Top U.S. Cities Where Affluent Home Buyers Can Snag a Deal This Fall

5 min

5 min

An opportunity could be on the horizon for those who deferred a home purchase in some of the luxury real estate markets that boomed during the pandemic as demand falls.

Among them, the Miami and Naples areas of Florida; urban Honolulu; and Santa Fe, New Mexico, could be among the best luxury markets in the U.S. for buyers this fall, according to data Realtor.com provided to Mansion Global. The data was staked on a combination of falling luxury median price points, which indicate markets that are softening and where buyers could potentially score a deal; a shift in median days on market; and page views, with fewer views indicating less demand.

“We see that these higher-priced markets are seeing falling demand,” said Hannah Jones, senior economic research analyst at Realtor.com . “And so for buyers who do have access to the capital that they could purchase in one of these markets, they may find more flexibility than in some of the markets that are lower priced and are still seeing a ton of competition.”

Read on for where the opportunity lies and advice in those markets from real estate agents on the ground.

Miami, Fort Lauderdale and Pompano Beach, Florida

Buyers who couldn’t get enough of the sandy shores of this trio of South Florida cities during the pandemic have largely backed off, making it the No. 1 destination for luxury buyers this fall.

The luxury median listing price in Miami, Fort Lauderdale and Pompano Beach was down 22% to $2.5 million in the second quarter. Between June 2023 and June 2024, the median days on market for luxury listings rose five days and in the same time page views of luxury properties on Realtor.com fell a whopping 44%.

Mick Duchon, a Miami-based agent with Corcoran, said that some sellers who were stuck in the high-price mindset of 2021 and part of 2022 are starting to come around, meaning there are still properties out there with a listing price ripe for an adjustment. He said it’s an opportunity for people who have been waiting on the sidelines.

Case in point, Duchon was working with a buyer on a penthouse apartment in the South of Fifth neighbourhood in the summer of 2022, when the market had just started to adjust from its pandemic highs. After approaching the seller with a deal and agreeing on it, the buyer decided to wait. undefined undefined “Two years later, we transacted at 15% below that initial contract price,” on the same penthouse with the same buyer and seller, he said.

He added, “If buyers are basing their offers on what has transacted recently, then they should be able to achieve a solid deal.”

Pixabay

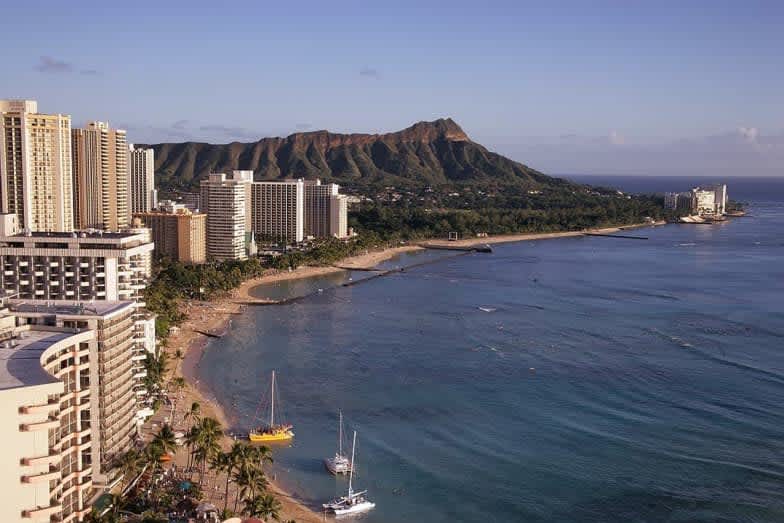

Honolulu

Realtor.com found that the median luxury listing price in Honolulu fell nearly 10% to $2.34 million in the second quarter. In June, the median days on market for luxury listings fell 11 days compared to a year ago, while in the same time frame, luxury page views fell 31%, indicating less interest, making Honolulu the No. 2 market for buyers this fall.

Noel Shaw, an agent with Hawai’i Life Real Estate Brokers Forbes Global Properties, said the peak Covid rush to Honolulu has abated somewhat, but other buyers who decided to change their lifestyle and move there as part of their 10-year plan are still trickling in. It’s keeping competition up for those mid-tier luxury listings and makes it imperative to work with an agent who knows the city like the back of their hand. (Shaw grew up in Honolulu, and said the quality of real estate varies block by block.)

“This is an island, the city’s very limited so we still have a limited supply,” she said. “So while there are going to be some great deals within the city, it’s not going to be as easy or obvious as other cities.” undefined undefined The listings luxury buyers should keep an eye out for are the top-tier properties of Japanese sellers, she said. Honolulu is a prestigious second-home market for Asians, Shaw said, but the weakness of the yen right now means that some Japanese owners may choose to sell and convert their funds back to yen. Those prized properties, which are rare in Honolulu because of the constraints on inventory, are the extra sweet spot for luxury buyers looking for top-of-the-line properties these days, she said.

Naples-Marco Island, Florida

The market frenzy has quelled in this Gulf Shore slice of Florida, with the luxury median listing price down 18% to $4 million in the second quarter. The median days on market over the year ending June is the same as the year prior, at 85, but page views on luxury properties are down over 11% in the same time period, bringing the Naples-Marco Island metro into the No. 3 spot. undefined undefined “We’re over the Covid mania, where people came and purchased properties at any price,” said Celine Wells, an agent with Douglas Elliman. “What we’re seeing now is less volume of sales, but very strong sales.”

For potential buyers, “patience is a virtue,” said Chris Wells, Celine’s business partner and husband. Chris added it’s important to have knowledge of the market so you can act quickly when a particularly interesting property comes to market. Most transactions happen in cash, with mortgages brought into the picture post-closing, he said.

He added, “A nice deposit, a quick closing, a cash deal, a short due-diligence period—these are things that help a buyer get the property they desire.”

Pixabay

Santa Fe, New Mexico

The Sunbelt and Mountain West experienced huge demand in recent years, and the small in-between market of Santa Fe was not immune to that.

Unlike the other cities on this list, demand is still up there, with luxury page views surging nearly 7% and luxury median days on market falling 33 days, to 86, between June 2023 and June 2024. Prices, however, are trending down, with the luxury median listing price having fallen nearly 14% to $2.98 million from April to June. All together, it makes Santa Fe the fourth-best market for luxury buyers this fall. undefined undefined “People are still wanting to come here. Santa Fe is still very, very desirable,” said Ricky Allen of Sotheby’s International Realty – Santa Fe Brokerage. “They’re coming for the size of the city, the climate, the culture, the lifestyle. … I think it’s a good time to be a buyer.” undefined undefined Allen suggested that buyers see as many properties as possible that check most of their boxes. “You never know what those properties are going to end up selling at,” he added.

(Mansion Global is owned by Dow Jones. Both Dow Jones and Realtor.com are owned by News Corp.)

This article was originally published on Mansion Global.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

The influencer and fitness entrepreneur is offloading the four-bedroom Main River residence she has called home since 2020 following her split from ex-husband Matt Zukowski.

< 1 min

Fitness entrepreneur and social media personality Tammy Hembrow has put her Broadbeach Waters mansion on the market, ending a six-year stint in the riverfront home she has regularly featured in content shared with her millions of followers.

Hembrow bought the property in June 2020 for $2.88 million.

Sitting on an oversized 979sqm allotment with north-east orientation and more than 30 metres of river frontage, the double-storey residence is set behind security gates at the end of a quiet cul-de-sac.

The home has been a fixture of Hembrow’s online presence for years, serving as the backdrop to family life and business updates for the mother-of-three, who also lived there with her former husband, Love Island Australia star Matt Zukowski, before the pair separated in mid-2025 following a brief marriage.

Inside, the residence centres on an open-plan kitchen, lounge and dining area that opens onto the pool and alfresco entertaining space, designed to make the most of the Gold Coast’s indoor-outdoor lifestyle.

Upstairs, the master suite includes a walk-through robe, dedicated dressing room and ensuite, alongside two further bedrooms, while a fourth bedroom downstairs offers separate access for guests or extended family. A multi-purpose room adds flexibility for use as a media room, home office or children’s retreat.

Outdoor features include a tiled pool, built-in barbecue and bar area, firepit and private boat ramp — amenities suited to the waterfront entertaining lifestyle the Broadbeach Waters pocket is known for.

The property is being marketed by Jay Helprin of Ray White through an expressions of interest campaign, with private inspections only and no scheduled public opens.

Hembrow, who built her public profile from 2014, documenting her fitness journey through three pregnancies, went on to launch fitness app TammyFit, which has since been downloaded more than a million times.

International AI strategist Justin Kabbani will headline the Kanebridge Property Summit in Sydney on June 18, with tickets selling fast.

Rugged coastal drives and fireside drams define a slow, indulgent journey through Scotland’s far north.