Nine-Figure Home Sales Are Skyrocketing. ‘Soon $100 Million Will Be $200 Million.’

The ultraluxury market has seen a surge in megadeals in recent years, as the ranks of wealthy buyers grew across the world

6 min

6 min

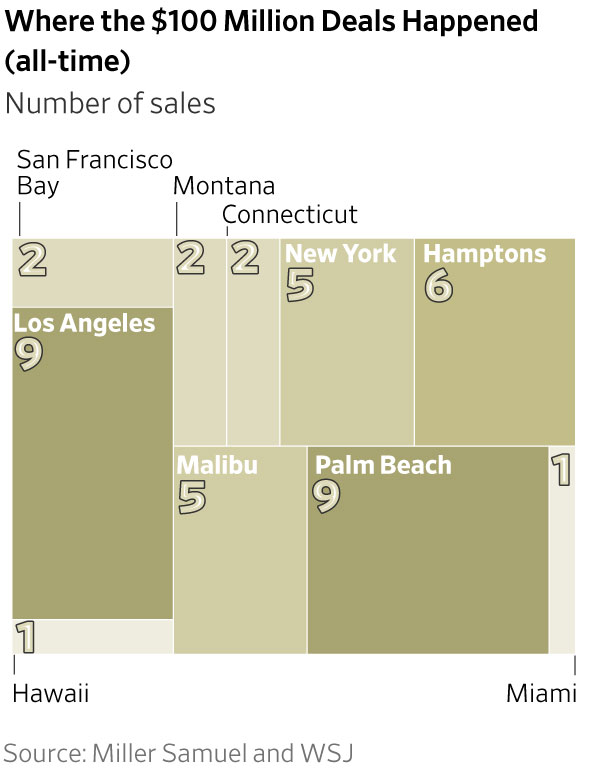

It has been nearly 20 years since the country’s first $100 million home sale, but in some ways the market is just taking off: Since 2020, at least 24 homes nationwide have traded for $100 million and up, more than the total number of nine-figure sales during the entire prior decade combined.

The 24 homes, and their uber-wealthy owners, also tell the compelling story of massive wealth creation and migration in the U.S. since the onset of the pandemic, with a dramatic surge in nine-figure deals in Florida in recent years. Since 2020, three homes over $100 million have changed hands in New York City compared with six in and around Palm Beach, including a $170 million deal in 2023 that set a Florida sales record.

“People’s wealth has grown so substantially and there’s such limited product,” said Chris Leavitt of Douglas Elliman in Palm Beach. “There are more billionaires than there are oceanfront, sprawling estates.”

Los Angeles and Malibu, Calif., have also notched a string of major transactions, gaining steam as the wealthy sought space and privacy during the pandemic or picked up second homes. Last year, entertainment power couple Beyoncé and Jay-Z paid $190 million for a mansion in Malibu that set a California sales record—and sparked predictions that the $200 million threshold is within reach.

“Soon $100 million will be $200 million, that’s the way it’s going,” said Drew Fenton of Carolwood Estates in Beverly Hills. “We’re inching closer to it.”

Nationwide, the number of mega deals skyrocketed as the ranks of ultra wealthy individuals swelled around the globe. There were 3,194 billionaires in 2023, up from 2,170 in 2013, according to wealth research firm Wealth-X.

Meanwhile, luxury home prices nationwide have soared. In 2023, the median sale price for a luxury home nationwide—defined as homes in the top 5% of the market—was $1.14 million, up 75% compared with 2013, according to real-estate brokerage Redfin.

In the past few years, the values of trophy homes around the country—disconnected as they might be from the rest of the market—also skyrocketed. So did the number of deals. In the 10 years between 2011 and 2020, there were 19 deals at or above $100 million. There were 22 deals over $100 million between 2021 and 2023. Those deals included properties that roughly doubled in value in a short amount of time.

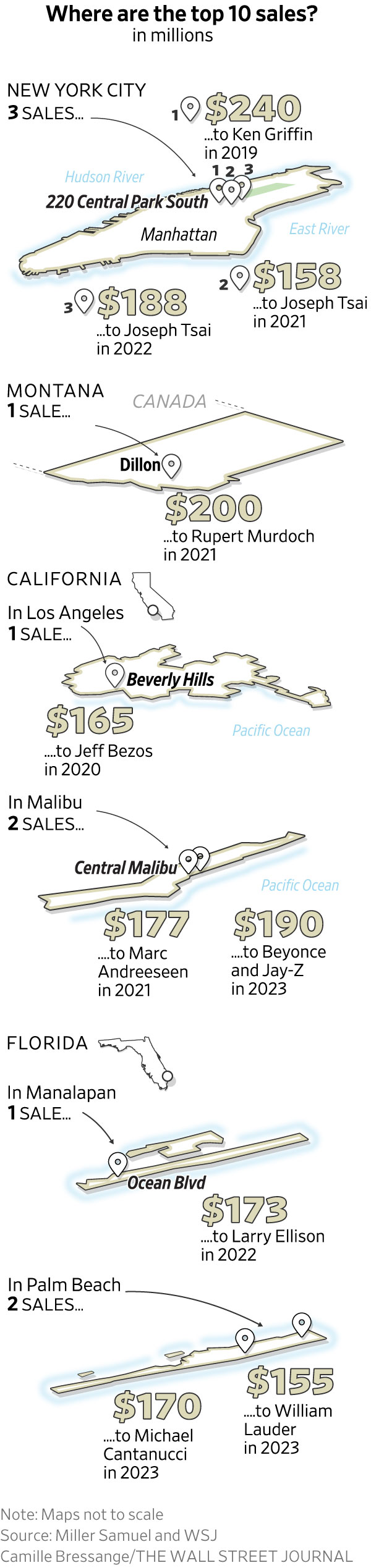

For example, Alibaba Group co-founder and Brooklyn Nets owner Joseph Tsai paid $188 million in 2022 for a penthouse at 220 Central Park South, the Robert A.M. Stern Architects-designed condo tower on Manhattan’s Billionaires’ Row. The seller was billionaire investor Daniel Och, who purchased the property for $95 million in 2019. Also in 2022, Oracle co-founder Larry Ellison bought an oceanfront estate near Palm Beach for $173 million. Seller Jim Clark, a co-founder of Netscape, paid just over $94 million for the property in 2021.

Although Ken Griffin’s roughly $240 million penthouse buy in Manhattan in 2019 is still the country’s most expensive sale, nine-figure deals have surged in Malibu and South Florida.

Florida, which had an influx of wealthy residents during Covid, had one deal above $100 million in 2013 and two in 2019. Since 2020, there have been seven—including six in and around Palm Beach, where the city’s sales record was shattered twice in 2023. In March, billionaire William Lauder bought the late Rush Limbaugh’s longtime Palm Beach estate for $155 million. The next month, luxury car dealership owner Michael Cantanucci paid $170 million for an oceanfront estate from Green Mountain Coffee Roasters founder Robert Stiller.

Miami, which courted the tech industry and others during the pandemic, also saw record sales in quick succession. In January 2022, Griffin paid a record $75 million for a mansion on Star Island, besting the prior Miami sales record of $60 million for two penthouses at Miami’s Faena House condominium. (The Citadel founder was also the buyer of those units, which he has since sold.) Then in June 2022, Phillip Ragon, founder of software company InterSystems, purchased three homes in Golden Beach—about 20 miles from downtown Miami—for a combined $93 million. In September 2022, Griffin struck again and handed Miami its first nine-figure deal with his $106.875 million purchase of a 4-acre estate from philanthropist Adrienne Arsht.

“That was a new frontier for Miami, but it was such a stupendous property,” said Jill Hertzberg of the Jills Zeder Group at Coldwell Banker Realty, who represented Griffin in the deal with colleague Jill Eber. Hertzberg said unlike Miami’s last real-estate boom in the early 2000s, which was fuelled by foreign buyers, domestic buyers are driving up prices for luxury properties.

With buyers from America’s 1% focused elsewhere, New York City logged fewer $100 million-plus deals by comparison. In 2023, Manhattan had no nine-figure deals. In 2022, it had two, including Tsai’s $188 million purchase and philanthropist Julia Koch’s purchase of two Upper East Side penthouses from the estate of the late Paul Allen for a combined $101 million. In 2024, real-estate developer Extell inked a deal to sell a penthouse at Central Park Tower for around $115 million. The deal hasn’t yet closed.

Local real-estate agents said the city’s biggest sales have taken place within a roughly 1-mile radius, where there are a limited number of properties that can fetch $100 million or more. “Everybody wants the Central Park view,” said Pam Liebman of the Corcoran Group. “There’s only a handful of buildings that could ever warrant that price,” she said. “It’s just a scarcity thing.”

But Jonathan Miller of real-estate appraisal firm Miller Samuel said developers sold off many of their biggest units over the past few years, and new inventory is skewing smaller. “The odds of having a lot more 10,000-square-foot transactions—those are the ones that are going to break the $100 million threshold—seem limited,” he said.

Covid also altered the city’s luxury market permanently. “Everybody needs to be here, it’s still the finance capital of the world, but they’re spending less time here,” said Tal Alexander of real-estate brokerage Official. He said buyers who want a sprawling apartment overlooking Central Park can get one for $40 million to $50 million. For that reason, he thinks buyers are more likely to spend $100 million for oceanfront land with multiple structures in Palm Beach than they are on a condominium in Manhattan, he said.

The reality is that many $100 million-plus properties rarely come to market, said Corcoran’s Tim Davis, who works in the Hamptons. “We’ve got low inventory,” he said. In 2023, a roughly 8-acre Hamptons estate sold for $112.5 million, the priciest Hamptons sale of the year.

Historically, California’s largest trades have also involved a small collection of trophy estates in Los Angeles, and to a certain degree, new spec homes. The size, provenance and location of L.A.’s iconic estates makes them rare commodities, Fenton said.

Among them is Casa Encantada, a roughly 8.5-acre estate owned by late billionaire Gary Winnick and his wife, Karen Winnick. After setting a U.S. sales record when it sold in 1980 and again in 2000, Casa Encantada hit the market in 2023 asking $250 million. It is now listed for $195 million.

Kurt Rappaport of Westside Estate Agency, who is marketing Casa Encantada with Fenton, said the price is justified by how infrequently properties of this caliber come to market. “There are a lot of people who own these properties who don’t want to sell,” he said. He pointed to Bezos’s 2020 purchase of the Warner Estate in Beverly Hills for $165 million, and Lachlan Murdoch’s purchase of Chartwell, an estate in Bel-Air, for roughly $150 million in 2019. (Murdoch is executive chairman of News Corp which owns Dow Jones & Co., publisher of The Wall Street Journal.) “If you look at who owns these great houses, some of them are generational,” Rappaport said.

Given the scarcity of singular trophy homes, savvy buyers have scooped up multiple properties in prime markets in recent years. Griffin, for example, has spent more than $250 million assembling land to build a mansion in Palm Beach over the past few years. In 2023, Bezos paid a combined $147 million for adjacent properties in Miami’s Indian Creek Village. “People have realized how precious land is in cities—there’s not a lot of land so if you find a particular piece that’s gorgeous, and you have the opportunity to buy next to you, why not?” Hertzberg said.

Buyers have also paid a premium for more space and privacy. In Malibu, WhatsApp founder Jan Koum spent a combined $187 million for neighbouring properties that he bought in two transactions in 2019 and 2021. Likewise, venture-capitalist Marc Andreessen and his wife, Laura Arrillaga-Andreessen, paid $177 million for a Malibu compound in 2021; a year later, they paid $44.5 million for another trophy home nearby.

Real-estate agents said there are also some properties that have been built over time that would likely fetch $100 million if they were ever sold. In Manhattan’s Greenwich Village, for instance, Chipotle Mexican Grill founder Steve Ells paid close to $32 million in two transactions in 2014 and 2015 to buy neighbouring townhouses. He later filed for permission from the New York City Landmarks Preservation Commission to combine the two buildings—spanning almost 16,000 square feet combined—into a mansion. In recent months, Ells has quietly been shopping the property, according to people familiar with the offer. The asking price? $125 million.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

Australia’s housing affordability crisis is being fuelled by chronic undersupply, planning delays and rising development costs, as politicians continue to focus on the wrong solutions.

3 min

Australia’s housing crisis will not be solved by first-home buyer incentives or tax changes alone, with leading property figures warning governments must tackle supply constraints if affordability is to improve.

Speaking at the Kanebridge Quarterly Property Leadership Summit in Sydney last week, expert project marketing specialist Sam Elbanna, property investor and fund manager Paul Miron and property consultant Karla McNeice said that a lack of housing supply remained the central issue facing the market.

Elbanna, Director of CPM Realty with more than 30 years’ experience in project sales, argued that successive governments had focused too heavily on stimulating demand rather than addressing the barriers preventing new housing from being delivered.

“The misconception is that politicians think the way to solve the housing crisis is to drive demand,” he said.

“The reality is that’s not the way. This is a supply-side problem, and it needs to be solved on the supply side.”

Drawing on his experience in project sales, Elbanna said policies designed to help first-home buyers often had unintended consequences, pointing to previous grants that ultimately flowed through to higher property prices.

Instead, he said developers were facing increasing red tape, approval delays and rising costs, which were discouraging new housing supply.

“In the absence of stock, demand exceeds supply,” he said.

Miron, a Co-Founder and Fund Manager of Msquared Capital, said the housing debate had become overly focused on tax policy while overlooking broader structural issues.

He argued that affordability challenges stemmed from a combination of factors, including planning constraints, supply shortages, migration levels and interest rates.

“No-one can be 100 per cent certain on the real reason for property prices is going up,” he said.

“The reason why property prices are higher is a combination of interest rates, lack of supply, migration, vacancy rates and maybe taxes play a role.”

Miron was critical of recent federal housing policy changes, warning they could reduce the number of new homes being built and further constrain supply that was even highlighted in the budget.

He also highlighted the importance of the property sector to the broader economy, noting that residential real estate and related industries employed more than one million Australians.

McNeice, who advises developers on sales strategy and market intelligence, said understanding buyers had become increasingly important as affordability pressures intensified.

While affordability remained a major consideration, she said today’s buyers were focused on value rather than simply price.

“People are looking for value for money,” she said.

She said buyers were increasingly evaluating factors such as transport connections, walkability, nearby amenities and flexible living spaces that could accommodate changing family needs.

“What infrastructure is going on? Can I walk to the shops? Can I meet people at the local cafe?” she said.

The panel also discussed the mounting pressures facing developers, with Elbanna arguing that many projects become financially unviable from the moment a site is purchased.

“The viability of a development happens at the moment the site is bought,” he said.

He said rising construction costs, higher interest rates and overly optimistic feasibility assumptions had left some developers exposed as market conditions changed.

While acknowledging the growing number of smaller and first-time developers entering the market, Elbanna said property development required expertise across finance, construction, marketing and legal disciplines.

“It is actually a business that requires a level of expertise,” he said.

Looking ahead, the panel agreed opportunities remained in the market despite current challenges.

Miron said property should continue to be viewed as a long-term investment and cautioned against trying to time short-term market movements.

McNeice said success would increasingly depend on identifying projects that genuinely met changing buyer expectations.

Elbanna said affordable housing remained achievable, but developers needed to deliver more than just homes.

“We can provide affordable housing in this country,” he said.

“But we’ve got to wrap that affordable housing with the things that people want.”

As Australia’s housing affordability debate intensifies, the panellists agreed on one point: without a meaningful increase in housing supply, demand-side measures alone are unlikely to solve the nation’s property challenges.

Margot Robbie and Jacob Elordi star in an adaptation of the classic novel that respects the romance’s slow burn.

From citrus oils to warming spices, the classic G&T is being reimagined at home as a more thoughtful, seasonal ritual for modern entertaining.