More than one in three Australians admit they have spent more than they intended on a date to impress their partners or a new love interest. A Finder survey of 1,070 people found 14 percent have spent more than they could afford on dates, while a further 21 percent say they have also gone over budget but could afford to do so.

Finder’s money expert, Rebecca Pike, said: “Millions of people are finding that their simple quest to find love is derailing their financial wellbeing. Aussies have less disposable income in general due to the cost of living crisis, and spoiling a potential love interest or overspending on a date is adding to the money stress.”

The research found younger singles were more likely to go over budget on dates, with 23 percent of Gen Z respondents and 22 percent of Millennials spending more than they could afford versus just seven percent of Gen Xers and five percent of baby boomers.

Ms Pike said Aussies should start with simple, affordable dates with someone new.

“’Fake it until you make it’ is a risky dating strategy. You may get stuck with some spending habits and decisions that you’re paying off long after the romance has fizzled out.”

While many Australians are prepared to go over budget to woo a beau or belle,another survey shows some people are becoming less inclined to shout a round or pick up the bill when dining out and socialising with family and friends.

A survey of 2,000 Australians by NAB Economicsfound 54 percent prefer to split the bill these days, with this figure rising to 72 percent among 18 to 29 year-olds.

“Young Australians are embracing ‘loud budgeting’ and getting more comfortable with talking about their financials,” said NAB personal everyday banking executive, Kylie Young. “It isn’t surprising that extends to splitting the bill, as they confidently step away from the social pressure of ‘shouting a round’.”

The majority of older Australians are still paying for each other, with only 32 percent of over-65ssaying today’s high cost of living made them more inclined to split the bill. Interestingly, splitting bills is least common among low-income earners(39 percent) and more common among high–incomeearners (63 percent). When separating the bill, almost four in 10 prefer one person to pay and the others to transfer their share. About three in 10 prefer to pay their share with a debit or credit card.

Great architectural design and exceptional food are two of life’s great indulgences. When these two worlds collide, the result is a landmark residence made for entertaining that is also easy on the eye.

Case in point; Italian restaurateur and art aficionado Rinaldo Di Stasio tasked his friend the late architect Allan Powell with crafting a home away from home atop a hill in the picturesque Yarra Valley.

In 1988, Di Stasio opened St Kilda’s Cafe Di Stasio, which has often been lauded as Melbourne’s best Italian restaurant.

Previously listed with expectations of between $9.5 million and $10 million, the house has now resurfaced with new agent Kathy Purcell of Barry Plant Doncaster East and a fresh asking price of $8.5 million to $9.35 million.

The property is in the middle of prime wine producing country in the Yarra Valley.

“The wow factor of this property is not only its location in the heart of the Yarra Valley — and the fact that it has been a prime wine-producing estate – but it has been architecturally designed by the great Allan Powell. It’s unlike anything I’ve seen before in this country,” Purcell says.

“And although it’s a very elite home, at the same time, it’s got some really cosy elements. When Rinaldo would spend time there with his family, and he wasn’t entertaining, it could be set up as a really intimate space.”

Set in the rolling green landscape of Gruyere 60kms east of Melbourne, the 32.37ha property is part gallery, part trophy home surrounded by close to 3ha of vines and the Warramate Flora Fauna Reserve.

The house is part gallery, part trophy home and has hosted several substantial parties with ease.

Built in 1995, the unique residence features an industrial aesthetic and a spacious three-bedroom floorplan wrapped around a central courtyard with sweeping district views over the private vineyard and Great Dividing Range. In years past, the home grown wine produced at the estate was served in Di Stasio’s Melbourne restaurants.

Created as a great entertainer, the Gruyere estate has hosted several high profile soirees and the commercial-grade kitchen, complete with butler’s pantry, has proven its worth during large-scale events.

“There have been some great events held there over the years as it’s an idyllic venue. If I look at the potential buyer, I can see either a business person who wants to entertain or simply keep it as an exclusive getaway,” Purcell adds.

Beyond the vast courtyard filled with more than a dozen plane trees and a reflection pool, the home’s dramatic entry foyer is a long gallery acting as a reception room connecting the outside world with the more intimate living spaces.

Past the reception, the lounge and dining rooms feature warming fireplaces and the adjoining primary suite sits separated from the remaining bedrooms. This main retreat has a walk-in wardrobe plus a bath ensuite and sliding doors to the great outdoors.

In 2007 Powell’s son, Hugo, was commissioned to add the striking swimming pool that seemingly floats above the natural landscape simultaneously capturing the panorama while also hiding a versatile studio space below.

In addition to the pool and sun deck, as well as the vines, the rolling estate also has a private 5km walking track and two dams. It is 11kms from both the townships of Coldstream and Healesville.

Expressions of interest on 12 Range Rd, Gruyere close on Friday, August 30 at 5.00pm.

Estimated sale price: $8.5 million to $9.35 million

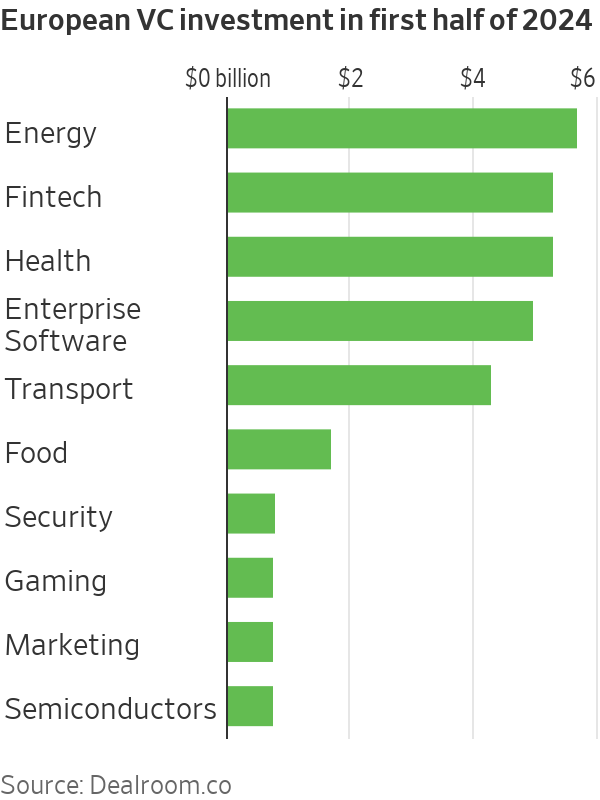

Venture capitalists’ appetite for energy and artificial-intelligence investments is putting Europe’s venture sector on a hot streak.

European governments’ focus on energy security amid heightened geopolitical tensions has helped spur a capital rush, investors and analysts say. That coupled with the emergence of Europe-based AI startups, which can be less expensive than their U.S. counterparts, is also drawing investors.

European startups raised $15.5 billion in the second quarter, up 14% from the first quarter and up 12% from the same quarter of last year, according to Europe-based analytics firm Dealroom.co. Meanwhile, the amount invested into North American startups rose 9.6% in the second quarter from the prior quarter while Asia deal value rose 6.4% over the same period.

Energy was the most funded sector in Europe in the first half of the year, netting $5.7 billion, while funding raised by AI startups accounted for a record 18% of venture funding in Europe, up from about 11% in 2021, Dealroom.co said. Before last year, energy startups typically raised less capital than fintech, health and enterprise software startups.

Russia’s invasion of Ukraine spurred European governments—which were historically dependent on Russian fossil fuels—to develop greater energy security. Support has reached startups in the form of grants and other government-backed investment opportunities.

“It has been a major shift,” said Orla Browne , head of insights at Dealroom.co. “The exposure of energy-security issues with the invasion of Ukraine has filtered down to startups.”

Large AI deals have also drawn capital to Europe. In May, Wayve, a U.K.-based developer of autonomous driving software, raised $1 billion from investors including SoftBank Group , chip maker Nvidia and Microsoft . In June, French startup Mistral AI raised $646 million from investors including the venture arm of software giant Salesforce , General Catalyst and Lightspeed Venture Partners.

In Europe, investors say they can scoop up shares of startups for less money compared with the prices that their counterparts in the U.S. command. Meanwhile, Europe’s technical universities are supplying promising entrepreneurs, particularly in the AI field.

“We have hired a world-class team at salaries that cost 30% or less than you would get for a similar team in [Silicon Valley] with the caliber being as good,” said Dominic Vergine , chief executive of Monumo in Cambridge, England, which uses AI to make electric motors more efficient.

Europe’s climate regulations have also helped attract funding for energy startups, for example the European Commission’s Innovation Fund.

Danijel Višević, co-founder of Berlin-based World Fund, said funding from countries like Germany and France as well as from the European Union helped push more capital into climate startups. “Europe has started to reap the rewards of the fruits it sowed with climate tech R&D,” said Višević.

He added that given the long-term effects of climate change, funding in the sector is likely to be stable, both from venture-capital firms and governments, for years to come.

Even so, Europe’s venture sector faces some headwinds. In the second quarter, the continent saw $2.2 billion in exits, a third fewer than in the same quarter a year ago and 93% under the second quarter of 2021, a banner year for exits worldwide, according to a report by professional-services firm KPMG. Exits include initial public offerings and mergers and acquisitions and are the primary way venture investors cash out of their startup investments.

High interest rates, which typically encourage investors to divert capital away from venture to fixed-income strategies, have also hurt the industry. European startups’ second-quarter haul is far below the record $34.6 billion they netted during the same quarter of 2021.

Investors are eager for a turnaround. Last year, Planet First Partners, which has offices in London and Luxembourg, raised a €450 million fund, equivalent to $485 million, in part on the thesis that Europe’s favourable climate regulations are a financial tailwind for energy startups.

In March, the firm invested in Sunfire, a German startup developing hydrogen energy technology aimed at reducing reliance on fossil-based energy from oil, gas and coal. The investment came as part of a €215 million Series E equity funding round and included an additional term loan of up to €100 million from the European Investment Bank.

Sergio Carvalho , a partner and head of sustainability at Planet First Partners, said the firm has invested in Sunfire in part for its potential to help Europe become more energy independent. PFP’s first investment in Sunfire was before the invasion of Ukraine. “Europe has been pushing decarbonisation systematically,” Carvalho said.

Last year, Sunfire received €169 million from a European Union initiative that funds projects that address EU-wide challenges.

In July, Index Ventures, which was founded in Europe and has offices in London, San Francisco and New York, raised $2.3 billion in new funds—an $800 million venture fund and a $1.5 billion growth fund. Hannah Seal , an Index partner in London who focuses on enterprise AI deals, among other sectors, said she expects roughly half of the venture fund to be used to invest in startups that are based in Europe.

“The first half of this year was one of the busiest we’ve ever had,” Seal said about AI dealmaking in Europe. “We’re seeing a general stabilisation in the global economy which is obviously impacting sentiment.”

Wealthy individuals remain just as interested in travelling as they were last year, but costs have become a larger factor in their plans, according to a Global Travel Study conducted by WSJ Intelligence between June 27-July 19.

Of the 879 Wall Street Journal readers surveyed—who had an average age of 56, were 79% male, and had an average net worth of about US$3.5 million—94% intend to travel for leisure in the next 12 months, down just 1% from 2023. Additionally, 64% plan to travel internationally, up from last year’s 60%.

Travellers are most concerned about costs amid ongoing inflation and other economic challenges, even as 80% of respondents say they plan to increase or maintain their travel spend compared to last year.

The cost of flights and hotels is the top factor of importance for WSJ readers, with 78% concerned about prices, a nine-point increase from 2023.

“Travel is still on the up—our readers are still really enthusiastic,” says Carolyn Romano, associate director of Luxury Lifestyle Intelligence at The Wall Street Journal. “But at the same time, it’s yet another year of market volatility and inflation, so I just think they’re being a little bit more thoughtful about the way that they’re traveling.”

Availability of flights and hotels is the second-biggest issue for travellers, with 76% of readers responding that it is a factor of importance for them.

Notably, as factors of importance, both loyalty programs and discounts and deals are up 10 percentage points year over year. Romano says this increase is “pretty significant.”

“Our reader approaches every purchase as an investment of some sort, and even our reader is still taking all of these factors into consideration,” she says.

Despite rising costs, the post-Covid enthusiasm for travel remains, with 70% of respondents traveling more than they have in the past. Over the next 12 months, WSJ readers’ average anticipated spend on leisure travel is US$18,305, up from last year’s US$18,250.

As for destinations, 86% of respondents are considering traveling to Europe, down just 1% from last year. Italy is the top European country of choice—superseding the U.K.—seeing a 9% annual increase in interest.

Though most destinations, both international and domestic, included in the survey saw similar interest as last year, traveling to Asia is up 10 points from 2023, with 40% of respondents considering booking a trip to the continent. Japan ranks the highest, with 61% of respondents considering traveling there, up 6% from last year.

When making travel plans, 72% of WSJ readers say they go to family and friends for recommendations. Only 13% report consulting a travel agent, though people taking cruises are much more likely to use a travel agent.

In an era when every square metre of real estate is worth its weight in gold, something as indulgent as a home library might feel like an anachronism. If we can store thousands of books in our smartphone, why line a room with potential dust collectors?

Despite the technological revolution — or perhaps because of it — the traditional home library space is holding its ground. As work infiltrates our homes and trickles into family life, many homeowners are purposefully carving out a corner of their home in an homage to a low-tech life.

Order prevails in a glass fronted library by Groth & Sons

Reading the room

Award-winning architect Luigi Rosselli says while the pandemic may have brought the office home to the fore, he’s witnessing a revolution against remote working.

“It depends on the client, but I’m mostly seeing two generations interested in libraries. One is the older generation who grew up with books, they still read a lot and like to get up and refer to a book or even feel the ‘microwaves’ from the pages reminding them of these wonderful stories or knowledge that can be passed on through,” he says.

“Then there’s the younger generation who are working long hours in front of a computer or some other electronic device and they are rebelling. They’re reacting to a sort of technology addiction and finding instead an interest in books and reading.”

Smaller footprints, especially in city residences, are notoriously challenging when it comes to storage and function, but Rosselli says libraries needn’t be single-use spaces.

“That’s very much my challenge; people saying they want a room for this, they want a room for that,” he says. “What I’ve done quite a few times is give a dual use to libraries. In fact, books only use up wall space, so in between those walls you can have quite a lot of space leftover.”

In his Bondi Bombora project, Rosselli created a stairwell library to accommodate the resident family’s large — and growing — book collection.

“One storey wouldn’t have been enough. So a stairwell worked ideally in the sense that it now has two functions.

“We also retained an old bay window underneath the stairs to make a study nook that is cocooned and separated from an active house filled with lots of kids.”

For a book-loving calligrapher in Sydney, Rosselli designed The Books House, which resembles a random stack of books from the outside while inside there is a private library hidden behind a moving bookcase.

While a home office and library fusion seems like a perfect match, savvy design and innovative thinking can marry a library to alternative rooms.

“In my house when the children were young they had a library room where the television was not allowed, they could do homework there but also it was a relaxing space with a couch so you could sit and read,” Rosselli says. “Now our children have grown up and moved out we put a table in there.

“It’s ended up being our favourite dining area because it’s in such good company, and the acoustics of books is fantastic.”

A turn up for the books

The Books House by Luigi Rosselli has a moving bookcase.

Whether it’s a limited footprint or a client seeking a hint of James Bond-style intrigue at home, professional cabinet maker Amos Groth of Groth & Sons says libraries are only limited by imagination — and budget.

“It’s a balance of what you’d like in your wildest dreams and what we can give you practically. But we try to really push the boundaries on the aesthetics to get all those bells and whistles,” Groth says, adding that private libraries can cost between $25,000 and $250,000. “A lot of my clients tell me when they go into their libraries and close the door they’re transported to London or Bath or anywhere in the world.

“Libraries offer an element of escapism.”

Over three decades, Groth & Sons has become known as “the bespoke library outfitters” fitting books into almost any space.

“We’ve done libraries in dining rooms, in hallways, as long as you’ve got enough space to get a floor lamp, a library ladder and a comfy chair. It doesn’t have to be an entire room,” Groth says.

“Today, people realise libraries aren’t about showing off a book collection, but are more about what a space represents.

“For me, in my library, I feel like I’m surrounded by my best mates.”

A home library might seem like an old school luxury, but Groth says they have come full circle.

“When I first started, some people thought book-filled rooms were ostentatious but today they can be really practical and fun spaces. It’s about getting away from the stresses and strains of technology to go into a low-tech room for a breath of fresh air,” he says.

Floor-to-ceiling walls of books, secret doors, cabinets on hydraulics and rolling library ladders might seem like the stuff of movies but Groth says fanciful libraries do exist.

“People have the fantasy of a library ladder, it makes them feel like they’re in a film with Audrey Hepburn or Rex Harrison,” he says.

“We often get asked about secret doors — we’re currently working on one where you actually pull a book and the door opens. They’re not the cheapest things, and there’s a lot of behind-the-scenes work because you can’t just put them into a regular doorframe.

“A lot of what we do are one-offs.”

Developing a love of books

A hallway library by Groth & Sons

A challenge for homeowners “rightsizing” to apartments is giving up superfluous living spaces, but developers are taking note of what buyers want, both inside and outside their residences. Along with private dining spaces and fully-equipped wellness spaces, libraries are seen as a desirable option for buyers.

Alceon has answered the call for more communal retreats on site, starting with Akoya in Sydney’s north.

The over-55s project is home to 39 apartments but includes approximately 700sqm of common areas such as a residents-only library to be stocked with 100 books from local bookshop Constant Reader.

“It’s not a tokenistic space, it’s a purpose-built library with a fireplace, a lounging section and plenty of shelving for residents to add more books to,” said Todd Campling, development director at Alceon Group.

“Our goal with the library was to recreate the creature comforts of home for residents who might be relocating from quite substantial family homes.

“There’s also a commercial-grade bar next to the library and personal lock-up wine cellars so people can enjoy a glass while they read.”

Campling adds that as Australians, especially in major cities, move towards multi-density living, it is the developer’s responsibility to create areas where neighbours, friends and family can enjoy social moments.

“Additional amenities aren’t for everyone and they aren’t for every development, it’s about curating spaces that are the perfect blend of what you’ve had — and what you wish you had,” he says.

And as generations age and needs evolve through a building’s lifespan, he says such communal spaces should be adaptable.

“The notion of a library with the Chesterfields lounges and balloons of bourbon could also become multi-generational spaces used by the grandparents down to their grandchildren. We envisage these library spaces or co-working areas can be a place to catch up with your neighbour, sit in a nice quiet space by yourself or hold a book club.”

Residential property price growth in FY24 was strongest in the lower price brackets of every capital city except Darwin, data from CoreLogic has revealed. Meantime, the mid-tier capital cities of Perth, Brisbane and Adelaide continue to lead the nation in overall value growth. Many home buyers and investors are gravitating toward cheaper suburbs that offer greater affordability due to ongoing price rises and higher interest rates constraining borrowing capacity.

“After recording a higher rate of gain through the early months of the growth cycle, conditions have faded across the upper quartile as borrowing capacity reduced and affordability constraints deflected demand towards middle-and-lower-priced properties,” said CoreLogic research director, Tim Lawless.

Over the past three months, apartment prices have also risen faster than houses in every city bar Darwin and Canberra, indicating more home buyers are compromising on the type of property they buy.

“Most cities now have a median house value that is at least 1.5 times higher than the median unit value,” Mr Lawless said. “With stretched housing affordability, lower borrowing capacity and a lift in both investor and first home buyer activity, it’s not surprising to see the unit sector outperforming for a change.”

REA Group economic analyst Megan Lieu said affordability was “now a key drawcard for buyers”.

“Demand from buyers has been high in the past year due to a number of factors that include strong population growth, increased confidence in the market and scarce rental availability,” Ms Lieu said. “Prices are expected to keep rising in the coming months due to strong demand. However, as housing affordability declines, buyers will likely continue gravitating towards more affordable areas.”

Ms Lieu said REA analysed FY24 search data from its website, realestate.com.au, to identify the ‘affordable’ hot spot suburbs of each capital city. The analysis focused on suburbs with median house and apartment prices below their capital city’s medians, and identified the most popular suburbs based on search volumes.

Here are the results.

Sydney

Sydney’s median house price is $1,407,000. The three most popular affordable suburbs for houses were Blacktown (median $980,000), Campbelltown ($855,000) and Oran Park ($1,080,000).

Sydney’s median apartment price is $775,000. The three most searched affordable suburbs were Blacktown ($530,000), Ryde ($738,000) and Hornsby ($708,000).

Melbourne

Melbourne’s median house price is $870,000. The three most searched affordable suburbs were Frankston ($740,000), Sunbury ($660,000) and Craigieburn ($640,000).

Melbourne’s median apartment price is $605,000. The most popular affordable suburbs in FY24 were Melbourne CBD ($560,000), Richmond ($590,000) and Hawthorn ($584,000).

Brisbane

Brisbane’s median house price is $840,000. The most popular affordable suburbs were Redcliffe ($770,000), North Lakes ($809,000) and Narangba ($780,000).

Brisbane’s median unit value is $555,000. The most searched affordable suburbs were Nundah ($535,000), Wilston ($550,000) and Kedron ($535,000).

Adelaide

Adelaide’s median house value is $751,000. The most searched affordable suburbs were Mawson Lakes ($725,000), Modbury ($701,000) and Mount Barker ($661,500).

Adelaide’s median unit price is $501,000. The most popular affordable suburbs were Adelaide CBD ($479,000), West Beach ($495,000) and Mawson Lakes ($440,000).

Perth

Perth’s median house price is currently $680,000 and the median unit price is $450,000.

Perth’s median house price is $680,000. The most popular affordable suburbs were Baldivis ($611,000), Rockingham ($610,000) and Morley ($676,000).

Perth’s median unit price is $450,000. The affordable suburbs with the highest search volumes in FY24 were Wembley ($330,000), Mount Lawley ($430,000) and Yokine ($430,000).

Hobart

Hobart’s median house price is $700,000. The most popular affordable suburbs were Geilston Bay ($693,500), Moonah ($610,000) and Glenorchy ($558,000).

Hobart’s median apartment value is $531,000. The most searched affordable suburbs were New Town ($455,000), Glenorchy ($440,000) and Sorell ($507,000).

Darwin

Darwin’s median house price is $568,000. The most popular affordable suburbs in FY24 were Zuccoli ($530,000), Durack ($550,000) and Wulagi ($528,000).

Darwin’s median unit price is also $568,000. The most searched affordable suburbs were Darwin CBD ($440,000), Nightcliff ($382,000) and Fannie Bay ($502,000).

Canberra

Canberra’s median house price is $950,000. The most searched affordable suburbs for houses were Kambah ($850,000), Gungahlin ($900,000) and Casey ($815,000).

Canberra’s median unit price is $605,000. The most popular affordable suburbs were Braddon ($582,000), O’Connor ($531,000) and Lyneham ($520,000).

A Beverly Hills mega mansion that singer Mariah Carey once rented hit the market Monday asking $31.99 million.

The 15,000-square-foot residence, inspired by a mashup of European architectural styles from Baroque to Louis XV, is located on a 0.6-acre lot on Laurel Way. The three-story home includes eight bedrooms, and an entryway that features a 30-foot rotunda and not one, but two imposing double stairways, one outdoors and one indoors.

It was built by a Russian couple who immigrated in the 1970s, and set about building their dream home, much to their neighbours’ consternation . “I used all of what Europe has to offer,” Natalie Glosman, whose husband Leonid is a dentist, told Today.com in 2014.

The Glosmans purchased the land for $2.2 million in 1988 and sold the home in 2019 for $30 million. The buyer was a California entity, BHLW LLC, according to property records. The manager for the entity could not immediately be reached for comment.

Last year, Mariah Carey rented the house for three months in the spring, which was asking for $125,000 in monthly rent at the time. The Queen of Christmas then partnered with Booking.com, which offered visitors a special two-night “ritzy summer reprieve” at the house, with a Carey-curated itinerary, including reservations to her favourite restaurants, according to marketing material from the booking platform.

Mariah Carey rented the Beverly Hills home in a promotion for Booking.com. Photo by RB/Bauer-Griffin/GC Images

“One of my Lambs has the opportunity to experience L.A. in true Mimi fashion by staying in the same home and visiting all my favourite places in the area!” Carey said in the Booking.com news release at the time .

The house has some additional Hollywood elan, as it served as filming location on several occasions. Danny DeVito and one of the cast members of the “Real Housewives of Atlanta” have been filmed there, according to Today, and in the second season of “True Detective,” it stood in for the “incredibly gaudy” home of the corrupt and alcoholic mayor Austin Chessani, according to Curbed.

In addition to its grand entryway, the home features arched doorways, French windows, coffered ceilings, wainscotting and Rococo wall mouldings, in a blend of Art Deco and Art Nouveau styles. Outside, there is a broad green lawn with a shaded sitting area, and a back patio with a glamorous pool to match the home’s style.

Alla Furman and David Kramer of Hilton & Hyland/Forbes Global Properties are marketing the property. They were not immediately available for comment.

ByAehra, the company that calls itself “Italy’s first pure EV brand,” has two uncommonly attractive vehicles in the works, the Impeto SUV and the Estasi sedan. The designs were first shown in 2022 and 2023 , then unnamed. Pricing for both vehicles is expected to be in the vicinity of US$170,000.

Aehra has some private resources, but is also awaiting government funding. It has submitted a €1.2 billion (US$1.3 billion) development plan to Italy’s Ministry of Industry (controller of the country’s Automotive Fund) to underwrite construction of a 200,000-square-metre plant, which it plans to build at Mosciano Sant’Angelo, in the Abruzzo region of eastern Italy. Aehra says it will create 540 jobs in the region, and 110 more at its headquarters in Milan.

The Estasi with its doors open Courtesy of Aehra

Hazim Nada, Aehra’s U.S.-born but Italy-raised CEO and founder, tells Penta he expects the Automotive Fund to be capitalised with €2.5 billion next year.

“The government is quite enthusiastic about this project, and we don’t see anyone else with significant production plans,” he says, adding that automotive start-ups are thin on the ground “in Europe, not just in Italy.”

Nada says the company had originally planned to build its cars via an existing contract manufacturer such as Magna Steyr in Austria, but he says finding a plant that could handle the special carbon-fibre process Aehra plans to use proved difficult. “It’s been a busy year, focusing on the location for our assembly line,” he says. “I hope to move soon to working on consolidating our dealer network and sales process.”

The company likes Abruzzo because it’s not only the centre of Italy’s lightweight carbon-fibre industry, but also a hive of EV expertise at the University of L’Aquila. As its plans changed, Aehra has had to push back its start date. Nada says the company aims to be through the building-permit process by the end of the year or early 2025, then start construction of the plant—a 1.5- to two-year process.

A rendering of the Aehra Estasi interior. Courtesy of Aehra

Cars should start issuing from the plant in 2027, Nada says. The plan is to eventually scale up to 50,000 vehicles annually. He says Aehra does not intend to produce anything but battery EVs.

“Our focus is to build cars you can’t create with a thermal engine,” he says. “That’s our core. We couldn’t achieve the same results with hybrids.”

The designer of the cars was Filippo Perini, a veteran of Audi and Lamborghini. The cars are certainly beautiful, and closely related in their very streamlined designs. Nada says “the platforms are identical below the beltline.” The vehicles have frameless upward-opening doors (the company calls them Dihedral Facing Doors) that leave a large opening and ease entry and exit. The target is for them to have a very low coefficient of drag, 0.21, which means they should slip easily through the air.

Aehra’s modified styling for its Impeto SUV. Courtesy of Aehra.

The announced statistics are impressive, with a 500-mile range (close to certain versions of the Lucid Air) via 120-kilowatt-hour Miba Battery Systems packs and a top speed of around 165 miles per hour from the 800-horsepower powertrain. Zero to 62 miles per hour should take less than three seconds in the Estasi sedan, aided by a target curb weight of around 4,850 pounds (low for an EV with that size battery pack). A 10% to 80% fast charge should take 15 minutes.

Like the aforementioned Lucid, the Aehras are intended to be roomy inside. The SUV “will effortlessly accommodate four full-size National Basketball Association players while leaving room for a 6-foot adult in the middle of the rear-seat row,” the company says.

Aehra is targeting North America, Europe, and the Gulf States as markets for its cars. Nada thinks the Impeto SUV might have a sales edge.

“The SUV is easiest in the current market, but we expect to see some surprises with the sedan,” he says.

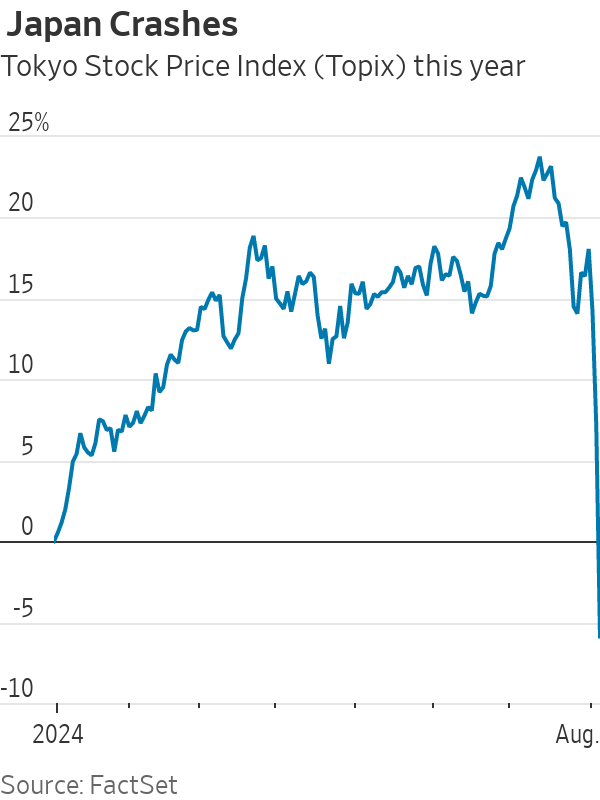

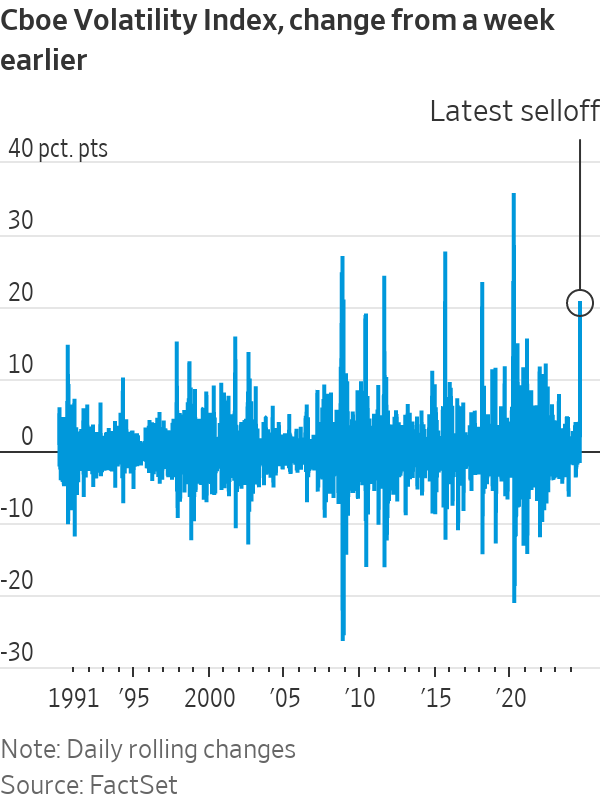

Financial markets are supposed to capture the wisdom of the crowd, but on Monday the crowd ran in all directions waving its hands in the air screaming. Japan’s stock market fell the most in 37 years with a 12% plunge that wiped out all its gains for the year, while in the U.S. the VIX index of implied stock volatility briefly had its biggest rise ever. Panic hit.

The selloff was triggered by Friday’s jobs data prompting a sudden switch in the economic narrative from soft landing to hard landing. Add to the mix a period of deflating hype about artificial intelligence and a Bank of Japan rate rise designed to strengthen the yen. News that Warren Buffett’s Berkshire Hathaway had sold half its Apple shares and boosted its cash pile added to the pain.

But the triggers couldn’t possibly justify the scale of the moves. When a new trigger arrived, in the form of better-than-expected data on the service sector, markets partially rebounded and the Vix fell sharply — again, far more than the data could justify.

The selloff—which at one point had chip maker Nvidia down 15%—was so big because investors had been all-in betting that things would work out well. Now things have calmed a bit, the question is whether the unwind of these bets, and the leverage behind them, is done. If it resumes, will the selloff feed back into higher savings and a weaker economy or, worse, hit the financial system?

The extreme examples of past effects from big market falls are 1987’s crash, 1998’s Long-Term Capital Management blowup and 2008’s global financial crisis. History is never perfect, but so far this looks more like a (much milder) version of 1987 than it does the other two.

In 1987, the stock market had its biggest one-day fall ever, with the S&P 500 down more than 20% on Black Monday in October. Investors had built up excessive leverage after a stunning 39% gain in the year to August’s high, and the crash led both to big margin calls and to badly designed automated trading that exacerbated the selling. But the Federal Reserve poured liquidity into the banks, brokers didn’t default and the market made back all its losses within two years. The economy was fine.

The good news was that 1987 was all about markets: They went up, they went back down, no one else was hurt. The S&P made 36% in the eight months to its August 1987 peak, similar to the 33% it rose in the eight months to the end of June this year. As in 1987, this year’s gains came in spite of tight monetary policy and higher bond yields. Just like today, in 1987 investors were on edge and ready to sell to lock in the unexpected profit. The losses are smaller so far, but lucrative trades have reversed , just as they did for the market as a whole in 1987.

In 1998, the situation was much worse, although stocks recovered more quickly. Highly levered hedge fund LTCM was crushed when Russia’s domestic debt default created a flight to safety. LTCM was big enough that it threatened to bring down Wall Street institutions. The Fed cut rates three times and pulled together a group of banks to rescue the firm and wind down its trades slowly. Stocks took just four months to recover, but the easy money helped stoke the dotcom bubble, which popped two years later and led to a mild recession—and gigantic losses for investors in tech stocks.

We don’t know yet if any hedge funds have been taken out by the big moves in markets, which have brought heavy losses for those engaged in the “ carry trade ” of borrowing cheaply in yen and buying higher-yielding currencies such as the Mexican peso or dollar. Large swings in Treasurys on Monday might also have hurt, given the large positions hedge funds hold. Traders are betting that the Fed will slash rates, with a super-sized cut of 0.5 percentage points priced into futures for the September meeting (and far more earlier in the day).

The really bad outcome would be a repeat of 2008, but it seems highly unlikely. True, some large U.S. banks failed last year, due to bad bets on government bonds. But banks are much less leveraged than they were, and the system is less exposed to a liquidity crisis, as private lenders have taken on much of the risk that used to sit in banks. Big losses are entirely possible, and private funds could hit trouble, but that would take time and wouldn’t create the same system-wide crisis.

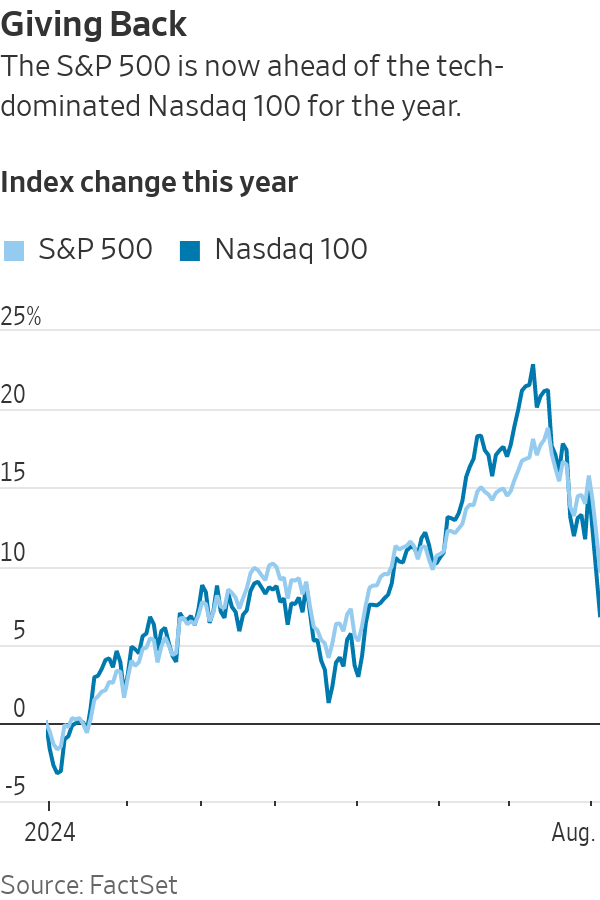

The ideal would be that excess in the stock market unwinds as in 1987 without creating wider trouble, hopefully more gradually than in 1987. AI enthusiasm could deflate stock prices much more—even after falling 30% from its June high, Nvidia has still doubled in price this year. But the market is already much closer to normal, with Monday’s falls leaving the Nasdaq 100 index up only 6% this year, and the S&P 7%.

If panic continues to abate, the Fed cuts and nothing breaks in the financial system, we should count ourselves lucky. But it would be good if investors could remember the sinking feeling they had on Monday morning, and try to be a bit wiser and less speculative.

Group travel has taken on new meaning for some wealthy consumers, who increasingly are taking over entire hotels.

In an experience-obsessed era, those who can are going beyond just a stay at a five-star hotel to having it all to themselves alongside family and friends. Luxury travel advisors report an uptick among their deep-pocketed clients who book accommodations in their entirety for both large and small groups.

Andrew Steinberg, an advisor with the Ovation Network in New York City, says that his buyout business is up 50% this year compared with 2023.

“From a dozen, I have more than double now. The prices for these weekend stays can start at US$500,000 and easily top US$1 million,” he says. “People love them because they can manage every aspect of the experience and extend their event.”

As an example, Steinberg planned a lavish 50th birthday last year in Versailles, France, for a client who took over Airelles Château de Versailles, Le Grande Controle, located on the grounds of Versailles, for a weekend. The extravaganza cost well into the seven figures, he says, and included elements such as a scavenger hunt on the palace grounds and a five-course dinner party prepared by the renowned chef Alain Ducasse, where guests donned 17th-century costumes provided by the host.

Entertainment included fire breathers and Cirque du Soleil-style dancers. Steinberg notes that guests also received a different gift each day such as silk scarves and pricey wines. “By having the property to ourselves, we were able to manage every touchpoint,” Steinberg says. “We had napkins for every meal with the host’s initial and amenities such as a personalised cookie station.”

Andrew Steinberg, an advisor with the Ovation Network in New York City, says that his buyout business is up 50% this year compared with 2023. Andrew Steinberg

Stacy Fischer-Rosenthal, the president of the New York-based Fischer Travel, which charges a US$150,000 membership fee, is also planning more buyouts than ever before for occasions such as weddings, birthdays, and “just because” get-togethers.

“Takeovers offer complete privacy, safety, and flexibility. The client does not have to adhere to a set schedule and can make theirs up as they go along,” Fischer-Rosenthal says. “There is a dedicated team catering to all of their wants and needs.”

The membership-based travel company Andrew Harper is another brand that has seen a jump in buyouts. Colin Housley, vice president of member experience, says the increase in demand led the company to launch an initiative called Exclusive Experiences, which focus on immersive and private trips such as luxury hotel buyouts and private island stays.

“Our members who plan these trips receive access to unique activities and excursions that we have negotiated with our partners,” Housley says. “We also leverage our relationships to make buyouts happen for properties that normally wouldn’t offer it.”

Andrew Harper has seen a “flood of requests” for private stays since Exclusive Experiences launched, he says.

Steinberg planned a lavish 50th birthday last year in Versailles, France, for a client. The extravaganza cost well into the seven figures, he says, Andrew Steinberg

Meanwhile, another New York-based travel company Black Tomato had a client who bought out Aman Venice to throw a US$1 million party for his wife’s 50th birthday.

“We arranged performances by opera singers, an orchestra, and a rock band, and the celebration ended with a treasure hunt on the rooftop of the Gritti Palace in the penthouse suite,” says Black Tomato travel expert Sunil Metcalfe , who also notes the uptick in such buyouts.

In addition to travel companies, representatives from several upscale hotels, including the Ranch at Rock Creek in Philipsburg, Mont., and Cal-a-Vie Health Spa in Vista, Calif., say that takeovers of their properties are on the rise. Many, particularly smaller hotels, offer buyout-specific packages.

Cali Mykonos, located on the namesake island’s Kalafati Beach, has created a package for a cost of between US$57,000 and US$75,000 that allows guests to book its 40 villas, each with a pool and large terrace, and enjoy amenities such as the large main pool, yoga classes, boat fleet, beach and restaurants exclusively with others in their group.

Sir Richard Branson ’s Necker Island in the British Virgin Islands has a buyout package starting at US$118,500 a night for 24 rooms that’s consistently booked throughout the year, according to a property representative. The rate includes meals and most activities, such as water skiing, snorkelling, and pickleball.

Weekapaug Inn, located in Westerly, R.I., introduced a buyout experience to commemorate its 125th anniversary this year. Called the Milestone Getaway, it encompasses the use of the hotel’s 33 rooms for two nights, meals and activities; the price is US$125,000.

Tom Parisi, an investment banker, and Adriana Destefanis, an asset manager, who live in Darien, Conn., bought out Weekapaug Inn for their wedding last October.

In addition to the wedding events, the couple’s more than 150 guests stayed busy by participating in diversions such as bike riding, birdwatching, stargazing, and s’mores by the fire pit.

“Having a private element is very unique in our view,” Parisi says. “We felt like we were in our own massive house and able to spend quality time with our family and friends. And we could be loud without worrying about other guests. We didn’t want to just have a wedding. We wanted an experience, and the buyout gave us that.”

In a widely predicted move, the Reserve Bank of Australia board decided to keep rates on hold at its meeting this afternoon.

In a statement, the board said the cash rate will remain at 4.35 percent, while the interest paid on exchnage settlement balances will also be unchanged at 4.25 percent.

The RBA noted that while inflation has fallen since its peak in 2022, the rate of inflation is still outside the board’s target range of between 2 and 3 percent.

“In underlying terms, as represented by the trimmed mean, the CPI rose by 3.9 percent over the year to the June quarter, broadly as forecast in the May Statement ob Monetary Policy,” the board said. “But the latest numbers also demonstrate that inflation is proving persistent.”

Noting that the economic outlook is uncertain and the road to a more manageable rate of inflation is slow and bumpy, the RBA board now predicts that the 2 to 3 percent rate is more likely to take at least another 12 months. The board has repeatedly stated its resolve to bring inflation to heel since it hit a high of 7.8 percent in December 2022.

“This represents a slightly slower return to market than forecast in May, based on estimates that the gap between aggregate demand and supply in the economy is larger than previously thought,” the board said. “In part, this reflects an increase in the forecast for domestic demand. But it also reflects a judgement that the economy’s capacity to meet that demand is somewhat weaker than previously thought, evidenced by the persistence of inflation and ongoing strength in the labour market.”

Research director at CoreLogic Asia Pacific, Tim Lawless, said the decision was unlikely to impact housing demand.

“Although a stable interest rate decision is seen as a positive for borrowers and housing more broadly, we aren’t expecting today’s outcome will have a material influence on housing trends,” Mr Lawless said. “While stable rates and lower inflation should help to lift consumer sentiment, which has historically shown a close relationship with property sales, the August hold decision may not be enough to see that rise in consumer sentiment flow through to housing market activity.

“Recent growth in property prices has had more to do with low supply, tight rental conditions and demographic factors than sentiment through the housing upswing to date.”

He pointed out that other factors, including ongoing problems with housing affordability and slowing migration were more likely influencing easing property prices.

“Even if sentiment lifts, an improvement in affordability barriers or strengthening in household balance sheets isn’t likely until interest rates start to fall,” he said.

The RBA board is expected to meeting again in six week’s time.

Christie’s is partnering with U.K.-based ocean protection charity Blue Marine Foundation to raise funds through a sale of works by leading contemporary artists during an October week of major London sales.

“Blue: Art for the Ocean” will include works from more than 20 artists, including Serbian performance artist Marina Abramović, Japanese painter Yoshitomo Nara, English artist Lydia Blakeley, English potter and author Edmund de Waal, and German painter Jonas Burgert.

Christie’s announced the first three pieces to be auctioned, including a photograph of Abramović from a May 2024 filming of a separate project that shows the artist on the shores of Fire Island, N.Y.

“My Performance for the Oceans artwork for the auction blends my artistic vision with environmental consciousness,” Abramović said in a news release. The image is one of three from the film that Christie’s will sell for between £50,000 and £70,000 (US$64,012 and US$89,617), according to Blue Marine, citing the Sunday Times of London.

The other two pieces are an underwater painting by Blakeley titled The Hunters and an illustration by Nara titled Walk On .

The foundation works toward ocean health by putting a spotlight on overfishing and efforts to protect critical marine ecosystems around the world.

Christie’s expects to announce a full lineup of lots and price estimates in the coming weeks, according to a company spokesperson. The auction will be held during Christie’s annual Frieze Week sales of 20th- and 21st-century art.

The red numbers in your 401(k) today might appear to vindicate warnings about an artificial-intelligence bubble and infirm economy. But don’t tilt your portfolio toward full pessimism just yet.

The S&P 500 was down 3% Monday, with the Nasdaq falling even further. Investors have been selling the year’s best performers, concerned that disappointing second-quarter results from big technology companies such as Alphabet , Tesla and Intel are a sign that the AI frenzy is a fad. Also, consumer discretionary stocks have become the worst-performing sector in the S&P 500, as lacklustre labour-market reports have raised worries that the Federal Reserve made a mistake by waiting until September to cut interest rates.

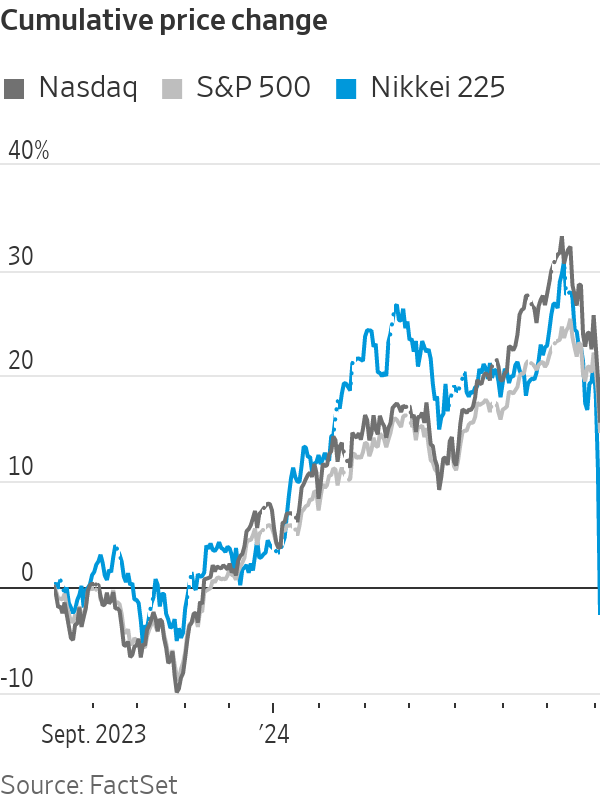

Overseas, the Stoxx Europe 600 closed almost 5% below where it was a week ago, whereas the Swiss franc, a common haven asset, is up roughly 4%. The most eye-popping moves happened in Asia, though, where the Nikkei 225 plunged 12.4% Monday in the worst trading session since Oct. 20, 1987—the day that followed Wall Street’s infamous Black Monday.

Yet it is precisely the breakneck speed with which Japanese equities tumbled that should give most investors a reason to remain calm.

As a guideline, sudden market selloffs are less dangerous than those that unfold progressively over time. This is because investors who rationally price in bad economic data often do so slowly, as it trickles in. Flash crashes, conversely, are often a sign that some tidbit of bad news made speculative bets go awry, triggering a cascade of trades, many of them automated.

Japan is particularly prone to such reversals because interest rates there are so low that many investors use them to fund higher-yielding investments in other currencies. Whenever markets get jittery, these “carry trades” tend to unravel, pushing up the yen and hitting Japanese stocks, many of which are diversified exporters that do better when global growth accelerates. Amplifying this tendency, Japanese stocks had this year become extremely popular among global investors.

The timing of the rout also points a finger at the Bank of Japan , which last week decided to tighten monetary policy for the first time in 17 years with the explicit goal of boosting the yen. Investors who rushed to cover their bets then triggered the reversal of stretched trades elsewhere, including in the U.S.

One of the most striking features of the S&P 500 for most of this year has been its extremely low volatility. Until July, the Cboe Volatility Index, or VIX, was at 2019 levels, and kept sliding lower even as investors made big changes to their monetary-policy forecasts.

While the VIX is often dubbed Wall Street’s “fear gauge,” the options contracts it is based on often themselves influence volatility. Whenever investors make bets against market swings, as they have recently in the U.S. by buying lots of structured products , the banks that sell those options are forced to take the other side. These hedges then suppress volatility in the stock market.

The flip side is that whenever a panic breaks through this feedback loop, volatility skyrockets. As the stock market opened Monday, the VIX hovered above 50, making it the highest weekly jump since the onset of the pandemic, though it later fell below 40.

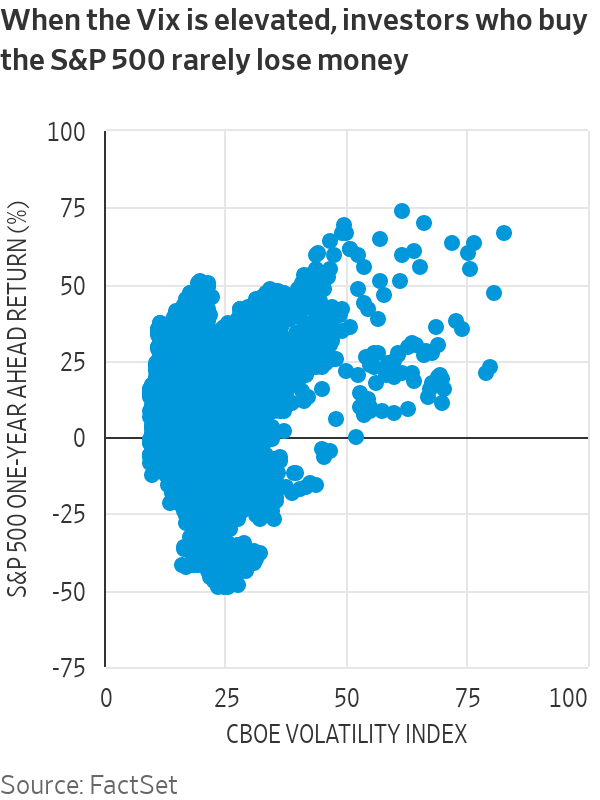

This suggests the selloff is disproportionate, especially looking at the historical record: 87% of the time, investors who bought the S&P 500 on days when the VIX closed at 30 or higher ended up making money a year later.

The second-quarter reporting season has brought mostly good news, with 78% of the S&P 500 firms that have reported so far beating analysts’ earnings estimates—compared with a 74% 10-year average. Both AI-related companies and the rest are reporting net income above what was forecast a month ago. Overall, the U.S. economy still looks robust: The unemployment rate has gone up because the labor force has expanded.

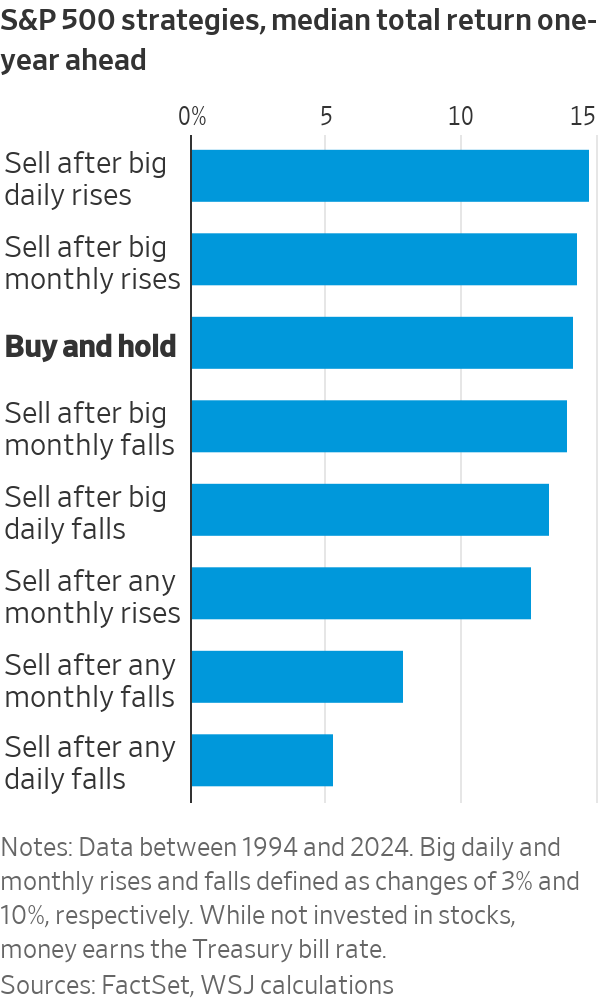

Also, looking at S&P 500 returns since 1994 shows that selling based on the previous day’s falls is a bad strategy. Electing to move into cash after large monthly declines fared better, but still less well than sitting tight.

This isn’t to say that concerns about an economic slowdown or high tech valuations aren’t warranted. Investors have reasons to diversify away from the AI trend or swap more cyclically exposed stocks for more “defensive” names. Indeed, selling out of stocks after particularly exuberant days and months has historically tended to be a winning move. But hindsight is a terrible guide to investing your savings.

Baby boomers make up just 21 percent of thepopulation but hold almost half of the nation’s private wealth, creating a ‘grandparent economy’. McCrindle Research said the trend indicated it would have a significant influence in today’s society and directly contribute to the financial wellbeing of younger generations.

The impact of baby boomer wealth is routinely seen in the property market, with boomers often observedat auctions standing side-by-side with their younger relatives as they bid for a potential new home. The Bank of Mum and Dad is likely a significant contributorto above-averagefirst-homebuyer activityin a market with rising values and interest ratesat their highest point in 13 years.

CoreLogic recently cited figures from the Australian Bureau of Statistics showing first home buyers comprise 28.7 percent of new owner-occupier finance, well above the decade average of 24.6 percent. One might assume that over the year to May 31,when the median national home value rose 8.3 percent and the official interest rate went another 0.5 percent higher, first home buyers’ budgets and borrowing capacity may have been squeezed. Instead, the value of their loansrose by 10.1 percent.

McCrindle says: “Baby Boomers … are having significant impacts in the economic landscape, showcasing their pivotal role in wealth transfers as they actively contribute to and shape the financial dynamics over the years ahead. Over the next two decades, we anticipate that $6.2 trillion of wealth will be transferred to younger generations. As a result, the grandparent economy is rising, facilitating wealth and contributing to the financial wellbeing of younger generations.”

In a survey published last year, McCrindle found grandparents were acutely aware of their younger relatives’ financial challenges. When asked about their greatest concerns for them, 77 percent cited the rising cost of living and 72 percent nominated the rising cost of buying a home. These concerns are influencing baby boomers’ own financial decisions, with 32 percent intending to pass on more than 50 percent of their wealth directly to their grandchildren.

A recent report published by Colonial First State found three in four Australiansplan to set aside a portionof their superannuation to pass on as an inheritance. Another survey by financial advisory company Findex found providing for relatives was a key motivator for 29 percent of investors.

McCrindle says: “As the current generation of grandparents continue to live longer and remain active well into their later years, their investments in properties and superannuation funds become pivotal components of the broader economic landscape.This trend signifies a notable shift in the traditional roles of grandparents, who are now not just recipients of support but active participants and contributors to the evolving economic dynamics, embodying the essence of the new investor in the financial landscape in the years to come.”

McCrindle Research shows two in five youngAustralians have receivedassistance from their grandparents. Most of that help is financial, including inheritances, living with them rent free, or paying cheap board, and getting help with everydaybills.

If there was a blueprint for how to do medium density housing in our major cities, Juliet Roseville could well be it. Located on Sydney’s Upper North Shore, close to some of the state’s most prestigious schools including Knox Grammar, Roseville College, Ravenswood Girls’ School and Pymble Ladies College, the residences are ideally positioned to encourage walking and public transport use while creating an enviable lifestyle of calm, comfort and relaxation.

Constructed above the reinvented Roseville Memorial Club — which itself is set to become a local architectural landmark — Juliet Roseville has been offered by award-winning, family owned developer Hyecorp which has been delivering homes in Sydney for more than 25 years.

With just 35 apartments over seven levels, the house-like spaces at Juliet provide the amenity traditionally associated with on-ground accommodation but with all the convenience of en plein air living. Light-filled interiors are complemented by spacious balconies which effectively double the available living space.

With one, two, three and four-bedroom apartments available, the boutique development is ideal for professional couples, families, downsizers and investors alike.

Central to Hyecorp’s interior design approach is the “Live Your Way” service, which allows prospective owners to customise their apartments to reflect their individual style. The bespoke service includes a studio appointment with an interior designer and the choice of two colour schemes for each apartment. For those with very discerning tastes, the bespoke upgrade packages offer buyers the chance to work with an interior designer to choose window coverings, lighting, underfloor bathroom heating and more.

Beyond the interiors, services at Juliet Roseville reflect the very best of contemporary living, with provision for everything from parcel lockers and dog washing bays to EV charging and car washing stations.

In keeping with its sustainability ethos, Juliet also enjoys an average NatHERS energy throughout the building.

While there is ample parking available, the site is conveniently placed near Roseville Village shops, just two minutes away, with Westfield Chatswood and The Concourse Chatswood less than 10 minutes down the road.

Families will enjoy the local parks and recreational facilities including Lane Cove National Park, Roseville Golf Club and Roseville Park Tennis Courts, while three of the city’s best hospitals are less than 20 minutes away.

From the sparkling new amenities to the well-serviced leafy surrounds, it’s hard to think of a better place to start your new life.