MELBOURNE HOUSING POISED FOR CYCLICAL RECOVERY IN 2025–26

Lower interest rates, firm population growth and tight supply set the stage for a late-2025 upturn, though Melbourne’s price discount to other capitals is likely to persist, according to new research.

2 min

2 min

Melbourne’s residential market appears to be on a comeback path, with a pricing recovery expected to take shape from late 2025 and continue through 2026 as borrowing costs ease and demand holds up.

New research by the MaxCap Group, commercial real estate fund manager, argues that lower mortgage rates will be the key catalyst for the next upswing, with stabilising sentiment and gradually improving activity reinforcing the turn.

The city has underperformed since 2022. While Brisbane, Perth and Adelaide posted strong gains, Melbourne recorded a modest correction.

One effect has been a lift in relative affordability. Local prices now sit below a wide set of comparable markets, including Brisbane, the Gold Coast, the Sunshine Coast, Canberra and Adelaide, and could trail Perth by year end.

That discount is expected to endure even as prices rise, reflecting differences in tax settings, investor participation and recent growth momentum elsewhere.

Several cyclical and structural forces are in play. Higher interest rates and softer sentiment have been a clear headwind over the past two years.

A heavier state tax take as Victoria pursues budget repair has also weighed on investor activity. Property-related imposts such as land transfer duty and land tax are taking a larger share of state revenues in 2025–26, and that has cooled appetite at the margin.

Set against those drags are supportive fundamentals. Population growth remains robust, interstate outflows are easing, and the construction pipeline is constrained.

The research estimates an 8,000-dwelling shortfall in Victoria in 2025, with the shortage most acute in the city of Melbourne. Rental markets remain tight, with a residential vacancy rate of 1.8 per cent in August pointing to ongoing pressure on rents and a continued incentive to build.

At a sub-market level, undersupply is most evident across the inner and middle rings and through the south-east corridor. There are early signs of price stabilisation, with more than half of the most-traded suburbs shifting from annual declines to annual growth.

The initial gains are concentrated in more affordable fringe areas, where price points and borrowing capacity are best aligned as rates begin to fall.

Looking ahead, model-based projections indicate prices should lift as mortgage rates decline, incomes rise and building activity gradually recovers. The upgrade cycle is expected to be measured rather than explosive.

Without near-term reform to property taxes, the recovery is likely to be more subdued than previous Melbourne upswings, and the city’s price discount to other capitals is expected to persist through this cycle.

The research also contrasts Melbourne’s broader post-pandemic performance with other markets, noting a deeper peak-to-trough decline in CBD office values than Sydney.

Even so, the residential turnaround is framed as primarily a function of the interest rate cycle rather than policy shifts. Risks to the outlook include a slower-than-expected pace of rate cuts, construction cost pressures that delay supply, and any renewed deterioration in investor sentiment.

For buyers, the combination of improved affordability, tightening rental conditions and the prospect of lower rates suggests a narrowing window before momentum rebuilds. For sellers, the message is that late 2025 into 2026 should deliver firmer conditions, especially in well-located, appropriately priced stock across the inner and middle rings where undersupply is most pronounced.

The 1860s Darlinghurst mansion Stoneleigh could become Sydney’s most expensive home ever sold under the hammer when it goes to auction. Clint Ballard is giving buyers a $28 million guide for the heritage-listed mansion on Darley Street, opposite Iona, the former home of Hollywood royalty Baz Luhrmann. Stoneleigh is being offered for sale for the …

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

3 min

3 min

The 1860s Darlinghurst mansion Stoneleigh could become Sydney’s most expensive home ever sold under the hammer when it goes to auction.

Clint Ballard is giving buyers a $28 million guide for the heritage-listed mansion on Darley Street, opposite Iona, the former home of Hollywood royalty Baz Luhrmann.

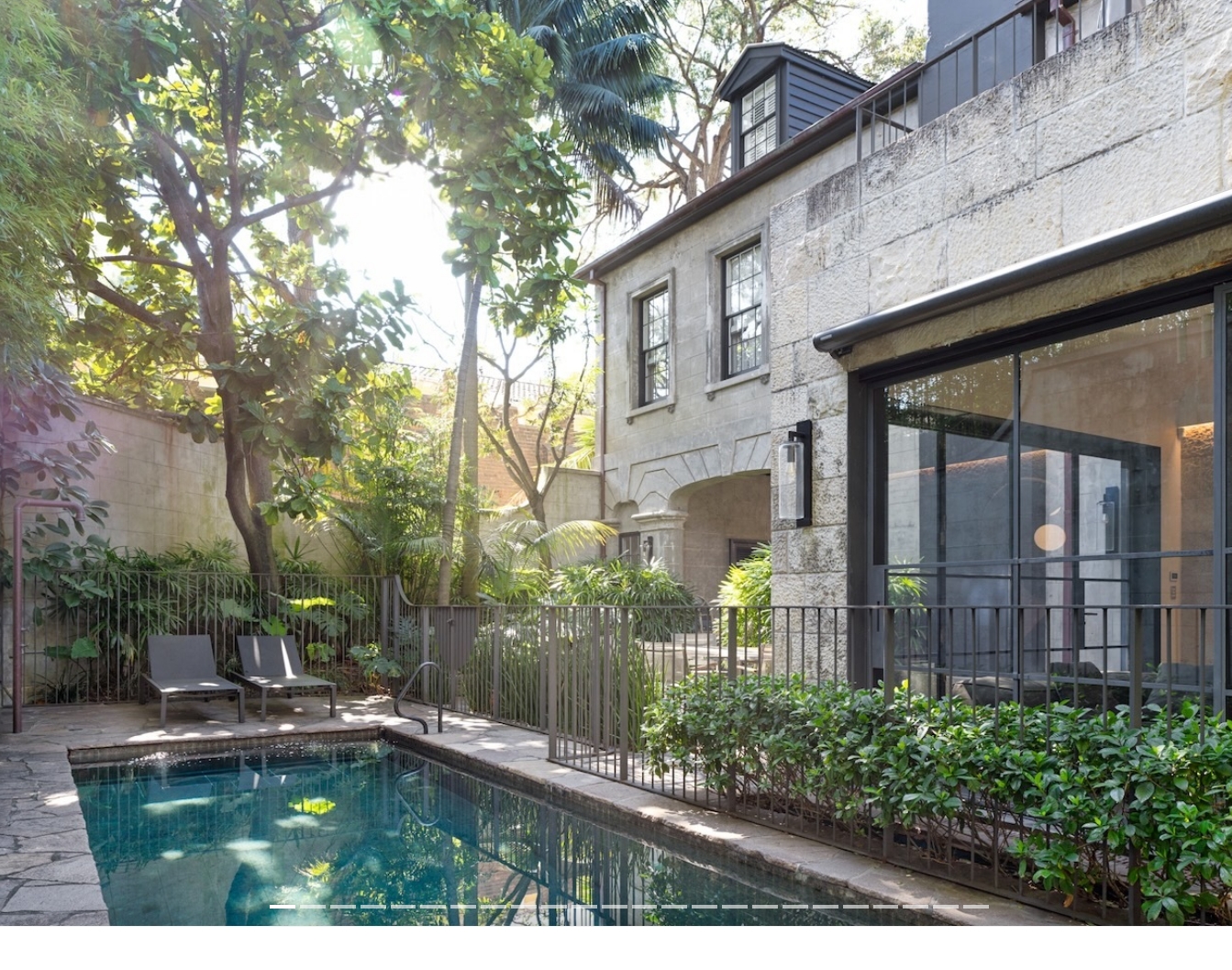

Stoneleigh is being offered for sale for the first time in 36 years. The home is owned by jeweller Vanessa Wong, who took the keys in 2016, after the Wong family paid $3.18 million in 1990. Wong renovated the home shortly after taking ownership, adding a pool to its 650 sqm grounds.

A Landmark on the Heritage Register

‘Stoneleigh’ is recognised on the NSW State Heritage Register for its architectural elegance and historical significance, and remains a defining presence within the tightly held Darlinghurst Ridge heritage precinct, an enclave prized for its concentration of intact colonial and Victorian-era residences just minutes from the CBD.

While the bones of the home date to 1860, its current form reflects a considered architectural transformation by Brian Hess, with landscaping by Dangar Barin Smith, that reconciles the villa’s historic fabric with the demands of contemporary living.

Stoneleigh was added to the State Heritage Register in 1999. It features a hipped corrugated steel roof, a bank of 12 paned timber framed double hung windows to the first floor, and arched colonnade to the ground floor, all set behind a Victorian cast iron palisade fence and colonnade extends around one side of the building.

Two of its previous owners have included Richard Jones, who was Chairman of the Commercial Banking Company of Sydney and the founder of the Maitland Mercury newspaper. He owned the home for around two decades from 1870. From the mid-1890s, J. Russell French, who was General Manager of the Bank of New South Wales, had the keys.

Grand Interiors, Resort-Style Grounds

Inside, the home unfolds across multiple levels, anchored by a statement marble kitchen with integrated dining that flows into expansive formal and informal living zones. These spaces open out to a private terrace and tropical gardens, blurring the line between indoor and outdoor living in a way that’s become the calling card of Sydney’s top-tier renovations.

The outdoor offering is a standout in its own right: a 3-metre-deep mineral pool with geothermal heating anchors a resort-style entertaining garden designed for year-round use, an increasingly sought-after feature among buyers at the top of the market.

Accommodation is generous with six bedrooms in total. There are two master suites, including a primary retreat built around a Japanese Hinoki bath, along with additional bedrooms, terraces and substantial storage, a rare inclusion in an inner-city heritage home of this era.

Finishes throughout run to French Oak flooring, hand-applied Marrakech plaster walls, bespoke lighting by Michael Anastassiades and a Stuv fireplace, all supported by advanced geothermal climate control, ducted air conditioning and a full security system. A cellar on the lower ground floor houses a functioning heritage well, a genuinely rare survivor that underscores just how much of the property’s 19th-century character has been preserved.

Perhaps most notably for an inner-city heritage property, ‘Stoneleigh’ offers secure parking for up to five vehicles, a feature agents will no doubt lean on heavily, given how scarce multi-car garaging is within walking distance of the city.

Key Features

- Architecturally redesigned by Brian Hess with landscaping by Dangar Barin Smith

- Landmark c.1860 Victorian Regency residence with a refined contemporary transformation

- Resort-style outdoor living with mineral pool, geothermal heating and tropical gardens

- Designer marble kitchen with integrated dining and Sub-Zero, Wolf and Miele appliances

- Multiple formal and informal living zones flowing to an outdoor entertaining terrace

- Two master suites, including a primary retreat with a Japanese Hinoki bath, plus additional bedrooms

- French Oak flooring, Marrakech plaster finishes and bespoke lighting throughout

- Advanced geothermal heating/cooling, ducted air conditioning and full security system

- Stuv fireplace, Michael Anastassiades lighting, retractable awnings

- Secure parking for up to five vehicles — a rare inner-city offering

- Level walk to fine dining, bars, cafes and train stations; 2km to the CBD

- Moments from some of Sydney’s finest schools, including Ascham, SCEGGS and Sydney Grammar

A New Record?

The highest price ever paid for a residential house sold under the hammer in Sydney is $24.6 million, for a home in Vaucluse in September 2020.

Bidding opened at $13 million for the 1,085-square-metre block against an $11 million price guide, and the hammer fell at $24.6 million — well above the $14 million reserve. A young Australian-Chinese couple who’d never bid at auction before walkedaway with the keys. That result broke the previous auction record of $23 million, set by media scion Lachlan Murdoch’s purchase of the Bellevue Hill mansion “Le Manoir” in 2009.

Late last year, Iona, across the road from Stoneleigh, sold by private treaty for $37.5 million. It was bought by Bryant Stokes, son of the billionaire Channel 7 chairman Kerry Stokes, and his wife Dominique. It was sold by investment banker Tim Eustace and his partner Salvador Panui, who bought it from film director Baz Luhrmann for $16 million in 2015.

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

Formula 1 may be the world’s most glamorous sport, but for Oscar Piastri, it’s also one of the most lucrative. At just 24, Australia’s highest-paid athlete is earning more than US$40 million a year.