Australia experiencing the worst year for home building since 2011

Data from the ABS paints a grim picture for the national target to build 1.2 million new homes

2 min

2 min

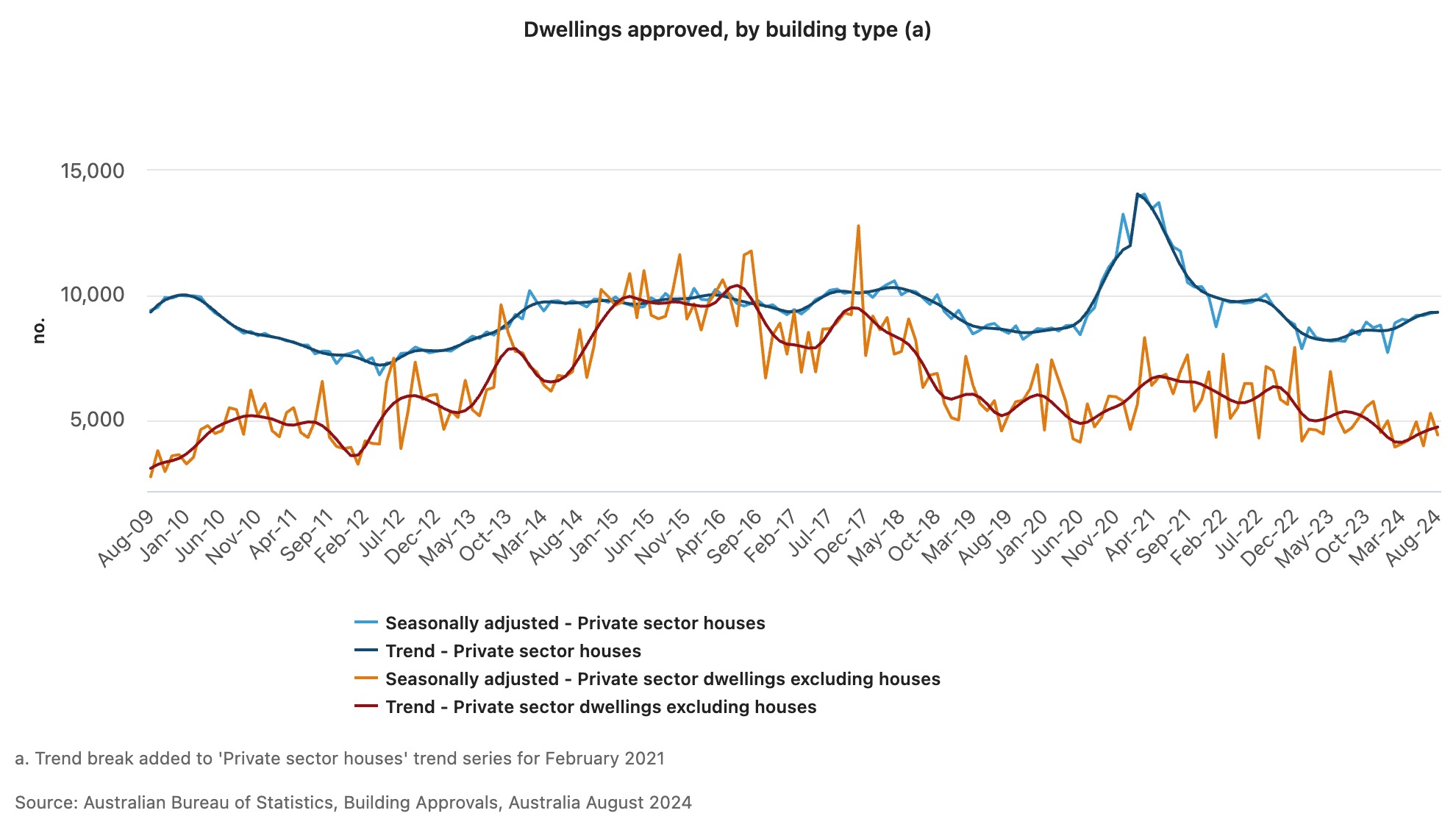

Building approvals fell again in August, as the Federal Government’s pledge of providing 1.2 million new homes looks more out of reach than ever.

The Australian Bureau of Statistics released data today showing total dwelling approvals fell by 6.1 percent in August to 13,991. While approval for houses rose 0.5 percent, the non house sector — apartments and townhouses — experienced a massive fall of 16.5 percent to 4,418.

Master Builders Australia reported that the latest decline in approvals contributed to 2023-2024 being the worst year for home building in more than a decade.

“Detached house starts fell by 10.1 percent, while higher density commencements were down by 6.0 per cent,” said Master Builders Chief Economist Shane Garrett. “If building continues at this pace, we’ll be in for less than 800,000 new home starts over the next five years.

“This would mean a shortfall of over 400,000 homes compared with the National Housing Accord target.”

Master Builders Australia CEO Denita Wawn said the data comes on the back of figures from the National Centre for Vocational Education Research which showed an alarming shortfall in the number of apprentices entering the industry and then completing their qualifications. Apprenticeship commencements fell 11.8 percent in the year to March 2023 while completion rates fell 8.6 percent over the same period.

“Today’s data releases aren’t unrelated,” Ms Wawn said. “To bring Australia out of the housing crisis we need to drastically increase the supply of housing and we can’t do that while we’re simultaneously suffering through a labour shortage.”

She said construction was experiencing a shortage of skilled workers across all trades.

“Until we’re able to address the challenges facing the future of the workforce, we won’t be able to increase building activity and reduce the impact of supply conditions in the residential building market on Australia’s inflation problem,” she said.

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

Australia’s housing affordability crisis is being fuelled by chronic undersupply, planning delays and rising development costs, as politicians continue to focus on the wrong solutions.

3 min

Australia’s housing crisis will not be solved by first-home buyer incentives or tax changes alone, with leading property figures warning governments must tackle supply constraints if affordability is to improve.

Speaking at the Kanebridge Quarterly Property Leadership Summit in Sydney last week, expert project marketing specialist Sam Elbanna, property investor and fund manager Paul Miron and property consultant Karla McNeice said that a lack of housing supply remained the central issue facing the market.

Elbanna, Director of CPM Realty with more than 30 years’ experience in project sales, argued that successive governments had focused too heavily on stimulating demand rather than addressing the barriers preventing new housing from being delivered.

“The misconception is that politicians think the way to solve the housing crisis is to drive demand,” he said.

“The reality is that’s not the way. This is a supply-side problem, and it needs to be solved on the supply side.”

Drawing on his experience in project sales, Elbanna said policies designed to help first-home buyers often had unintended consequences, pointing to previous grants that ultimately flowed through to higher property prices.

Instead, he said developers were facing increasing red tape, approval delays and rising costs, which were discouraging new housing supply.

“In the absence of stock, demand exceeds supply,” he said.

Miron, a Co-Founder and Fund Manager of Msquared Capital, said the housing debate had become overly focused on tax policy while overlooking broader structural issues.

He argued that affordability challenges stemmed from a combination of factors, including planning constraints, supply shortages, migration levels and interest rates.

“No-one can be 100 per cent certain on the real reason for property prices is going up,” he said.

“The reason why property prices are higher is a combination of interest rates, lack of supply, migration, vacancy rates and maybe taxes play a role.”

Miron was critical of recent federal housing policy changes, warning they could reduce the number of new homes being built and further constrain supply that was even highlighted in the budget.

He also highlighted the importance of the property sector to the broader economy, noting that residential real estate and related industries employed more than one million Australians.

McNeice, who advises developers on sales strategy and market intelligence, said understanding buyers had become increasingly important as affordability pressures intensified.

While affordability remained a major consideration, she said today’s buyers were focused on value rather than simply price.

“People are looking for value for money,” she said.

She said buyers were increasingly evaluating factors such as transport connections, walkability, nearby amenities and flexible living spaces that could accommodate changing family needs.

“What infrastructure is going on? Can I walk to the shops? Can I meet people at the local cafe?” she said.

The panel also discussed the mounting pressures facing developers, with Elbanna arguing that many projects become financially unviable from the moment a site is purchased.

“The viability of a development happens at the moment the site is bought,” he said.

He said rising construction costs, higher interest rates and overly optimistic feasibility assumptions had left some developers exposed as market conditions changed.

While acknowledging the growing number of smaller and first-time developers entering the market, Elbanna said property development required expertise across finance, construction, marketing and legal disciplines.

“It is actually a business that requires a level of expertise,” he said.

Looking ahead, the panel agreed opportunities remained in the market despite current challenges.

Miron said property should continue to be viewed as a long-term investment and cautioned against trying to time short-term market movements.

McNeice said success would increasingly depend on identifying projects that genuinely met changing buyer expectations.

Elbanna said affordable housing remained achievable, but developers needed to deliver more than just homes.

“We can provide affordable housing in this country,” he said.

“But we’ve got to wrap that affordable housing with the things that people want.”

As Australia’s housing affordability debate intensifies, the panellists agreed on one point: without a meaningful increase in housing supply, demand-side measures alone are unlikely to solve the nation’s property challenges.

A Vaucluse masterpiece by MHNDU with interiors by Poco Designs brings architectural ambition and breathtaking ocean outlook to the auction block.

Rising rates, construction inflation and shrinking investor confidence are pushing Australia deeper into a dangerous housing spiral that monetary policy alone cannot fix.