The Luxury Home Market Confronts Its New Reality: Not Enough Buyers and Sellers

Sales at the high end continue to decline, as homeowners pull back on listing properties and would-be buyers grapple with high interest rates and recession fears

8 min

8 min

When Joan Dangerfield, wife of the late comedian Rodney Dangerfield, first walked into her Los Angeles home in the early 2000s, she knew immediately that she would buy it. The Art Deco-style estate, perched in the coveted Bird Streets above L.A.’s Sunset Strip, had dramatic views spanning Downtown Los Angeles to the ocean and Catalina Island.

“I stepped 3 feet into the house and I knew it was the place for me,” said Dangerfield, who paid $6.25 million for the property. “It swept me away.”

Roughly two decades later, Dangerfield, 70, is trying to sell the home—and finding that would-be buyers aren’t as eager as she once was. The $17.8 million listing for her property has been active since February and while she has received several full-price offers, they have come with complicated contingencies, such as requiring her to provide seller financing, she said.

“I figured it would sell in a week, but didn’t quite work out that way,” she said of the house, which is comparably priced with other homes in the area. “It was a shock for me to just watch it sit there on the market.”

Luxury sellers across the country are finding themselves in similar circumstances, as the high-end real-estate market faces a perfect storm of rising interest rates, recession fears and population shifts in the wake of the Covid-19 pandemic.

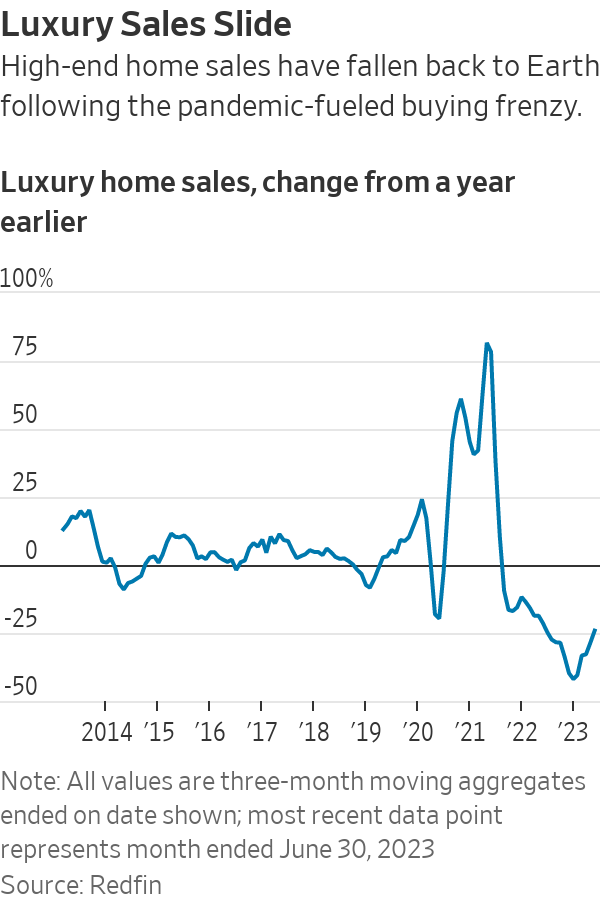

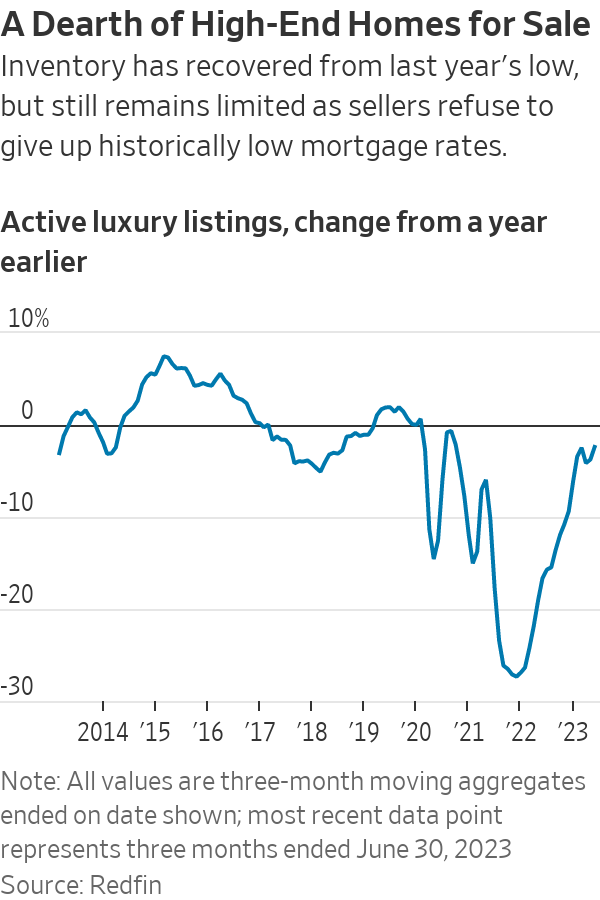

Sales of luxury homes nationwide, defined as the top 5% of homes based on estimated market value, declined by 24.13% in the three months ended June 30, compared with the same period last year, according to a new report by brokerage Redfin. Inventory of luxury homes was down 2.39% during that same period, while the median sales price for a luxury home was up by 4.55%. In many metros, homeowners appear to have pulled back on listing homes in light of the market shift. New luxury listings were down by 17.08% year-over-year in the three months ended June 30, Redfin’s data shows.

Sales of non luxury homes also fell during the same period, but that drop—19.42%—was smaller than the decline in the luxury market, according to Redfin.

“The luxury market is definitely hurting in terms of transactions,” said Daryl Fairweather, Redfin’s chief economist. “Even when you compare it to the rest of the market, it’s looking like luxury has really cooled off.”

The report marks the continuation of a market slide that began in earnest last spring, following an unprecedented deal-making frenzy during the pandemic. Redfin’s data shows that sales began to plummet significantly as early as June 2022, as buyers began to grapple with inflation and a volatile stock market. In the first quarter of 2023, luxury sales volume was down by 33.3% year-over-year.

Some of the biggest drops in sales volume over the three months ended June 30 were in markets that seemed unstoppable during the pandemic. The Miami metro area saw the largest drop in activity, for instance, with a 40.14% year-over-year reduction in luxury transaction volume for the three months ended June 30, according to Redfin.

Other metro areas with large drops included Nassau County on New York’s Long Island, where luxury sales volume dropped 39.34% year-over-year, followed by New York City, down 35.98%, Los Angeles, down 36.17%, and Chicago, which was down 34.13%.

Real-estate agents and industry experts said the luxury market’s performance has been uneven. That often comes down to pricing: In areas where sellers have capitulated to the declining market and dropped prices, transaction activity is holding relatively steady. But in markets where sellers are clinging to pandemic-era prices, activity has taken a nosedive.

In the San Francisco area, for instance, where median sales prices for luxury homes were down by 12.73%, there was only a 4.04% drop in transaction volume. “Because the prices have fallen, it’s opened up the opportunity for people who say, ‘I might finally be able to buy,’ ” Fairweather said.

In contrast, in markets like New York, Chicago and Los Angeles, prices have remained consistent or even risen slightly from last year, but transaction activity is way down. “There’s less demand, but it’s not enough of a pullback in demand to draw down prices,” Fairweather said.

In Miami, industry insiders say it is lack of supply, not lack of demand, that has caused the drop in activity. That’s thanks in large part to the mass migration to Miami and buying frenzy during Covid. “People who are going to sell have already sold,” Fairweather said, noting that new luxury listings in the Miami area were down by 33.1% year-over-year in the three months ended June 30. “There are definitely people who are moving to Miami who want to buy homes, but there are not necessarily homes for sale.”

Heigo Paartalu is among those buyers frustrated by a lack of inventory properties.

Paartalu, a Cigarette boat dealer and CEO of YachtWay, a digital boat show company, said he and his wife purchased a modern, five-bedroom house on Hibiscus Island, a gated island in Miami Beach, for $6 million in late 2021. The home value shot up 25% after about a year, so they cashed out and sold the house for $7.5 million in early 2023. Now, with a budget of around $10 million, they are looking for a waterfront property in the area without luck. “The inventory is very low and we’re not seeing the prices come down, which is what we were hoping for,” he said. The couple is currently renting in Miami’s Edgewater neighbourhood for $24,000 a month.

Jeff Miller of ONE Sotheby’s International Realty, Paartalu’s broker, said some homeowners aren’t selling because prices have gotten so high they won’t be able to buy something else in the area. Others don’t want to walk away from low mortgage rates. “It’s creating a huge shortage in our supply of available inventory and homes,” he said.

Even with a limited supply of inventory in Miami, Dina Goldentayer of Douglas Elliman said buyers have more leverage than they did last year for things like home inspections and closing credits. “I’m no longer taking the position of, ‘Take it or leave it,’ ” she said. “There are clear shifts that are making it seem like a normal market.”

In Los Angeles, the issues in the luxury market go far beyond an inventory crunch. Real-estate agent Juliette Hohnen of Douglas Elliman estimated that her business is down roughly 50% in that market from this time last year. At the height of the pandemic-fuelled market, she said, she had signed as many as 10 deals in a month. This July, she has only one so far. She chalked up the drop to rising interest rates, an outward migration from Los Angeles to lower-tax states, the introduction of a new mansion tax and more recently, the strike by both the actors’ and writers’ unions. She said she was slated to show an Oscar-winning writer around L.A. homes this month, but he called off his search in favour of renting amid the strikes.

The rising interest rates are keeping inventory low and stymying sales activity, Hohnen said. “Anyone who bought in the last few years has got these crazy low interest rates, usually between two and three percent,” she said. If those buyers sell now, they’ll be incurring rates that are almost double and potentially taking a loss on the sale.

Hohnen said she bought a $2.525 million home in 2021 in the Sag Harbor area of the Hamptons, securing an interest rate of just 1.875% for an adjustable-rate mortgage. Normally, she would buy, renovate and flip, but not this time, she said. “I’m never going to sell that house. I could never afford it if I was buying now. The monthly expenses on a new house would be too high.”

Dangerfield said she didn’t foresee how detrimental the mansion tax would be for her home’s prospects. The new measure, which was implemented April 1, requires sellers to pay 4% on sales of homes priced between $5 million and $10 million, and 5.5% on sales of properties at $10 million or above. “We were flooded with shoppers in March. Then, things just came to a screeching halt. It was such a change in the amount of people coming to view the home that it felt like it wasn’t even on the market,” she said.

One of Dangerfield’s agents, Marcy Roth of the Eklund Gomes team at Douglas Elliman, said the ULA tax “tainted buyer sentiment,” especially when combined with other issues like rising interest rates. “Everything is muddy and offers are complicated,” she said. “There aren’t a lot of quick, clean deals.”

In Chicago, real-estate agent Katherine Malkin of Compass said the city’s downtown area and so-called Gold Coast have been most affected by the slowdown. She said quality of life concerns like crime and an outward migration of some of the city’s businesses has put a damper on sales. Citadel, for instance, the hedge fund headed by billionaire Ken Griffin, recently left the city and moved to Miami. Other businesses that recently relocated their headquarters from Chicago include Boeing.

“You have businesses that are leaving because of the taxes,” Malkin said, noting that some prominent Chicago philanthropists and entrepreneurs have also left the city in the past few years. “They went to Florida, they went to Texas, they went to states that had a much lower tax circumstance. That’s been a difficult thing for people to grasp.”

Some sellers, Malkin said, have been reluctant to lower prices significantly—median luxury sales prices were actually up by more than 6.82% in Chicago in the three months ended June 30—which has been a further drag on sales. “No person of means wants to give their property away when they feel that they’ve invested in it,” she said.

When sellers have capitulated to the market, it has led to activity, Malkin said. She said one of her clients, who public records identify as private-equity executive John Weaver “Jay” Jordan II, recently lowered the price of a roughly 20,000-square-foot townhome in the Gold Coast neighbourhood to $15.75 million from the $18.75 million it listed for in 2020. While the home hasn’t yet sold, the price cut resulted in a new wave of interest, Malkin said. Jordan, who paid $1.8 million for the house in 1996 and remodelled it extensively, didn’t respond to a request for comment.

Although luxury median sale prices in the New York metro area are up by 7.69% for the three months ended June 30 compared with the year-earlier period, the slower pace of sales has allowed some opportunistic buyers to ink great deals. Vanessa Lucin of the Corcoran Group recently worked with buyers who paid $6 million for an Upper West Side apartment that was first listed for $7.495 million in June 2022. The roughly 3,383-square-foot apartment has two private balconies and is currently configured as a four bedroom, according to StreetEasy. Lucin said the couple is relocating to New York from California and began searching in January, when the market had slowed from its Covid peak. “There was another offer on the table but it wasn’t going anywhere,” she said.

Daniel Parker, co-head of Compass New Development Marketing Group, said some recent condo closings reflect deals struck during the more robust market in 2021 and 2022. In pockets of the city, such as Billionaires’ Row and Hudson Yards, developers have offered significant discounts. “They are embracing the market we have rather than the market they wish we had,” he said.

However, there are signs of life. Agents in New York reported a recent pickup in big-ticket deals this summer; in particular, large downtown condos have been the “golden sweet spot” of the market, said luxury real-estate agent Donna Olshan. A string of mega deals downtown over the past few weeks include the $52 million off-market sale of a penthouse at 150 Charles Street, the $50 million off-market sale of penthouse at 151 Wooster Street, and a signed contract for a penthouse asking $52 million at One High Line in Chelsea.

Sylvia Hughes, Lucin’s client, said she and her husband, John Hughes, saw several apartments before making an offer on their new four-bedroom on the Upper West Side. “I think the seller was motivated. This apartment had languished,” she said. By the time they saw it, the original $7.495 million asking price had been reduced to $6.195 million and their offer of $6 million was accepted. “I was beginning to wonder if we should have offered less.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

2 min

2 min

Held by the same family for 26 years, this Harbour Bridge-facing residence at Longueville is the type of property that rarely comes to market. Set on more than 1,100 sqm on one of Sydney’s most tightly held peninsulas, it combines complete privacy with uninterrupted views across the harbour to the city skyline.

It’s the sort of offering where the land is just as important as the home. Positioned directly opposite Aquatic Park with a prized northeast aspect, the residence captures sweeping harbour views from almost every main living space while remaining remarkably secluded from neighbouring properties.

Large picture windows frame the outlook throughout the home, flooding the interiors with natural light and making the harbour the centrepiece of everyday living.

Designed for family living

The home offers multiple living zones, including a formal lounge and dining rooms, a separate family room and an open-plan living and meals area. Blackbutt timber parquetry flooring, high ceilings and ducted reverse-cycle air conditioning feature throughout.

The kitchen sits at the heart of the home, with induction cooking, a generous island bench, and a walk-in pantry, connecting both the formal entertaining areas and the more casual family spaces.

A ground-floor master suite includes a walk-in robe, dressing area and ensuite, while upstairs are three additional bedrooms with built-in robes, together with a spacious home office or study.

The lower ground level adds another layer, with a temperature-controlled cellar and tasting room, plus a flexible gym, wellness or recreation space.

Resort-style setting overlooking Sydney Harbour

Outside, landscaped gardens wrap around a heated swimming pool, an expansive entertaining terrace, and a level lawn, creating a private resort-style setting against the backdrop of Sydney Harbour.

Additional features include a solar system with battery storage, remote lock-up garaging for three vehicles and generous storage throughout.

Beyond the home itself, the location remains one of Longueville’s biggest drawcards. Longueville Ferry Wharf sits around 150 metres away, providing direct access to the CBD while preserving the quiet character of one of Sydney’s most tightly held waterfront suburbs. The property is also within the catchments of Lane Cove Public School and Hunters Hill High School.

Simon Harrison and Kim Walters of Belle Property Lane Cove are marketing the property on a Contact Agent basis.

At a glance

Address: 3 Mary Street, Longueville NSW 2066

Configuration: 4 bedrooms | 3 bathrooms | 3-car garage

Land: Approximately 1,100 sqm

Highlights: Harbour Bridge and city skyline views, northeast aspect, heated pool, cellar, solar with battery storage

Held: First time offered in 26 years

Price: Contact Agent

Agents: Simon Harrison and Kim Walters, Belle Property Lane Cove

This article is produced by the Kanebridge Media editorial team. Property information has been supplied by the listing agent. Buyers should conduct their own due diligence before relying on any information contained in this article. Enquiries: propertyconcierge@kanebridge.com.au.

Chinese carmaker GAC will expand its Australian electric vehicle line-up with the city-focused AION UT hatchback.

The grand harbourside residence combines sweeping Sydney Heads views, resort-style entertaining and refined designer finishes with a reported $36 million price guide.