Why Inflation Erupted: Two Top Economists Have the Answer

Former Fed chair, IMF chief economist say it wasn’t pandemic or stimulus; it was the pandemic, then the stimulus

4 min

4 min

For two years debate has raged over what caused the highest inflation since the 1980s: government stimulus or pandemic-related disruptions.

Now two of the country’s top economists have an answer: It’s both. Pandemic-related supply shocks explain why inflation shot up in 2021. An economy overheated by fiscal stimulus and low interest rates explain why it has stayed high ever since. The conclusion: For inflation to fade, the economy has to cool off, which means a weaker labour market.

The study, released Tuesday, is by Ben Bernanke, former chair of the Federal Reserve, and Olivier Blanchard, former chief economist of the International Monetary Fund. Bernanke is now at the Brookings Institution and Blanchard is at the Peterson Institute for International Economics. The two are among the world’s most cited academic economists.

When Congress passed President Biden’s $1.9 trillion American Rescue Plan in early 2021, which included checks to households, enhanced jobless benefits and aid to state and local governments, inflation was around 2% and unemployment, though coming down, still above 6%.

At the time many forecasters thought the stimulus could push demand above the economy’s potential to supply goods and services and unemployment below its long-run natural rate of around 4%. Yet few thought this would meaningfully raise inflation. In previous decades unemployment had remained similarly low without raising price pressures.

A few disagreed, notably former Treasury Secretary Lawrence Summers and Blanchard. Both warned the stimulus was so large it would push the economy dangerously into overheating territory.

Not the inflation critics expected

Inflation did shoot up, hitting 7% that December, 5.5% excluding food and energy. “The critics’ forecasts of higher inflation would prove to be correct—indeed, even too optimistic—but, in substantial part, the sources of the inflation would prove to be different from those they warned about,” Blanchard, one of those critics, and Bernanke write in their study.

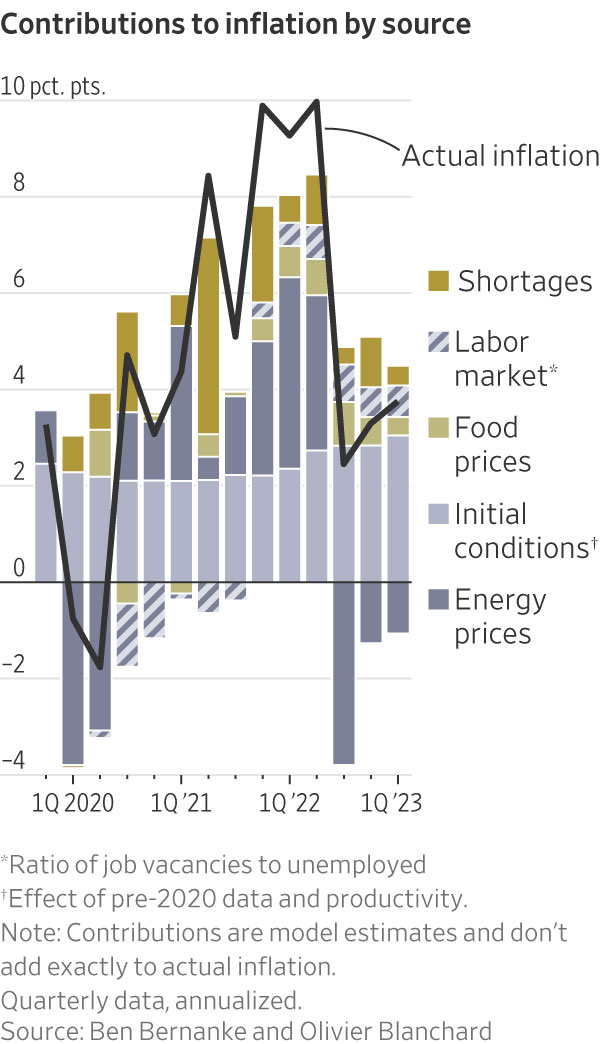

To tease out the sources of inflation, Bernanke and Blanchard build a relatively conventional model in which inflation is a function of, among other things, the gap between the supply and demand for labor, the public’s expectations of inflation, and commodity prices. They include a variable for supply-chain disruptions derived from Google searches for “shortage.”

Usually economists judge labor market tightness from how far unemployment is above or below its natural rate. But this time the labor market heated up before unemployment got that low. So instead, Bernanke and Blanchard use the ratio of job vacancies to unemployed workers. Finally, their model lets all these factors interact, with varying lags.

If stimulus had overheated the economy, it should have shown up in the labor market, i.e., an unusually high ratio of vacancies to unemployed. In fact, labor market conditions put downward pressure on inflation through the third quarter of 2021, the authors concluded. Instead, the inflation that year was driven almost entirely by shortages and energy prices. (To be sure, many shortages reflected restricted supply interacting with demand boosted by stimulus.)

Demand shifted abruptly from services to goods in the early months of the pandemic. The overall effect should have been a wash as prices rose for goods and fell for services. It wasn’t, because goods producers faced supply constraints, which caused costs and prices to spike, while costs to service producers didn’t decline much. “These sectoral mismatches between demand and supply proved more intractable and longer-lasting than many had expected,” the authors note.

The legacy of stimulus

These pandemic disruptions did eventually subside. Why didn’t inflation then fall? The reason, the authors conclude, is that by this point demand was so strong, reflecting the legacy of low interest rates and fiscal largess, the labor market was significantly overheated with the ratio of vacancies to unemployed up dramatically. Moreover, the initial surge of inflation had an echo: It lifted workers’ expectations of short-term inflation, which then partly found its way into their wages.

If anything, the study might understate the effect of pandemic disruptions. The labor market didn’t just overheat because of excess demand, but reduced supply, as well. The rising ratio of vacancies to unemployed, which the model equates with a tighter labor market, reflects employers struggling to fill vacancies. The authors note much of that struggle was because of the pandemic: Firms that had laid off employees had to find new ones, while some workers left the labor force because of family obligations, illness or work-life balance priorities.

This decline in supply-side potential hasn’t gotten much attention in the inflation debate, but its role could be significant. John Williams, president of the Federal Reserve Bank of New York, last week estimated that potential was 4.2% lower at the end of 2022 than its pre pandemic trend.

That stimulus wasn’t the inflation culprit it is often made out to be doesn’t entirely absolve the Fed and Biden. Arguably, they should have anticipated supply disruptions would amplify the risks of stoking demand. In 2020 the Fed introduced a new framework and guidance under which interest rates would stay near zero until maximum employment was restored, even if inflation topped its 2% target. That “contributed to delayed action and the inflation overshoot,” former Fed Vice Chair Donald Kohn and Brown University economist Gauti B. Eggertsson say in another paper to be presented Tuesday.

Bernanke and Blanchard conclude that because inflation today reflects a too-hot labor market, the solution is to cool it off. To bring inflation back to the Fed’s target, they estimate unemployment would have to rise above 4.3% from its current 3.4% assuming vacancies remain difficult to fill. But, they say, inflation could drop without a significant increase in unemployment if the ease of hiring returns to pre pandemic norms. The good news: There are tentative signs that is happening.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Ophora Tallawong has launched its final release of quality apartments priced under $700,000.

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

2 min

2 min

Held by the same family for 26 years, this Harbour Bridge-facing residence at Longueville is the type of property that rarely comes to market. Set on more than 1,100 sqm on one of Sydney’s most tightly held peninsulas, it combines complete privacy with uninterrupted views across the harbour to the city skyline.

It’s the sort of offering where the land is just as important as the home. Positioned directly opposite Aquatic Park with a prized northeast aspect, the residence captures sweeping harbour views from almost every main living space while remaining remarkably secluded from neighbouring properties.

Large picture windows frame the outlook throughout the home, flooding the interiors with natural light and making the harbour the centrepiece of everyday living.

Designed for family living

The home offers multiple living zones, including a formal lounge and dining rooms, a separate family room and an open-plan living and meals area. Blackbutt timber parquetry flooring, high ceilings and ducted reverse-cycle air conditioning feature throughout.

The kitchen sits at the heart of the home, with induction cooking, a generous island bench, and a walk-in pantry, connecting both the formal entertaining areas and the more casual family spaces.

A ground-floor master suite includes a walk-in robe, dressing area and ensuite, while upstairs are three additional bedrooms with built-in robes, together with a spacious home office or study.

The lower ground level adds another layer, with a temperature-controlled cellar and tasting room, plus a flexible gym, wellness or recreation space.

Resort-style setting overlooking Sydney Harbour

Outside, landscaped gardens wrap around a heated swimming pool, an expansive entertaining terrace, and a level lawn, creating a private resort-style setting against the backdrop of Sydney Harbour.

Additional features include a solar system with battery storage, remote lock-up garaging for three vehicles and generous storage throughout.

Beyond the home itself, the location remains one of Longueville’s biggest drawcards. Longueville Ferry Wharf sits around 150 metres away, providing direct access to the CBD while preserving the quiet character of one of Sydney’s most tightly held waterfront suburbs. The property is also within the catchments of Lane Cove Public School and Hunters Hill High School.

Simon Harrison and Kim Walters of Belle Property Lane Cove are marketing the property on a Contact Agent basis.

At a glance

Address: 3 Mary Street, Longueville NSW 2066

Configuration: 4 bedrooms | 3 bathrooms | 3-car garage

Land: Approximately 1,100 sqm

Highlights: Harbour Bridge and city skyline views, northeast aspect, heated pool, cellar, solar with battery storage

Held: First time offered in 26 years

Price: Contact Agent

Agents: Simon Harrison and Kim Walters, Belle Property Lane Cove

This article is produced by the Kanebridge Media editorial team. Property information has been supplied by the listing agent. Buyers should conduct their own due diligence before relying on any information contained in this article. Enquiries: propertyconcierge@kanebridge.com.au.

A restored 1860s Brisbane residence transformed by GRAYA has smashed Paddington’s house price record, selling for more than $12 million.

Rising rates, construction inflation and shrinking investor confidence are pushing Australia deeper into a dangerous housing spiral that monetary policy alone cannot fix.