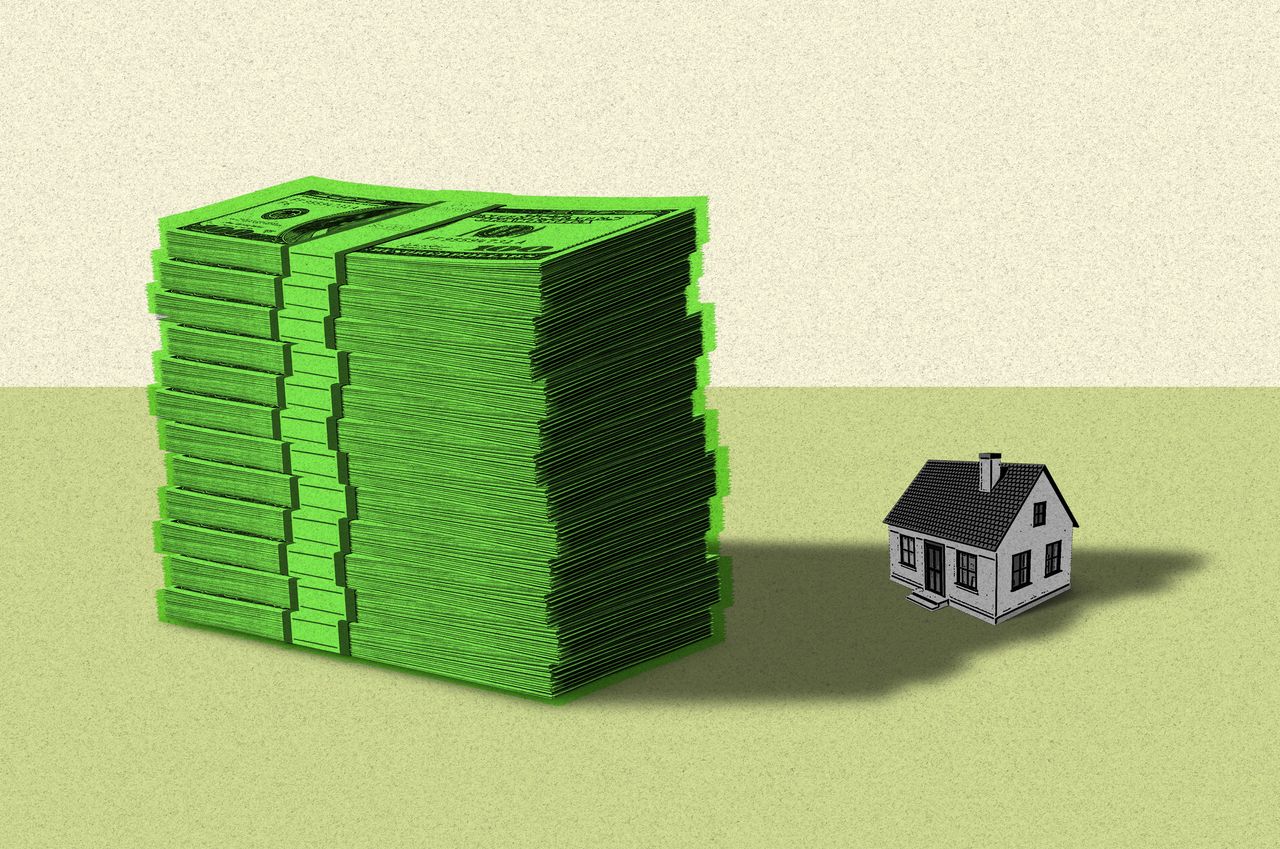

The New Math on Inheriting Your Parents’ House

Rising costs are prompting more adult children to sell the homes they inherit from their parents

3 min

3 min

One of the first things many people do when they inherit their parents’ home these days is put up a for-sale sign.

Deciding what to do with a family property is often both an emotional and financial decision, but the rising costs of renovations, property taxes and utilities are making it harder for adult children to hold on to the real estate, financial advisers say. Higher home prices and mortgage rates have often also made it impractical for heirs to buy out their siblings, said Dick Stoner, a Realtor in Rockville, Md.

The high home prices of the past few years have made the decision to sell even more attractive. If inheritors can unload a house in a hot location for a high price, the proceeds from the home’s sale can help secure their finances and fund goals such as retirement, advisers say.

“For inheritors, cash is king,” said Paige Wilbur, Wells Fargo’s head of estate services.

Cash over sentimental value

Leaving a home to children remains a common way to transfer wealth, according to financial advisers and estate planners. There is no recent data that tracks home inheritance nationally.

More than three-quarters of parents plan to leave a home to their children when they die, according to a 2023 Charles Schwab survey of more than 700 American investors between the ages of 27 and 95. Some children may be reluctant to sell for sentimental reasons, but finances and simplicity of unloading a property often win out. Nearly 70% of those who expect to inherit a home from their parents plan to sell it, the survey found.

When Heidi Whaley and her sister, Melissa Mills, inherited their parents’ home, they chose to put it on the market. They recently listed the Charleston home for just below $3.5 million. The sisters, both retired, felt some sadness letting go of the home they grew up in and where their parents hosted many waterfront parties.

“My father wanted to build a house that would be strong, one which would be passed from generation to generation,” said Whaley.

Both sisters are empty-nesters with their own nearby homes, and said they couldn’t justify the expense of maintaining a nearly 4,000-square-foot house for the sake of fond memories.

Rising costs are a bigger part of the calculus these days when heirs decide whether or not to keep an inherited house, real-estate agents say. For instance, the higher cost to insure coastal homes in the Southeast is pushing more heirs in the area to sell, said Ruthie Ravenel, a Realtor in Charleston.

Inflation has also made repairs and upkeep on older properties more expensive, leading some to favour newer properties that may be cheaper to maintain and insure, she said.

I’ll keep the vacation home, though

The declining interest in keeping Mom and Dad’s home is part of a broader generational trend among inheritors, estate planners say.

Some tangible assets aren’t considered as valuable as they were in the past, thanks partly to changing tastes, said Wilbur with Wells Fargo’s estate services.

Renovation is expensive and what one generation sees as on-trend, the other may not. For example, the younger generation of beneficiaries mostly don’t want older traditional furniture. Instead, they prefer the modern, farm-style chic look, said Wilbur.

“While Mom and Dad’s home might be nice, the children may not want to live in it and would consider it too costly to renovate to their style,” she said.

Vacation homes and secondary properties, however, are more likely to be kept by heirs, at least for a few years, especially if it is in an appealing location, financial planners say. If multiple family members are inheriting a vacation house, there needs to be a way to split maintenance costs fairly and create a usage schedule that is to everyone’s liking, said Jeff Fishman, a financial adviser in Los Angeles.

Consider the taxes

Taxes remain a key reason many heirs sell relatively soon, financial advisers say.

Aaron Buchbinder, a real-estate agent in Boca Raton, Fla., is working with three brothers who inherited their grandmother’s condominium this year in Boca Raton and none of them live in Florida. They discussed keeping it and renting it out, but none of them wanted to keep it long term and preferred to sell because of the carrying cost of the homeowners association fees and taxes, said Buchbinder.

Heirs who wish to buy out their other siblings will want to use a reasonable method for valuing the home, said John Voltaggio, a managing director at Morgan Stanley Private Wealth Management. The family may decide to use the value reported on the estate tax return if it is recent, or they may want to obtain a few appraisals and use an average, he said.

The family members inheriting the property will also want to make sure they aren’t getting in over their head financially, with mortgage rates hovering around 7%.

“Many financial decisions today are very rate-dependent, so remove emotions or risk doing something you may later regret,” said Fishman, the financial adviser in Los Angeles.

A home’s cost basis—which is the starting point for measuring a future taxable gain—resets to market value, typically its value at the date of death, said Eric Smith, a spokesman for the Internal Revenue Service.

Any increase in value after death is taxed as long-term capital gains, and those rates are lower than the rates on short-term gain. But if a home is sold quickly, there is likely to be little gain if any and little to no tax, said Smith.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Margot Robbie may have travelled from a Queensland farm to the highest reaches of Hollywood, but a reported $28 million property deal suggests the Gold Coast has never lost its hold on her. The Australian actor and producer is believed to be the mystery buyer of Redwood, a seven-acre Currumbin Valley estate transformed into the …

Continue reading “Margot Robbie Reportedly Behind $28 Million Currumbin Valley Homecoming”

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

3 min

The most coveted properties are rarely defined by amenity alone. Their value lies in something far more enduring: a position that cannot be recreated.

Occupying one of the final north-facing, absolute riverfront sites in South Brisbane, The Riversdale commands an extraordinary position where the Brisbane River arcs towards the city, capturing sweeping views across water, skyline and parkland.

Positioned between the cultural sophistication of South Bank and the creative energy of West End, it sits at the centre of one of Brisbane’s most connected, walkable and desirable lifestyle precincts.

For Mosaic, one of Australia’s most awarded and trusted developer-builders, The Riversdale represents far more than another residential project. It is the culmination of a vision first pursued in 2018, when the company identified the site as one of Brisbane’s last truly irreplaceable riverfront opportunities.

Defined by a relentless commitment to design excellence, craftsmanship and enduring value, Mosaic has built a reputation for creating residences distinguished not only by their architectural quality, but by the way they are lived in and enjoyed for decades to come. The Riversdale is perhaps the purest expression of that philosophy to date.

Designed in collaboration with acclaimed architects Bureau Proberts, the landmark development draws inspiration from the movement of the river itself. Sculptural in form, its flowing curves, layered articulation and expansive glazing respond to light, outlook and connection to place, creating a distinctive architectural presence on Brisbane’s evolving waterfront.

The development comprises 213 residences and Masterpiece Sky Homes, each designed with an emphasis on generosity, permanence and livability. Natural stone, richly crafted timber finishes and meticulously detailed joinery create interiors of understated luxury, while expansive glazing and outdoor living spaces immerse residents in ever-changing river and city vistas.

Rather than following passing trends, every residence has been conceived as a timeless individual home designed to endure.

Beyond the residences, a carefully considered collection of extremely generous six-star hotel-inspired amenity elevates daily life. A concierge-serviced arrival experience, dedicated guest suites, private business facilities, wellness spaces and an exclusive resident EV fleet provide a level of convenience more commonly associated with the world’s leading luxury hotels.

Nearly 3,000 square metres of curated amenity culminates in a spectacular rooftop destination overlooking the river and city skyline. Resort-inspired leisure spaces, private dining experiences, sophisticated entertaining areas and landscaped retreats create opportunities for both celebration and relaxation.

Crowning the experience is an exclusive private club, conceived as a sophisticated social destination for residents and their guests. Beautifully appointed private dining rooms, elegant lounges, an intimate cocktail bar and a variety of entertaining spaces create the perfect setting for everything from casual gatherings to milestone celebrations.

Complemented by billiards, championship golf and Formula 1 simulators, it offers a rare blend of hospitality, recreation and connection, all framed by sweeping views across the Brisbane River and city skyline.

Yet its greatest luxury is its rarity.

The broader transformation of South Brisbane will introduce new public spaces, parklands and lifestyle amenity, further enhancing what is already Queensland’s premier cultural and lifestyle precinct. While the surrounding neighbourhood continues to evolve, The Riversdale will retain a true riverfront position that cannot be replicated.

At a time when opportunities for absolute riverfront ownership are becoming increasingly scarce, The Riversdale represents one of Brisbane’s last great waterfront acquisitions; a landmark address shaped by vision, underpinned by certainty and destined to become part of the city’s enduring legacy.

The Riversdale by Mosaic is currently under construction, with completion anticipated in late 2029.

Register to learn more at The Riversdale by Mosaic.

A long-standing cultural cruise and a new expedition-style offering will soon operate side by side in French Polynesia.

A cluster of century-old warehouses beneath the Harbour Bridge has been transformed into a modern workplace hub, now home to more than 100 businesses.