A hot spring selling season forecast as property market roars back to life

Real estate leader says strong sales last month point to a busy season ahead

2 min

2 min

Ray White boss Dan White is forecasting a bumper spring selling season for Australia’s property market, after the real estate company wrote a staggering $6.9 billion in sales last month.

August’s stellar result was 14 percent higher than the same month last year and only four percent down on 2021 when record home price growth was seen.

“Our August sales results officially certified the renewed and broad-based resurgence in the residential market that we have been seeing since late May,” Mr White said.

May was when Ray White saw a small “but identifiable” lift in new listings coming to market, particularly in the eastern states, he said.

“This was very unusual as new listings normally drop in the winter months. Interest rates were still rising, and given that the expectation was for an increasingly depressed market, was this a blip? But the trend became firmer in June, and stronger again in July.”

Ray White Group listed 10,500 homes in August, up 12 percent on last year and more than 20 percent higher than 2021.

And Mr White revealed the company’s pre-listing data shows a “strong” flow of more listings in the next few weeks.

“Buyers, including potential sellers that intend to repurchase, now have a lot more property to choose from. The market is very well-stocked for spring.”

Despite an increase in supply, buyer demand remains elevated across much of the country, meaning prices are likely to continue rising in the months ahead.

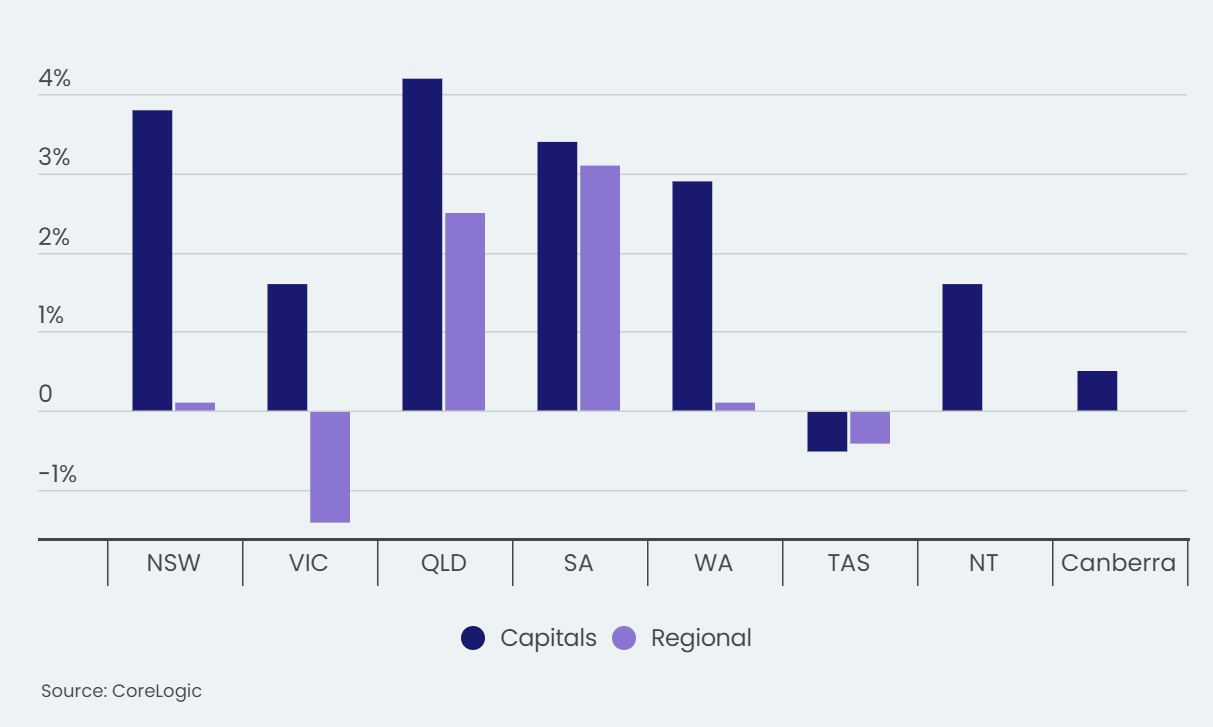

CoreLogic’s latest Home Value Index, released this week, shows home prices nationally inched upwards by 0.8 percent in August – the sixth consecutive month of growth.

Since bottoming out in February, prices at a national level are 4.9 per cent higher, adding $34,000 to the median value of a dwelling.

Sydney has led the recovery trend, with a gain of 8.8% since values found a floor in the Harbour City in January, while Brisbane has also seen values up 6.2% since bottoming out in February.

Ray White’s Lower North Shore Group posted $216 million in sales in August while Ray White Quakers Hill sold 135 homes.

Mr White is expecting the coming months – traditionally the busiest in real estate – to be just as busy.

“There will be enough stock to record some big results – maybe not at 2021 levels but not too far off,” he said. “So much depends of course on the broader economic sentiment and how that influences buyer behaviour.”

One likely driver of sustained buyer confidence is the decision this week by the Reserve Bank to leave interest rates on hold, which has led many economists to believe the tightening cycle is on hold for now.

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

While many investors are waiting for commercial property prices to fall alongside the residential market, buyers’ advocate Abdullah Nouh says they’re looking at the wrong data, with demand strengthening across several commercial sectors.

2 min

For months, Australia’s property conversation has centred on falling house prices, higher interest rates and the impact of the Federal Budget on investors.

But according to Melbourne buyers’ advocate Abdullah Nouh, many investors expecting commercial property to follow the same path are overlooking what’s actually happening across the market.

“The biggest mistake investors are making is treating commercial property as one market that moves in one direction at one time,” Nouh says.

“Office towers, neighbourhood medical centres, industrial warehouses and childcare centres all respond to completely different supply and demand dynamics.”

Rather than experiencing a broad downturn, he says that parts of the commercial market continue to perform strongly, particularly sectors supported by essential services and with limited new supply.

Neighbourhood retail centres anchored by supermarkets and medical services have proven more resilient than many expected, while industrial property continues to benefit from tight supply in most major cities.

Medical centres, childcare assets and other essential service properties are also attracting sustained tenant demand despite higher borrowing costs.

Office markets, however, are telling a different story.

Premium buildings in well-connected locations are beginning to stabilise, Nouh says, while secondary office stock in oversupplied precincts continues to face pressure.

“This isn’t a story about commercial property going up or going down,” he says.

“It’s a story about asset selection mattering more than the headlines.”

The changing market is also altering the questions investors are asking.

Rather than focusing solely on buying another residential investment property, Nouh says more investors are now looking for higher rental income and improved cash flow.

“Instead of asking how to buy another investment property, investors are increasingly asking how they can generate more income from their portfolio,” he says.

He believes commercial property has become part of that conversation because it can deliver stronger rental returns while still offering long-term capital growth when quality assets are selected carefully.

However, Nouh warns investors against assuming every commercial property represents a sound investment simply because it offers a higher yield.

“I’ve seen commercial properties remain vacant for years because they’re in locations with weak business activity,” he says.

“A high yield isn’t necessarily evidence of a good investment. Sometimes it’s evidence of the opposite.”

Instead, he says investors should focus on the same fundamentals that have always underpinned successful commercial acquisitions, including tenant demand, constrained future supply, location quality and whether another tenant would readily occupy the property if the existing lease expired.

“The lease and the tenant both matter,” Nouh says.

“But neither replaces buying a quality asset in a quality location.”

As investors continue to assess the outlook for property following this year’s Budget changes, Nouh believes the biggest opportunity may lie in recognising that commercial property is not a single market.

“Property has never moved as one market,” he says.

“The better question isn’t whether commercial property will fall in the short term. It’s which assets are likely to be in greater demand over the next decade, and whether today’s market creates an opportunity that looks obvious in hindsight.”

On October 2, acclaimed chef Dan Arnold will host an exclusive evening, unveiling a Michelin-inspired menu in a rare masterclass of food, storytelling and flavour.

The PG rating has become the king of the box office. The entertainment business now relies on kids dragging their parents to theatres.