Home loan lending increases, as housing market steadily picks up pace

2 min

2 min

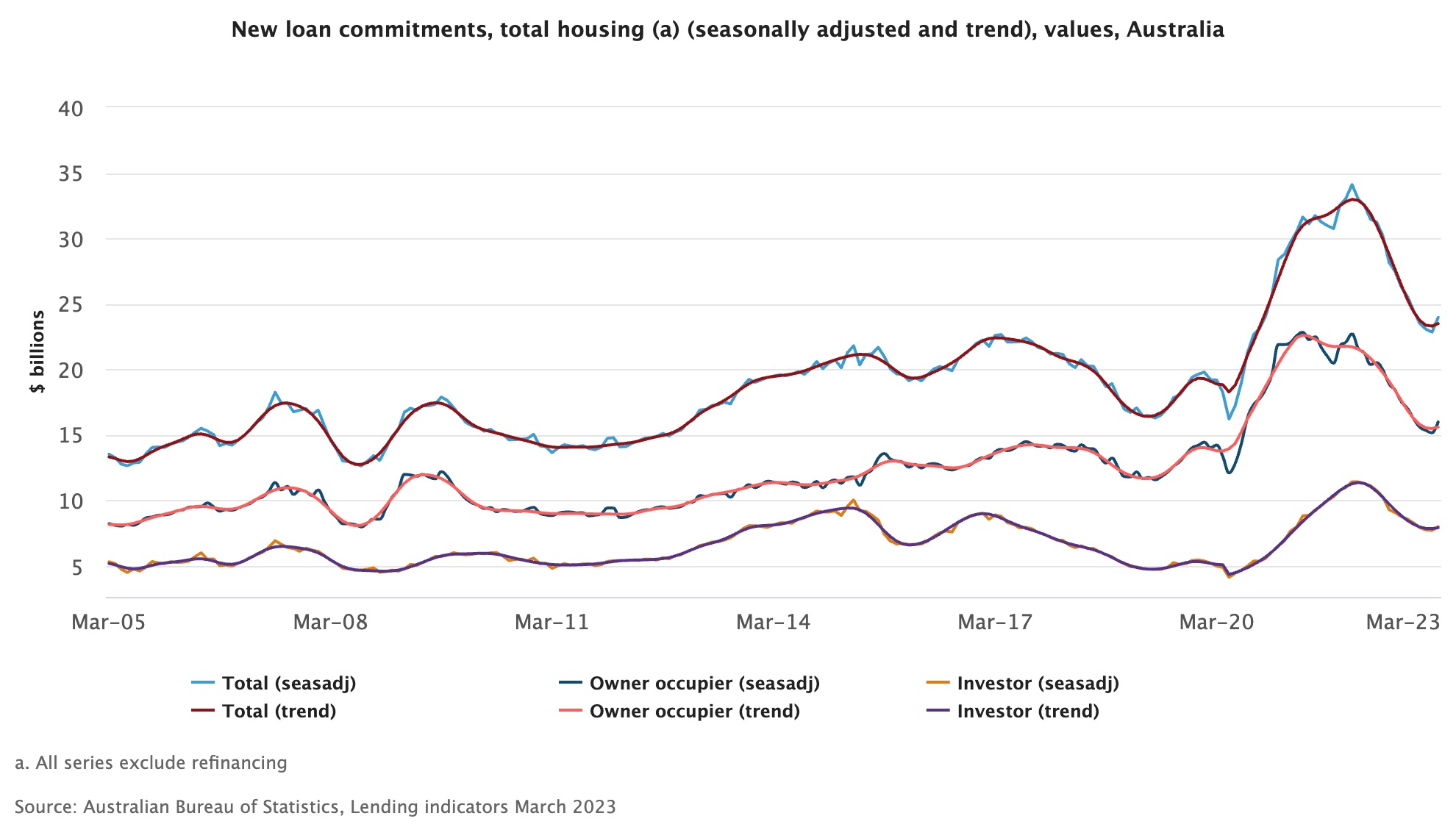

New mortgage commitments have seen a monthly rise of almost 5 percent since January 2022, ABS data released today reveals.

The strongest figures were for loan commitments by owner/occupiers, up 5.5 percent compared with investors at 3.7 percent. The rise is a 1 percent increase on February figures.

While it’s an overall improvement, the ABS notes that the $24 billion increase in loans is 26.3 percent down on this time last year. Borrowing rose sharply during COVID, particularly among owner/occupiers. This reflects the corresponding rise in housing values, which analysts put down to low interest rates and government support to protect jobs during the pandemic.

PropTrack economist Angus Moore lending activity was remarkably strong in 2020 and 2021.

“The value of new mortgage commitments in March was up just under 5% compared to April. That’s notable as it’s the first time we’ve seen an increase in new lending since early 2022,” he said. “Even so, we’re seeing a lot less new lending than we were a year ago, down a bit over a quarter compared to March 2022.

“While that’s a substantial pullback, it really reflects just how strong lending activity was in late 2021 and early 2022. The value of new loan commitments is still pretty robust and is substantially stronger than we were seeing in 2019 or early 2020, in part because of the strong growth in house prices we’ve seen.”

His expectation is that the upward trend in lending is set to continue this year, although it may be tempered by further interest rate increases by the RBA.

“External refinancing activity remains very strong and is showing no signs of slowing down,” Mr Moore said. “It hit another new peak in March, with around 28,000 owner occupiers refinancing in March alone – that’s twice as many as we’ve typically seen on average over the past two decades.”

Automobili Lamborghini and Babolat have expanded their collaboration with five new colourways for the ultra-exclusive BL.001 racket, limited to just 50 pieces worldwide.

As housing drives wealth and policy debate, the real risk is an economy hooked on growth without productivity to sustain it.

Strong consumer spending and tight supply have driven retail to the top of commercial property, but signs of pressure are starting to emerge.

2 min

Australia’s retail property sector entered 2026 as the strongest performing commercial asset class, but rising geopolitical risks and cost pressures are beginning to test its resilience, according to new research from Knight Frank.

The latest Australian Retail Review shows the sector rode a wave of consumer spending and constrained supply through 2025, delivering total returns of 9.2 per cent and driving transaction volumes up 43 per cent year-on-year to $14.4 billion.

That momentum carried into early 2026, with around $3.6 billion in deals recorded in the first quarter alone.

“Retail clearly emerged as the standout commercial property performer in 2025,” said Knight Frank Senior Economist, Research & Consulting Alistair Read.

“Improving household spending, limited new supply and stronger leasing fundamentals combined to drive better income growth and renewed investor confidence in the sector.”

Spending rebound drives retail strength

A lift in household spending has been central to the sector’s performance. Consumer spending rose 4.6 per cent year-on-year to February 2026, supported by easing inflation and improving real incomes.

That shift flowed directly into retailer performance, with average EBIT margins across major retailers rising to 8.9 per cent in the first half of 2026, their strongest level in several years.

“Stronger consumer spending was critical in restoring momentum to the retail sector,” Mr Read said.

“Retailers have generally been better able to absorb costs, rebuild margins and support sustainable rental outcomes, particularly in higher-quality centres.”

Improved trading conditions also pushed leasing spreads up 4.2 per cent in 2025, reinforcing income growth and supporting capital values.

Geopolitical tensions begin to bite

But the outlook has become more complicated. The report warns that escalating conflict in the Middle East and its impact on fuel prices, supply chains and interest rates could weigh heavily on consumer spending.

“Higher fuel prices, flow-on cost pressures across supply chains, and recent interest rate increases are collectively squeezing household budgets, and early consumer sentiment data suggests confidence is already softening,” Mr Read said.

“While household balance sheets remain generally resilient, heightened uncertainty over future costs is likely to weigh on spending — particularly in discretionary categories — in the months ahead.”

The impact is already being felt in investment activity. While the year began strongly, transaction volumes slowed in March as investors paused amid the uncertainty.

“Early indicators suggest elevated uncertainty has already begun to affect the market. While retail investment enjoyed its strongest start to a year in a decade, with nearly $3 billion transacted by the end of February, activity stalled in March, as investors took a pause amid elevated uncertainty,” Mr Read said.

Solid foundations support medium-term outlook

Despite the near-term headwinds, Knight Frank maintains that the sector’s underlying fundamentals remain strong. Limited new supply, high construction costs and population growth are expected to continue supporting rental growth over the medium term.

“Retail has entered this period of uncertainty from a position of strength,” Mr Read said.

“Supply-side constraints, population growth and improving income fundamentals remain powerful structural supports for the sector.”

The report highlights several trends shaping the year ahead, including steady yields as interest rates rise, mounting pressure on tenant margins, continued outperformance of prime centres, the growing need for logistics integration, and risks linked to underinvestment in capital expenditure.

For now, retail remains a sector with momentum, but one increasingly at the mercy of forces far beyond the shopping centre.

MAISON de SABRÉ’s new Spring Harvest Collection turns everyday produce into collectible leather charms and introduces fresh silhouettes in its cult Bucket bag family.

From warmer neutrals to tactile finishes, Australian homes are moving away from stark minimalism and towards spaces that feel more human.