How an Ex-Teacher Turned a Tiny Pension Into a Giant-Killer

A bold bet on rising rates lifted a small Massachusetts fund near the top of the performance rankings.

5 min

5 min

Plymouth County is known for Pilgrims, cranberries—and a top-performing pension fund run by a 65-year-old former schoolteacher.

After a decade of mostly ho-hum performance, the $1.4 billion Plymouth County Retirement Association ranked in the top 10% of U.S. pensions over the past three years. Key to that success was an early—and prescient—bet that interest rates would rise. That buoyed the fund through big chunks of the past two years, when climbing rates hammered both stocks and bonds.

Now markets of all kinds have posted a six-month rally , stocks are hitting records and Plymouth risks falling behind again. But Peter Manning, the fund’s director of investments, is sticking to his guns. The hope that rates will fall soon is misplaced, he said. Another downturn could be coming for Wall Street.

And so, to Manning, the best way to enlarge the pension long term is by avoiding big losses, rather than chasing high returns.

“It ain’t about what you make. It’s about what you keep,” he said.

Beating the big guys

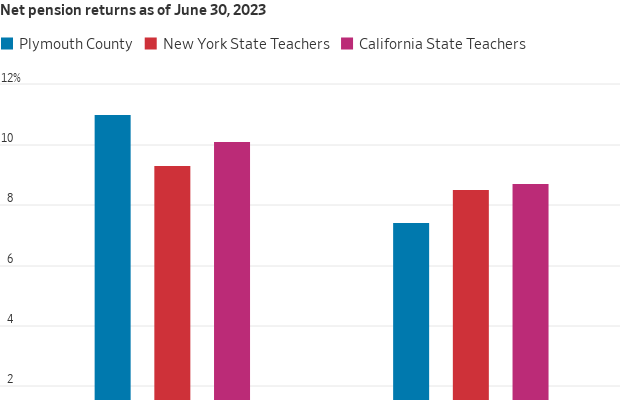

The fund, which manages savings for the county’s firefighters, bus drivers and custodians, delivered average annual net returns of 5.7% in the three years ending Dec. 31. That put it ahead of 92% of pensions nationally. The median U.S. public retirement fund returned 3.7% over the same period, according to Investment Metrics, a portfolio analysis provider.

Plymouth County surpassed bigger peers by slashing exposure to Treasurys and public stocks before they tanked in 2022. The fund then reinvested the money in infrastructure, private equity and inflation-protected debt.

While many other public plans have followed suit , the trades were also unusually quick for pension funds, which often change investments incrementally rather than in bold strokes.

“A lot of our clients made moves on the margin,” said Daniel Dynan, a managing principal at Meketa Investment Group, Plymouth County’s investment consultant. “The difference in Plymouth is the magnitude of the change.”

An unlikely trendsetter

With only 10,500 members, the fund is an unlikely trendsetter. U.S. public pensions guarantee retirement and benefit payments to 34 million members nationally, according to data from the Urban Institute, a nonprofit think tank. Plymouth County, which lies south of Boston, encompasses mostly middle-class suburbs, but also some wealthy enclaves and gritty urban areas. It is split between Democratic and Republican voters.

A decade ago, Plymouth County had only about half of the money it needed to make expected payments for its retirees. An accounting change in 2012 drastically widened shortfalls for most public pensions across the country.

At the same time, the board overseeing the fund, which had spent years relying solely on an outside consultant, was dissatisfied with its investment performance. The approach resembled the classic mix of 60% stocks and 40% bonds popular with ordinary investors.

“We were doing what everyone else was doing, running a 60-40 portfolio and hoping for the best,” said Tom O’Brien, Plymouth County’s treasurer and chairman of the pension board.

From teacher to investor

The county hired Manning to advise the board on investment strategy in 2012. He had never managed a pension fund before.

“I was a schoolteacher [in the 1980s] in a suburb of Boston and one day, after staring at 20 vacuous stares, I had a talk with my Uncle Bill, a currency trader,” Manning said.

He spent two decades trading commodity futures at his uncle’s brokerage in Boston and stocks at brokerages in Chicago. Then he became a financial adviser to wealthy individuals and families at Merrill Lynch on Cape Cod.

The job at Plymouth County involved a small pay cut, but offered the opportunity to run a nine-figure portfolio for public employees. He got a taste of how painful rising rates could be in May 2013, when comments by Fed Chairman Ben Bernanke sent bond prices tumbling in what became known as the “taper tantrum.”

“We lost $20 million in three trading days and it took us 36 months of clipping coupons to make that back,” Manning said. Coupons are the interest payments bondholders receive.

Initially, Manning and O’Brien focused on boosting alternative investments such as private equity and infrastructure, which made up less than 5% of the fund. They were part of a flock of pension funds seeking alternative investments for higher returns .

Plymouth County hired Meketa as a consultant in 2015, and private-equity and infrastructure investments climbed to nearly 15% by 2020, according to fund financial reports. Returns improved.

“They have a level of comfort being different,” said Dynan.

A contrarian call

Markets were on a tear the following year, lifted by the economy’s reopening from the pandemic. But Manning grew concerned in the summer about inflation. While many on Wall Street were calling price increases transitory, he worried inflation would persist, triggering rate increases and declines in stocks and bonds.

“We were going to conferences and being told that inflation was a paper tiger, or ‘this is not your father’s inflation,’” O’Brien said.

Manning consulted Bob Sydow, a high-yield bond fund manager at Mesirow who manages part of the pension’s money. Like Manning, he has worked on Wall Street since the 1980s.

“The money supply grew 43% over 26 months during Covid,” Sydow said. “I called it ‘free-range’ money and I thought it would generate a lot of inflation.”

From October 2021 to February 2022, Plymouth County pension sold about $80 million of its public stocks, or 6% of the fund’s assets, according to an email viewed by The Wall Street Journal. It shifted into real estate and infrastructure as well as short-term and floating-rate debt that is less sensitive to rising rates than traditional bonds, Manning said.

The fund lost 6.5% in 2022 while the median U.S. pension plan lost 14%. That outperformance has helped it stay ahead of other funds, even after it lagged behind the average in 2023.

Now, inflation remains above the Fed’s targets , and analysts’ forecasts for multiple rate cuts this year seem less certain. Plymouth County is keeping its strategy relatively unchanged, betting that rates will remain steady—or even climb.

Many investors are buying back into bonds because yields are at multiyear highs and they expect cuts by the Fed to trigger a rally. Manning takes a different tack. He thinks rates could stay high far longer than the Wall Street consensus, so he is using infrastructure funds to deliver income rather than bonds.

“Why do you have to own bonds at all in 2024?” Manning said. “It’s a legitimate question.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

Margot Robbie may have travelled from a Queensland farm to the highest reaches of Hollywood, but a reported $28 million property deal suggests the Gold Coast has never lost its hold on her. The Australian actor and producer is believed to be the mystery buyer of Redwood, a seven-acre Currumbin Valley estate transformed into the …

Continue reading “Margot Robbie Reportedly Behind $28 Million Currumbin Valley Homecoming”

Artificial intelligence is making it easier than ever to build a business without building a team. As AI takes over coding, customer support, marketing, administration, and other day-to-day tasks, a growing number of solo founders are scaling startups to millions in revenue with few—or even no—employees. While the trend is lowering barriers to entrepreneurship, it is also reshaping hiring, raising questions about the future of work and how businesses will grow in the AI era.

5 min

Ben Broca launched a company last December that offers AI tools to entrepreneurs. He’s already added 10,000 paying customers and is on track to bring in $10 million in revenue this year.

One thing he hasn’t added: any other employees.

The 40-year-old is part of a class of entrepreneurs who are launching, and then often running, new companies on their own. Artificial intelligence tools answer Broca’s emails, help write and debug code, field requests from customers, sign up new subscribers and grant refunds when issues arise.

Broca relishes his ability to make whatever decisions he wants on his own, often from his sun-drenched Sausalito, Calif., living room. “I think compromises make lukewarm results,” he said.

Once upon a time, running a business of a certain size required a team. AI is turning that assumption upside down, and more aspiring entrepreneurs are going it alone.

An analysis by the payments company Stripe shows there are thousands of solo operators on the company’s platform that are generating over $1 million in revenue, with their ranks doubling between 2023 and 2025. The number of solo operators crossing the $10 million threshold nearly tripled in that same span.

In the past, people without business contacts or particular savvy might not have known how to get their ideas off the ground, said Ernie Tedeschi, Stripe’s chief economist. “Now, AI can be a built-in business partner,” he said.

AI’s ability to handle various administrative tasks makes it potentially useful for launching solo businesses in many fields. But the technology’s ability to also handle key tasks in tech, like coding, make that field a particular hot spot.

Analyzing Census Bureau data, Bank of America Institute economist Taylor Bowley found that among all industries, new business applications in the information sector have seen the biggest percentage increase—nearly 45%—over the past year. At the same time, the rate of information-sector applicants saying they plan to hire workers has experienced the sharpest decline of any measured industry.

This Census dataset doesn’t track solo-operated businesses. But the numbers broadly show—in tech and beyond—that applications are flat among businesses likely to hire workers, but generally rising elsewhere. Economists say that’s a strong sign that solo operators are on the upswing.

“The bar for getting started has never been lower,” said Julian Weisser, who runs a San Francisco-based accelerator for solo founders working in tech. The accelerator—which offers founders seed money and mentorship in exchange for an equity stake—attracted 4,500 applicants for 10 slots made available in its most recent cycle, nearly five times the number it drew when it launched last May.

Going it alone with AI can still be surprisingly expensive. Broca said he was losing money on many customers’ accounts while paying to access Anthropic’s Claude to run his clients’ requests—that AI company, as well as others, charges based on usage. He has since switched to free open-source AI models from China.

Broca said he has raised $30 million from investors and, at the same time, has saved millions in salary since he hasn’t needed a team of software engineers.

Another risk: If it’s easy for one entrepreneur to launch an AI-assisted business, copying them can be easy, too. This creates anxiety for founders like Troy Johnston, who runs an AI-assisted business alone in Orlando, Fla.

“Everybody has the sword and we all have the ability to unsheathe Excalibur now,” said Johnston, 40, who used AI to code an app that helps people get the most out of credit card benefits. The company makes around $3,000 a month in profit, with no employees, and is continuing to grow.

What one-person businesses will mean for the labor market remains to be seen. Polling has shown Americans are worried that AI will replace jobs, and top economists are wrestling with that possibility, too. But AI is also creating lots of new jobs, and the go-it-alone entrepreneurs show how the technology can both open doors and limit employment opportunities.

“If everyone’s hiring less, but you get four times more firms, what does that do to head count?” said Rembrand Koning, an associate professor at Harvard Business School who studies entrepreneurship. He co-authored a recent study that found that among 50,000 startups the researchers examined, those focused on AI tended to operate with 25% fewer employees.

Koning also believes a soft hiring environment that’s left some people mired in long job searches has encouraged more to try their hand at launching businesses.

Some founders cite different motives. “It’s a perfect storm of post-pandemic burnout and a re-evaluation of one’s priorities, and also booming AI and a sense of what’s possible,” said Samir Ahmad, 39, who lives in Breinigsville, Pa.

Two years ago, Ahmad decided to leave the corporate job he had worked at Verizon for almost two decades to start a solo coaching and consulting business. He had been seeing social-media posts touting the ease and virtues of AI, which he used to chart a business plan and help with marketing. “It was like my chief of staff, a second in command,” he said.

The business ultimately petered out within months, though, and Ahmad is now back to a full-time corporate role with a utility company.

For Claire Vo, 41, AI helped her turn a passing impulse into a business. She was working full-time as a tech executive when she tapped AI in late 2023 to help code an app that would help her manage documentation and design for new products, with customers ranging from financial services to healthcare firms.

“I was copying and pasting from ChatGPT,” said Vo, who lives in San Francisco.

She put the app online for $1 a month, and within weeks people downloaded it thousands of times. Nearly three years later, Vo’s company—which she ran solo for nine months before hiring an engineer—now has 100,000 users and is on track to make seven figures in profit this year. AI handles the company’s marketing, sales and customer support.

While AI is a shortcut, Vo said her network and credibility in the industry were key. “I think people over-index on how easy AI is and under-index on how much I did to get to this point,” she said.

When the Writers Festival was called off and the skies refused to clear, one weekend away turned into a rare lesson in slowing down, ice baths included.

ABC Bullion has launched a pioneering investment product that allows Australians to draw regular cashflow from their precious metal holdings.