Tougher Return-to-Office Policies Are No Remedy for Half-Empty Buildings

Office owners are struggling with near record-high vacancy rates

3 min

3 min

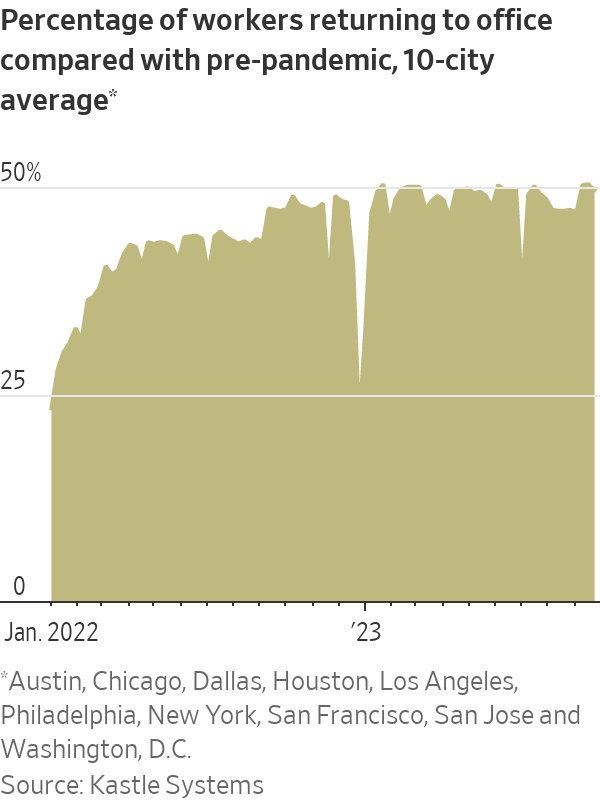

First, the good news for office landlords: A post-Labor Day bump nudged return-to-office rates in mid-September to their highest level since the onset of the pandemic.

Now the bad: Office attendance in big cities is still barely half of what it was in 2019, and company get-tough measures are proving largely ineffective at boosting that rate much higher.

Indeed, a number of forces—from the prospect of more Covid-19 cases in the fall to a weakening economy—could push the return rate into reverse, property owners and city officials say.

More than before, chief executives at blue-chip companies are stepping up efforts to fill their workspace. Facebook parent Meta Platforms, Amazon and JPMorgan Chase are among the companies that have recently vowed to get tougher on employees who don’t show up. In August, Meta told employees they could face disciplinary action if they regularly violate new workplace rules.

But these actions haven’t yet moved the national return rate needle much, and a majority of companies remain content to allow employees to work at least part-time remotely despite the tough talk.

Most employees go into offices during the middle of the week, but floors are sparsely populated on Mondays and Fridays. In Chicago, some September days had a return rate of over 66%. But it was below 30% on Fridays. In New York, it ranges from about 25% to 65%, according to Kastle Systems, which tracks security-card swipes.

Overall, the average return rate in the 10 U.S. cities tracked by Kastle Systems matched the recent high of 50.4% of 2019 levels for the week ended Sept. 20, though it slid a little below half the following week.

The disappointing return rates are another blow to office owners who are struggling with vacancy rates near record highs. The national office average vacancy rose to 19.2% last quarter, just below the historical peak of 19.3% in 1991, according to Moody’s Analytics preliminary third-quarter data.

Business leaders in New York, Detroit, Seattle, Atlanta and Houston interviewed by The Wall Street Journal said they have seen only slight improvements in sidewalk activity and attendance in office buildings since Labor Day.

“It feels a little fuller but at the margins,” said Sandy Baruah, chief executive of the Detroit Regional Chamber, a business group.

Lax enforcement of return-to-office rules is one reason employees feel they can still work from home. At a roundtable business discussion in Houston last week, only one of the 12 companies that attended said it would enforce a return-to-office policy in performance reviews.

“It was clearly a minority opinion that the others shook their heads at,” said Kris Larson, chief executive of Central Houston Inc., a group that promotes business in the city and sponsored the meeting.

Making matters worse, business leaders and city officials say they see more forces at work that could slow the return to office than those that could accelerate it.

Covid-19 cases are up and will likely increase further in the fall and winter months. “If we have to go back to distancing and mask protocols, that really breaks the office culture,” said Kathryn Wylde, head of the business group Partnership for New York City.

Many cities are contending with an increase in homelessness and crime. San Francisco, Philadelphia and Washington, D.C., which are struggling with these problems, are among the lowest return-to-office cities in the Kastle System index.

About 90% of members surveyed by the Seattle Metropolitan Chamber of Commerce said that the city couldn’t recover until homelessness and public safety problems were addressed, said Rachel Smith, chief executive. That is taken into account as companies make decisions about returning to the office and how much space they need, she added.

Cuts in government services and transportation are also taking a toll. Wait times for buses run by Houston’s Park & Ride system, one of the most widely used commuter services, have increased partly because of labor shortages, according to Larson of Central Houston.

The commute “is the remaining most significant barrier” to improving return to office, Larson said.

Some landlords say that businesses will have more leverage in enforcing return-to-office mandates if the economy weakens. There are already signs of such a shift in cities that depend heavily on the technology sector, which has been seeing slowing growth and layoffs.

But a full-fledged recession could hurt office returns if it results in widespread layoffs. “Maybe you get some relief in more employees coming back,” said Dylan Burzinski, an analyst with real-estate analytics firm Green Street. “But if there are fewer of those employees, it’s still a net negative for office.”

The sluggish return-to-office rate is leading many city and business leaders to ask the federal government for help. A group from the Great Lakes Metro Chambers Coalition recently met with elected officials in Washington, D.C., lobbying for incentives for businesses that make commitments to U.S. downtowns.

Baruah, from the Detroit chamber, was among the group. He said the chances of such legislation being passed were low. “We might have to reach crisis proportions first,” he said. “But we’re trying to lay the groundwork now.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

A Name Steeped in History, A Home Built for the Future. Timeless architecture, premium residences, and an exceptional Inner West location come together at Maybelle. With construction nearing completion, buyers can move into their brand-new home by the end of the year and purchase with confidence, knowing their home is backed by 10-Year Latent Defects Insurance.

3 min

Almost a century before construction began, two sisters unknowingly inspired one of Sydney’s newest residential addresses.

Local landowner and developer John Henry Schroeder combined his daughters’ names, Isobel and May, to create Ismay Avenue, a street name that has become part of the area’s identity, still visible today in Ismay Reserve. The Maybelle borrows that story rather than inventing one. It takes its name from Isobel and May, drawing a direct line between the development and the history sitting right outside its front door.

More than simply another apartment building, it reflects a vision of creating homes that honour the past while looking confidently to the future.

Developed and built by Omaya, a family-owned company with more than 35 years of experience, The Maybelle reflects a commitment to craftsmanship, quality and creating communities that stand the test of time.

Located beside Ismay Reserve, the boutique collection of one, two and three-bedroom residences combines timeless architecture by Squillace Architects, premium interiors and exclusive resident amenities within one of Sydney’s most connected Inner West locations.

Location is one of The Maybelle’s defining strengths, residents are moments from train stations, bus services and the M4 Motorway.

Positioned just moments from North Strathfield, Bakehouse Quarter, Sydney Olympic Park, Parramatta and the Sydney CBD, residents enjoy the perfect balance of green open space, vibrant local amenity and exceptional connectivity.

Surrounded by cafés, restaurants, leading public and private schools, shopping and parklands, The Maybelle offers a lifestyle where everything is within easy reach.

Designed to embrace its unique park-side setting, many residences enjoy expansive balconies overlooking Ismay Reserve, while selected homes capture elevated views across the Sydney Harbour Bridge and city skyline.

Spacious open-plan layouts, premium fixtures and finishes, and two carefully curated interior schemes create homes that are both beautifully refined and designed for everyday living.

The lifestyle extends well beyond each apartment. Residents will enjoy exclusive access to a full-level Garden Pavilion on Level 8, featuring beautifully landscaped spaces for entertaining, recreation, remote working and gathering with family, friends and neighbours.

Complementing this is the elevated Sky Terrace on Level 14, where sweeping Sydney Harbour Bridge and city skyline views create a tranquil setting to relax, recharge and enjoy the remarkable outlook.

As both developer and builder, Omaya oversees every stage of the project – from planning through to construction – ensuring quality, accountability and meticulous attention to detail throughout.

Buyers can also purchase with confidence, knowing The Maybelle is protected by 10-Year Latent Defects Insurance, providing additional peace of mind long after settlement.

With construction nearing completion, buyers will be moving into their brand-new homes by the end of the year, offering a rare opportunity to secure a premium residence without the lengthy wait often associated with off-the-plan developments.

For those seeking more than just a new apartment, The Maybelle offers something increasingly rare – a home with an authentic story, a genuine connection to its surroundings and a lifestyle that brings together heritage, nature, connectivity and contemporary design in one exceptional address.

Now selling premium one, two and three-bedroom residences. To learn more or book a private appointment, visit www.themaybelle.com.au or call 1300 066 292.

The grand harbourside residence combines sweeping Sydney Heads views, resort-style entertaining and refined designer finishes with a reported $36 million price guide.

From snow-dusted valleys to festival-filled autumns, Bhutan reveals itself as a rare destination where culture, nature and spirituality unfold year-round.