China’s Housing Market Woes Deepen Despite Stimulus

Home prices declined at a faster pace in May in major cities, while other data show a mixed picture for the world’s second-largest economy

4 min

4 min

China’s broken housing market isn’t responding to some of the country’s boldest stimulus measures to date—at least not yet.

The Chinese government has been stepping up support for housing and other industries in recent months as it tries to revitalise an economy that has continued to disappoint since the early days of the pandemic.

But fresh data for May showed that businesses and consumers remain cautious. Home prices continue to fall at an accelerating rate, and fixed-asset investment and industrial production, while growing, lost some momentum.

“China’s May economic data suggest that policymakers have a lot to do to sustain the fragile recovery,” Yao Wei, chief China economist at Société Générale, wrote in a client note on Monday.

The worst pain is in the property sector, which has been struggling to deal with oversupply and weak buyer sentiment since 2021, when a multiyear housing boom ended . The market still doesn’t appear to have found a floor, even after Beijing rolled out its most aggressive stimulus measures so far in mid-May in hopes of restoring confidence.

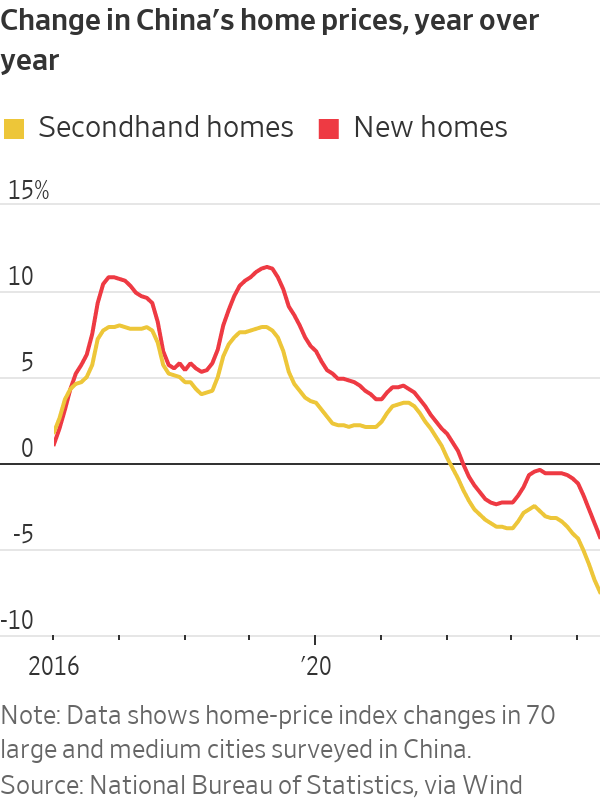

In major cities, new-home prices fell 4.3% in May compared with a year earlier, worse than a 3.5% decline in April, according to data released Monday by China’s National Bureau of Statistics. Prices in China’s secondhand home market tumbled 7.5%, compared with a 6.8% drop in April.

Home sales by value tumbled 30.5% in the first five months of this year compared with the same months last year.

“This data was certainly on the disappointing side and may ring some alarm bells, as May’s policy support package has not yet translated to a slower decline of housing prices, let alone a stabilisation,” said Lynn Song, chief China economist at ING.

Economists had also been hoping to see a wider recovery this month after Beijing started rolling out a planned issuance of 1 trillion yuan, the equivalent of $138 billion, in ultra-long sovereign bonds in May. The funds are designed to help pay for infrastructure and property projects backed by the authorities. Investors gobbled up the first batch of these bonds.

Monday’s bundle of economic data, however, underlined how the country still isn’t firing on all cylinders.

Retail sales, a key metric of consumer spending, rose 3.7% in May from a year earlier, compared with 2.3% in April, according to the National Bureau of Statistics. While the trend is heading in the right direction, it is still a relatively subdued level of growth, and below what most economists believe is needed to kick-start a major revival in consumer spending.

The expansion in industrial production—5.6% in May compared with a year earlier—was down from April’s 6.7% increase. Fixed-asset investment growth, of which 40% came from property and infrastructure sectors, also decelerated, to 3.5% year-over-year growth in May from 3.6% in April.

Key to the sluggish economic activity data in May—and China’s outlook going forward—is the crisis in the property market, which has proven hard for policymakers to address.

The property rescue package in May included letting local governments buy up unsold homes, removing minimum interest rates on mortgages, and reducing payments for potential home buyers. It also included as its centrepiece a $41 billion so-called re-lending program launched by the People’s Bank of China, which would provide funding to Chinese banks to support home purchases by state-owned firms.

The hope was that by stepping in as a buyer of last resort for millions of properties, the government would manage to mop up unsold housing inventory and persuade wary home buyers to re-enter the market. In turn, Chinese consumers, who have most of their wealth tied up in real estate, would feel more confident about spending again, thereby lifting the overall economy.

But the size of the re-lending program wasn’t big enough to convince home buyers, said Larry Hu , chief China economist at Macquarie Group. “Meanwhile, their income outlook also stays weak given the current economic condition,” he said.

For the property market to bottom out and reach a new equilibrium, mortgage rates, which stand at around 3-4% in China, need to be as low as rental yields, which are currently below 2% in major cities, said Zhaopeng Xing, a senior China strategist at ANZ. He said that a large mortgage rate cut will need to happen eventually.

The other key part of China’s push to revive growth revolves around the manufacturing sector, with leaders funnelling more investment into factories to boost output and reduce the country’s reliance on foreign suppliers of key technologies.

The result has been a surge in production. But with domestic consumption not strong enough to absorb all those goods, many factories have been forced to cut prices and seek out more overseas buyers.

Data released earlier this month showed that Chinese exports rose faster in May than the month before.

However, the export push is butting into resistance as governments around the world worry about the impact of cheap Chinese competition on domestic jobs and industries. The European Union last week said it would impose new import tariffs on Chinese electric vehicles, describing China’s auto industry as heavily subsidised by the government, to the point where other countries’ automakers can’t fairly compete.

The U.S. has also hit Chinese cars and some other products with hefty duties, while countries including Brazil, India and Turkey have opened antidumping investigations into Chinese steel, chemicals and other goods.

Beijing says such moves are protectionist and that its industries compete fairly with global rivals.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

Australia’s housing affordability crisis is being fuelled by chronic undersupply, planning delays and rising development costs, as politicians continue to focus on the wrong solutions.

3 min

Australia’s housing crisis will not be solved by first-home buyer incentives or tax changes alone, with leading property figures warning governments must tackle supply constraints if affordability is to improve.

Speaking at the Kanebridge Quarterly Property Leadership Summit in Sydney last week, expert project marketing specialist Sam Elbanna, property investor and fund manager Paul Miron and property consultant Karla McNeice said that a lack of housing supply remained the central issue facing the market.

Elbanna, Director of CPM Realty with more than 30 years’ experience in project sales, argued that successive governments had focused too heavily on stimulating demand rather than addressing the barriers preventing new housing from being delivered.

“The misconception is that politicians think the way to solve the housing crisis is to drive demand,” he said.

“The reality is that’s not the way. This is a supply-side problem, and it needs to be solved on the supply side.”

Drawing on his experience in project sales, Elbanna said policies designed to help first-home buyers often had unintended consequences, pointing to previous grants that ultimately flowed through to higher property prices.

Instead, he said developers were facing increasing red tape, approval delays and rising costs, which were discouraging new housing supply.

“In the absence of stock, demand exceeds supply,” he said.

Miron, a Co-Founder and Fund Manager of Msquared Capital, said the housing debate had become overly focused on tax policy while overlooking broader structural issues.

He argued that affordability challenges stemmed from a combination of factors, including planning constraints, supply shortages, migration levels and interest rates.

“No-one can be 100 per cent certain on the real reason for property prices is going up,” he said.

“The reason why property prices are higher is a combination of interest rates, lack of supply, migration, vacancy rates and maybe taxes play a role.”

Miron was critical of recent federal housing policy changes, warning they could reduce the number of new homes being built and further constrain supply that was even highlighted in the budget.

He also highlighted the importance of the property sector to the broader economy, noting that residential real estate and related industries employed more than one million Australians.

McNeice, who advises developers on sales strategy and market intelligence, said understanding buyers had become increasingly important as affordability pressures intensified.

While affordability remained a major consideration, she said today’s buyers were focused on value rather than simply price.

“People are looking for value for money,” she said.

She said buyers were increasingly evaluating factors such as transport connections, walkability, nearby amenities and flexible living spaces that could accommodate changing family needs.

“What infrastructure is going on? Can I walk to the shops? Can I meet people at the local cafe?” she said.

The panel also discussed the mounting pressures facing developers, with Elbanna arguing that many projects become financially unviable from the moment a site is purchased.

“The viability of a development happens at the moment the site is bought,” he said.

He said rising construction costs, higher interest rates and overly optimistic feasibility assumptions had left some developers exposed as market conditions changed.

While acknowledging the growing number of smaller and first-time developers entering the market, Elbanna said property development required expertise across finance, construction, marketing and legal disciplines.

“It is actually a business that requires a level of expertise,” he said.

Looking ahead, the panel agreed opportunities remained in the market despite current challenges.

Miron said property should continue to be viewed as a long-term investment and cautioned against trying to time short-term market movements.

McNeice said success would increasingly depend on identifying projects that genuinely met changing buyer expectations.

Elbanna said affordable housing remained achievable, but developers needed to deliver more than just homes.

“We can provide affordable housing in this country,” he said.

“But we’ve got to wrap that affordable housing with the things that people want.”

As Australia’s housing affordability debate intensifies, the panellists agreed on one point: without a meaningful increase in housing supply, demand-side measures alone are unlikely to solve the nation’s property challenges.

Three-Michelin-starred chef Massimiliano Alajmo will host an intimate Mediterranean sailing aboard Crystal Serenity, redefining fine dining at sea.

Rugged coastal drives and fireside drams define a slow, indulgent journey through Scotland’s far north.