Home Sales on Track for Worst Year Since 1995

September sales fell 3.5% from a year earlier. In 2023, home sales hit their lowest point in 30 years.

5 min

5 min

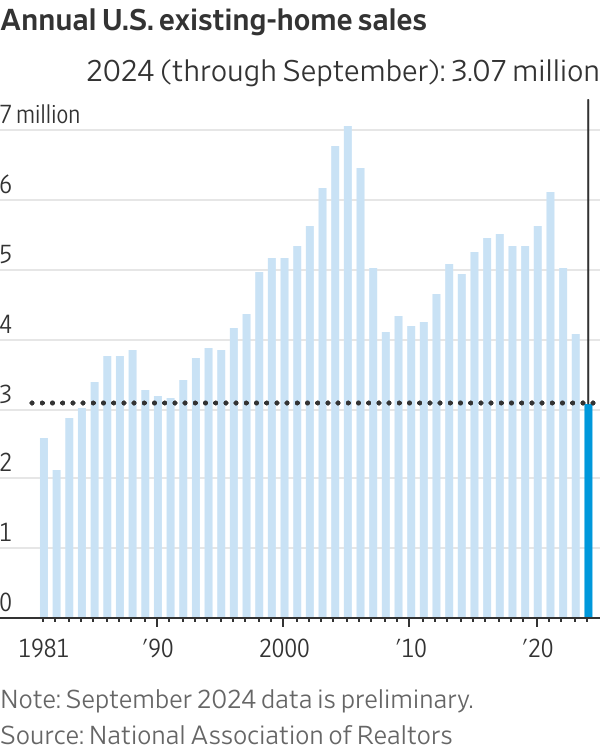

Sales of existing homes in the U.S. are on track for the worst year since 1995— for the second year in a row.

Persistently high home prices and elevated mortgage rates are keeping potential home buyers on the sidelines. Sales of previously owned homes in the first nine months of the year were lower than the same period last year, the National Association of Realtors said Wednesday.

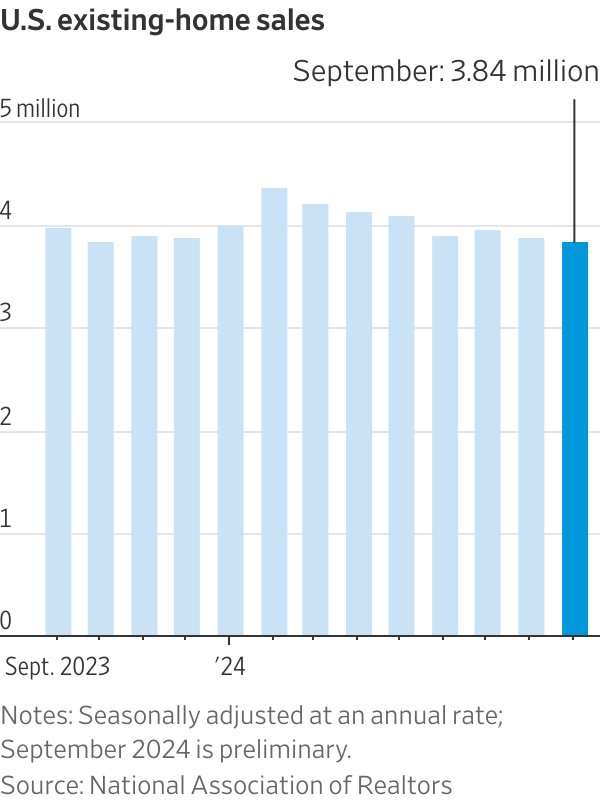

Existing-home sales in September fell 1% from the prior month to a seasonally adjusted annual rate of 3.84 million, NAR said, the lowest monthly rate since October 2010. Economists surveyed by The Wall Street Journal had estimated a monthly decrease of 0.5%.

September sales fell 3.5% from a year earlier.

After a sluggish 2023, economists and real-estate executives widely expected activity to pick up in 2024.

But mortgage rates have stayed higher throughout the year than some had forecast, including in recent weeks after the Federal Reserve’s interest-rate cut last month. That has kept home-buying affordability low .

Home prices have continued to rise, as inventory in many parts of the country is still below normal historical levels. Climbing home insurance costs and a coming election are also adding to buyers’ uncertainty.

“Home sales are stuck at low levels,” said Lawrence Yun , NAR’s chief economist. “Americans are really not moving.” Yun said he forecasts that existing-home sales for 2024 as a whole could match or be slightly below last year’s level.

Expectations that the Fed would cut rates this year caused mortgage rates to drop to 6.08% in September, a two-year low. But the move came too late in the year to lure buyers, real-estate agents say. Many families prefer to purchase in the spring and move houses between school years.

The reprieve in rates also didn’t last long. Mortgage rates have risen for three straight weeks to the highest level since August.

“That trickle up in rates, to right back where we were, just sucked the air out,” said Michael Read, owner of Bridgeway Mortgage & Real Estate Services in Morristown, N.J.

Mortgage rates tend to loosely follow the yield on the 10-year Treasury note, which has been above 4%. But the spread between mortgage rates and the 10-year has widened to above historical norms in recent years, which can push up borrowing costs.

Lenders often sell mortgages to investors. Those investors demand a bigger return, particularly when rate volatility is higher than normal, because mortgages are riskier than ultrasafe government bonds.

Uncertainty around the presidential election and “murkiness” around recent labor and inflation data haven’t helped, said Mike Fratantoni , chief economist at the Mortgage Bankers Association.

Mortgage applications have fallen for four straight weeks as rates have risen.

“It’s tough in this business,” said Alex Elezaj , chief strategy officer at United Wholesale Mortgage. “Once you think it’s going one way, it goes another.”

A drop in mortgage rates later this year or next would make home purchases more affordable, but that benefit could be offset if home prices continue to rise. In September, 42% of more than 1,000 people surveyed said they expect mortgage rates to fall in the next 12 months, but 39% said they expect home prices to rise over the same period, according to Fannie Mae .

The national median existing-home price in September was $404,500, a 3% increase from a year earlier, NAR said. While that is down from the recent high, it is the highest median home price for any September, Yun said. Prices aren’t adjusted for inflation.

Widespread frustration with the housing market has made affordability an important campaign topic . Both parties have offered proposals to bring down housing costs. Vice President Kamala Harris has rolled out plans for building more housing, for example, and offering help with down payments. Former President Donald Trump has proposed cutting regulations and allowing more building on federal land.

For the buyers who are able to jump into the market now, there is less competition and more room to negotiate. The typical home sold in September was on the market for 28 days, up from 21 days a year earlier, NAR said.

Lucy and Graham Schroeder tried buying a house in the suburbs of Madison, Wis., in 2023 and again this past spring, but they got outbid by other buyers. When they re-entered the market this summer, “it felt like something kind of shifted,” Graham Schroeder said. “Houses were kind of sitting a little bit.”

The couple bought a five-bedroom home in August for $585,000, about 5% below the listing price, and sold their smaller home for $330,000.

The number of homes for sale or under contract rose 23% in September from a year earlier, NAR said, but it remains below normal levels in many markets. Many homeowners who locked in low rates on their current mortgages a few years ago are staying put, because they are reluctant to take on a new loan at a higher rate.

At the current sales pace, there was a 4.3-month supply of homes on the market at the end of September. That is at the low end of what is considered a balanced market between buyers and sellers.

David Schlichter

Kaitlin Skilken and Matt Adler experienced the cool-down in the market firsthand. The couple competed against other buyers to purchase a house this spring in Wheat Ridge, Colo. But when they listed their townhouse in a nearby city for sale in June, it sat for almost two months.

Other units in the community were also sitting on the market, and the homeowner association’s insurance policy didn’t comply with every lender’s requirements, making it more difficult for buyers to get a mortgage, Adler said. “‘You only need one buyer,’ is what I kept saying,” Skilken said.

The couple sold the townhouse in September for the $475,000 asking price, and they paid a $12,000 credit to the buyers for some home repairs and to help lower the buyers’ interest rate.

Home-buying activity typically slows during the holiday season. Some real-estate agents say they expect sidelined buyers to re-enter the market in early 2025.

“It’s not like all of a sudden people have stopped needing to buy houses,” said David Schlichter, a real-estate agent in Denver. “You can only defer for so long.”

News Corp , owner of the Journal, also operates Realtor.com under license from NAR.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

The influencer and fitness entrepreneur is offloading the four-bedroom Main River residence she has called home since 2020 following her split from ex-husband Matt Zukowski.

< 1 min

Fitness entrepreneur and social media personality Tammy Hembrow has put her Broadbeach Waters mansion on the market, ending a six-year stint in the riverfront home she has regularly featured in content shared with her millions of followers.

Hembrow bought the property in June 2020 for $2.88 million.

Sitting on an oversized 979sqm allotment with north-east orientation and more than 30 metres of river frontage, the double-storey residence is set behind security gates at the end of a quiet cul-de-sac.

The home has been a fixture of Hembrow’s online presence for years, serving as the backdrop to family life and business updates for the mother-of-three, who also lived there with her former husband, Love Island Australia star Matt Zukowski, before the pair separated in mid-2025 following a brief marriage.

Inside, the residence centres on an open-plan kitchen, lounge and dining area that opens onto the pool and alfresco entertaining space, designed to make the most of the Gold Coast’s indoor-outdoor lifestyle.

Upstairs, the master suite includes a walk-through robe, dedicated dressing room and ensuite, alongside two further bedrooms, while a fourth bedroom downstairs offers separate access for guests or extended family. A multi-purpose room adds flexibility for use as a media room, home office or children’s retreat.

Outdoor features include a tiled pool, built-in barbecue and bar area, firepit and private boat ramp — amenities suited to the waterfront entertaining lifestyle the Broadbeach Waters pocket is known for.

The property is being marketed by Jay Helprin of Ray White through an expressions of interest campaign, with private inspections only and no scheduled public opens.

Hembrow, who built her public profile from 2014, documenting her fitness journey through three pregnancies, went on to launch fitness app TammyFit, which has since been downloaded more than a million times.

Margot Robbie and Jacob Elordi star in an adaptation of the classic novel that respects the romance’s slow burn.

Warmer minimalism, tactile materials and wellness focused layouts are redefining luxury interiors as homeowners design for comfort, connection and lasting appeal.