time home buyers. In Clifton, N.J., a New York City suburb, a two-family house that listed for $449,000 in early April received 120 offers in six days, said Mahmoud Ijbara, the real-estate agent who listed it. The house is under contract for about $150,000 over the asking price, he said.

“The low inventory is what’s driving the prices up,” he said. “A lot of buyers are really panicking right now.”

A healthy housing market has between four and six months of supply at current sales rates, economists say. The existing-home market, which makes up most of the housing market, hit a record low 1.6 months’ supply in January 2022 and stood at 2.6 months’ supply in March of this year, according to NAR. The smaller new-home market is more amply supplied, at a seasonally adjusted 7.6 months in March, according to the Commerce Department.

The shortage of supply in the housing market has been a growing issue for years. Following the subprime-mortgage crisis, many builders went out of business and others sharply cut back on spending and new construction.

The problem worsened starting in 2020, when record-low mortgage rates and a pandemic-driven increase in remote work prompted buyers to rush into the market and snap up primary homes, vacation homes and investment properties. Home builders ramped up construction but struggled to meet demand due to volatile material costs, labor shortages and supply-chain issues.

That sales boom, along with a huge wave of homeowners who refinanced their mortgages, locked in millions of homeowners to low-rate, long-term loans. Among people planning to sell their homes and buy new ones in the next 12 months, about 56% plan to wait for rates to decline, according to a Realtor.com survey conducted in February. (News Corp, parent of The Wall Street Journal, operates Realtor.com.)

The Fed has been working to slow inflation. It raised its benchmark federal-funds rate last week for the 10th time since the start of 2022 but signalled it might be done raising rates for now.

Housing is one of the most rate-sensitive economic sectors, and the housing-market slowdown since early 2022 has been one of the main ways that the Fed’s actions have directly affected consumers.

Even some people who can accept higher mortgage rates are staying put because they are struggling to find something to buy. Julie and Aidan Booth expected to live in their three-bedroom home in East Rutherford, N.J., for about five years when they bought it in late 2019. Since then, they’ve had a second child and both switched to fully remote and hybrid working schedules, prompting them to want more space sooner than they expected.

The family started house hunting at the start of the year. They would be able to afford a higher mortgage rate, Mrs. Booth said, but they are stymied by the lack of supply.

“The last three weeks, there has been nothing new in our town” that met their criteria, she said. “There’s just no inventory.”

Opening for builders

The housing scarcity is good news for home builders, who struggled to find customers for much of 2022 with mortgage rates rising but reported stronger-than-expected demand in the first quarter. Newly built homes made up about one-third of total single-family homes for sale in March, up from a historical norm of 10% to 20%.

“If somebody does want a home at [either higher or lower price points], new construction is where they can find it right now,” said Jessica Hansen, vice president of investor relations and communications at D.R. Horton, the biggest home builder by volume, in an April earnings call.

The current market could also be a boon to remodelling companies. Rachael and Aaron Wyley, who have owned their Sacramento, Calif., house for almost 10 years, have considered moving to another house with space for Mrs. Wyley’s mother. But prices were either too high or mortgage rates too steep. Instead, they are saving up to remodel to add an in-law unit.

“We would break down the math of it and look at what we would put down, on top of how much we would get from the house selling,” Mr. Wyley said. “We’d have enough to make the monthly payments but not much else.”

There will always be homeowners who have to move due to life events like death, divorce or job relocations, and others who don’t view current mortgage rates as an obstacle. Many retirees and remote workers opt to move to cheaper housing markets, where lower prices can offset the effect of higher rates. About 38% of owner-occupied housing units have no mortgage, according to Census Bureau data. And about 27% of March existing-home sales were purchased in cash, according to NAR.

Many homeowners who have lived in their houses for years have also built up equity they can use toward down payments on their next homes, reducing the size of their loans. U.S. homeowners had $270,000 more equity on average in the fourth quarter of 2022 than they did at the start of the pandemic, according to CoreLogic.

How long the mortgage rate lock-in effect will last is hard for economists to say. Mortgage rates have never climbed as quickly as they did in 2022.

As the gap widens between homeowners’ existing mortgage rates and the prevailing rate, moving slows down, according to a March working paper by Julia Fonseca at University of Illinois at Urbana-Champaign and Lu Liu at the University of Pennsylvania’s Wharton School. The paper also found homeowners with low locked-in mortgage rates are less likely to relocate for higher-paying jobs.

Ryan and Megan Carrillo bought their first home in Phoenix in 2020 for $320,000, locking in a 2.75% fixed mortgage rate for 30 years.

Last year, after Mr. Carrillo got a higher-paying job, they wanted to upgrade to a nicer house in the $600,000 to $700,000 price range. When they started looking in January 2022, they planned to pay about $3,000 a month for a new house, but they backed out of the market after their expected payments ballooned to more than $4,000 by September.

The Carrillos now plan to stay in their house for about five more years and then turn it into a rental property when they move out of state.

“I’d love to keep it forever and not sell it,” Mr. Carrillo said. His ultra low mortgage rate, he added, is “too good to give up.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

Sydney Children’s Hospitals Foundation CEO Kristina Keneally says Australia’s culture of large-scale philanthropy is becoming more sophisticated as Gold Dinner raises $75.5 million for children’s health, research and innovation.

3 min

Australia’s wealthiest donors are becoming more strategic, more ambitious and increasingly focused on creating measurable impact, according to Sydney Children’s Hospitals Foundation chief executive Kristina Keneally.

Speaking after the 2026 Gold Dinner, held last week in Sydney, Keneally said Australia was experiencing a significant shift in how major philanthropy is viewed, with large-scale giving increasingly part of conversations about leadership, legacy and social impact.

The annual Gold Dinner, now in its 29th year, brought together some of the country’s most influential business leaders, philanthropists and cultural figures, raising $75.5 million and counting in support of the Sydney Children’s Hospitals Network.

While the event has become one of Australia’s most prestigious fundraising gatherings, Keneally said its significance extends far beyond a single evening.

“Gold Dinner, the flagship event of Sydney Children’s Hospitals Foundation, represents far more than a single evening. It is a powerful demonstration of what a committed community can achieve together over 12 months,” she said.

“The strength of that community, and the trust built over nearly three decades, means people return not just for the event, but for the impact they know it delivers.”

A NEW ERA OF PHILANTHROPY

Large-scale philanthropy has long been a feature of American society, where charitable foundations and major donors often play a prominent role in funding medical research, education and social programs.

Keneally believes Australia is moving in a similar direction.

“Australia is building a stronger culture of large-scale philanthropy, but it is still evolving compared to the United States, where giving at scale is more deeply embedded and widely recognised,” she said.

She said the country’s philanthropic landscape was becoming more sophisticated as successful business leaders increasingly sought opportunities to create meaningful change through their giving.

“In Australia, while generosity has always been strong, large-scale giving has historically been less visible, but that is changing rapidly as more leaders embrace philanthropy as a powerful way to drive meaningful outcomes.”

According to Keneally, events such as the Gold Dinner are helping reshape public perceptions of philanthropy by demonstrating the tangible outcomes that major donations can achieve.

“Gold Dinner is helping to reshape how philanthropy is perceived in Australia, making it more visible, more aspirational and more connected to real-world outcomes,” she said.

WHERE THE MONEY GOES

The funds raised through Gold Dinner support clinical care, research and innovation across the Sydney Children’s Hospitals Network.

Over the past 12 months, more than $75.5 million has been raised to help fund advanced medical equipment, innovative care models and world-leading medical research. Areas of focus include precision medicine and early diagnosis, where emerging technologies are already changing how childhood illnesses are detected and treated.

Keneally said the impact is felt directly by children and families facing some of the most difficult moments of their lives.

“For children and families, this translates into very real and immediate impact. It means faster diagnoses, earlier access to life-saving treatments, and care that is more personalised and effective,” she said.

“It also ensures hospitals are equipped not just to respond to illness, but to reimagine what care can look like, giving children the best possible chance not only to survive, but to live full, healthy lives.”

BUSINESS LEADERS BACKING CHANGE

One of the defining characteristics of Gold Dinner is the calibre of its supporters.

The event has evolved into a meeting point for influential leaders from business, culture and philanthropy, many of whom see charitable giving as an extension of their professional and personal legacy.

“It speaks to a community that is not only generous, but increasingly ambitious in how it gives, combining influence, expertise and purpose to achieve outcomes at scale,” Keneally said.

Among the major supporters of this year’s event were Presenting Partner, John-Paul Nassif Foundation; Major Partners, ABC Bullion, Shaw and Partners Financial Services and One Circular Quay by Lendlease; and Premier Partner, Range Rover, whose ongoing support reflects a shared philosophy of legacy and long-term impact.

The evening also featured performances, premium hospitality experiences and fundraising initiatives designed to encourage further support for children’s health services and research.

LOOKING BEYOND NEW HOSPITALS

With major new children’s hospital developments at Randwick and Westmead progressing, Keneally said the focus is increasingly turning towards what comes next.

“The long-term vision is to ensure every child has access to world-leading healthcare, care that continues to evolve through innovation, research and global collaboration,” she said.

The foundation’s future priorities include accelerating medical discovery, expanding access to cutting-edge treatments and helping position New South Wales as a global leader in children’s health.

Keneally said the Gold Dinner remains central to achieving those ambitions because it does more than raise money.

“Gold Dinner is critical to making that vision possible. It not only provides significant funding, but also unites a powerful network of supporters who are driving the future of philanthropy in Australia,” she said.

As Australia’s culture of philanthropy continues to mature, Keneally believes that the network will play an increasingly important role in shaping the future of healthcare for generations to come.

“The result is a community that is helping to shape the future of paediatric care, not just for today’s patients, but for generations to come.”

From the shacks of yesterday to the sculptural sanctuaries of today, Australia’s coastal architecture has matured into a global benchmark for design.

Sydney Children’s Hospitals Foundation CEO Kristina Keneally says Australia’s culture of large-scale philanthropy is becoming more sophisticated as Gold Dinner raises $75.5 million for children’s health, research and innovation.