America’s Empty Apartments Are Finally Starting to Fill Up

If that demand is sustained, landlords likely will have more pricing power starting sometime next year

3 min

3 min")

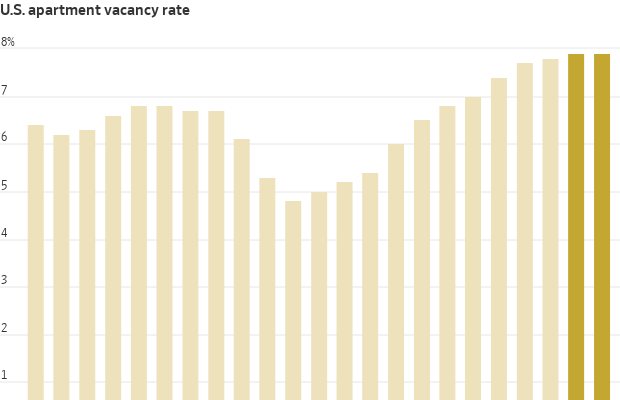

The biggest apartment construction boom in four decades flooded the market with new supply over the past two years. Apartment owners had to contend with a surge in empty units.

That is starting to change.

The vacancy rate, or the share of apartment units that are empty, stopped rising for the first time in three years last quarter, as demand for apartments rose to its highest levels since 2021, according to CoStar .

The more than 1.2 million new apartment units that were built during the past two years are filling up. If that demand is sustained, if the economy remains strong and if housing prices remain near record highs, landlords likely will have more pricing power starting sometime next year. That could allow building owners to raise rents more than they have recently.

Some 672,000 new apartment units will have been completed by the end of this year, but only about half that number is expected in 2025, and even fewer in 2026, CoStar said.

“The worst of the pressures on pricing from new supply are likely behind us,” said Eric Bolton , chief executive of publicly traded landlord Mid-America Apartment Communities , on an October earnings call.

Housing affordability has become a hot-button election issue at the federal and local levels. Any sign that rents are poised to rise in 2025 could intensify pressure on the new administration to address housing costs. President Biden announced a plan over the summer to cap rent increases, though it would need to pass Congress.

Nationally, sales of apartment buildings have also started to pick up again, as investors become more confident that the market is bottoming and sellers are more willing to acquiesce on price.

Renters were hit hard by the historically high rent increases during the pandemic years, especially in Sunbelt cities, such as Phoenix and Tampa, Fla., where rents rose 20% or more during 12-month periods.

Rents for new leases nationwide have held close to flat for more than a year. That is due in part to a big split between supply-heavy Sunbelt cities, some of which have seen rent cuts, and the rest of the country, which hasn’t.

Renters who choose to renew their leases were still paying a 3.5% rent increase on average as of this past August, the most recent month data was available from Yardi Matrix.

Throughout this year, the places with the highest renewal rent growth have been on the coasts and in the Midwest. New York City, Los Angeles, Indianapolis and Columbus, Ohio, saw renewal rent increases of 5% or more in July, according to Yardi.

Increased return to office orders in major employment hubs may also start translating into even more urban rental demand soon, especially in coastal cities.

In Seattle, Equity Residential said in an October earnings call that it is seeing a pickup in leasing from Amazon employees, who are locking in apartments ahead of a five-day office attendance policy, scheduled to begin in January.

On the flip side is Austin, Texas, which has experienced a building boom after companies such as Tesla and Oracle moved offices there. Austin’s vacancy rate, if new buildings are included, is the highest in the country at over 15%, according to CoStar.

Rent growth for new leases in the Texas capital ranks last among major metros during the past year. Landlords of new luxury buildings are still offering big concessions, such as months of free rent, to fill up units. undefined undefined “Basically, the worst apartment market in the country right now is Austin,” said Matt Rosenthal , managing partner of multifamily investor Eastham Capital.

On an annual basis, apartment building sales have grown for two consecutive quarters, according to MSCI Real Assets. Places seeing some of the biggest increases in sales include Denver, San Francisco and the Washington, D.C. suburbs.

Apartment companies also continue to feel tailwinds from renters locked out of homeownership. Major owners have remarked on how few of their renters move out to purchase homes now, amid some of the worst conditions for home-purchase affordability in four decades. That is unlikely to change much in 2025.

“Probably the biggest story this year that we’ve seen [is] from people coming in the front door and then not leaving [out] the back door,” said Joe Fisher , president of publicly traded apartment owner UDR .

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

The influencer and fitness entrepreneur is offloading the four-bedroom Main River residence she has called home since 2020 following her split from ex-husband Matt Zukowski.

< 1 min

Fitness entrepreneur and social media personality Tammy Hembrow has put her Broadbeach Waters mansion on the market, ending a six-year stint in the riverfront home she has regularly featured in content shared with her millions of followers.

Hembrow bought the property in June 2020 for $2.88 million.

Sitting on an oversized 979sqm allotment with north-east orientation and more than 30 metres of river frontage, the double-storey residence is set behind security gates at the end of a quiet cul-de-sac.

The home has been a fixture of Hembrow’s online presence for years, serving as the backdrop to family life and business updates for the mother-of-three, who also lived there with her former husband, Love Island Australia star Matt Zukowski, before the pair separated in mid-2025 following a brief marriage.

Inside, the residence centres on an open-plan kitchen, lounge and dining area that opens onto the pool and alfresco entertaining space, designed to make the most of the Gold Coast’s indoor-outdoor lifestyle.

Upstairs, the master suite includes a walk-through robe, dedicated dressing room and ensuite, alongside two further bedrooms, while a fourth bedroom downstairs offers separate access for guests or extended family. A multi-purpose room adds flexibility for use as a media room, home office or children’s retreat.

Outdoor features include a tiled pool, built-in barbecue and bar area, firepit and private boat ramp — amenities suited to the waterfront entertaining lifestyle the Broadbeach Waters pocket is known for.

The property is being marketed by Jay Helprin of Ray White through an expressions of interest campaign, with private inspections only and no scheduled public opens.

Hembrow, who built her public profile from 2014, documenting her fitness journey through three pregnancies, went on to launch fitness app TammyFit, which has since been downloaded more than a million times.

Three completed developments bring a quieter, more thoughtful style of luxury living to Mosman, Neutral Bay and Crows Nest.

Travellers are swapping traditional sightseeing for immersive experiences, with Africa emerging as a must-visit destination.