Why First-Home Buyer Schemes Are Becoming a Stealth Investment Strategy

First-home incentives can still form part of a long-term investment plan if used strategically.

3 min

3 min

Australia’s home prices continue to grow, and while that makes them great investments, they are also some of the most unaffordable in the world.

That’s why first-home buyer schemes such as the First Home Owner Grant, the First Home Guarantee, and stamp duty concessions have become so valuable.

These programs are designed to reduce upfront costs and fast-track people into homeownership.

But the question many aspiring investors are now asking is can these schemes be used as part of an investment strategy? These government initiatives aren’t designed for investors, but they can still play a key role in your long-term investment journey if used strategically.

What the schemes actually allow

Every first-home buyer incentive in Australia is created to support owner-occupiers, not investors.

Whether it’s a cash grant, reduced deposit requirement, or a stamp duty discount, the catch is always the same in that you must live in the property for a set period of time. For example, the First Home Owner Grant often requires you to live in the property for at least six to twelve months, depending on the state.

The First Home Guarantee allows you to purchase with just a 5 per cent deposit without paying lenders’ mortgage insurance, but again, you’re required to live in the property for at least one year.

Likewise, state-based stamp duty concessions are only available for properties intended as a principal place of residence. If your intention from the outset is to buy a property solely for rental income, you won’t be eligible. However, if you’re open to living in the property initially, then transitioning it into an investment, there’s a path forward.

A strategy that works

Rentvesting has emerged as one of the most practical ways for first-time buyers to take advantage of these schemes while also laying the groundwork for a property portfolio.

The concept is simply, buying a property in an area you can afford (using the first-home buyer schemes to assist), live in it for the minimum required period, and then rent it out after fulfilling the occupancy condition.

This approach lets you legally access the benefits of first-home buyer schemes while building equity and entering the market sooner. Instead of waiting years to save a full 20 per cent deposit for an investment property, or getting priced out altogether, you get your foot in the door with reduced upfront costs.

Once you’ve satisfied the live-in requirement, the property can become an income-generating asset and even serve as collateral for your next purchase.

What to look for in a rentvestment property

If you plan to eventually convert the property into an investment, you need to think beyond your short-term living experience. It’s essential to buy a property that performs well both as a home and as a long-term asset.

That means looking at key fundamentals like location, rental demand, and growth potential. Suburbs with strong infrastructure, access to employment hubs, good transport links, and low vacancy rates should be high on your list.

A balanced price-to-rent ratio will help ensure manageable holding costs once the property transitions to an investment.

Established low-density areas often outperform high-rise apartment developments that flood the market with supply and limit capital growth. And ideally, your property should offer scope for future improvements, whether that’s a cosmetic renovation, granny flat addition, or potential to subdivide down the track.

Mistakes to avoid

There are a few common missteps that can undermine this strategy. The first is selling too soon. Some grants and stamp duty concessions include clawback provisions if you offload the property within a short period, which could see you lose the benefits or even owe money back.

It’s also a mistake to let the lure of a government handout sway your purchasing decision. A $10,000 grant doesn’t justify compromising on location, growth prospects, or property fundamentals.

Another pitfall is failing to consider the financial impact once the property becomes an investment. Repayments, tax treatment, and outgoings may change, so it’s important to stress-test your position from day one.

Lastly, beware of buying into oversupplied areas simply because they’re marketed to first-home buyers. Not all new builds are good investments. If hundreds of identical properties are being built nearby, your long-term growth could be seriously limited.

With the right approach, your first home can be the foundation for an entire property portfolio. It starts with using available government support to lower your entry cost.

From there, you occupy the property for the required time, convert it to an investment, and leverage the equity and rental income to fund your next purchase.

Many of the most successful investors today began with a single, strategically chosen property purchased using these exact schemes. By buying well, you can turn your first home into the launchpad for long-term wealth.

Abdullah Nouh is the Founder of Mecca Property Group (MPG), a buyers’ advisory firm specialising in investment opportunities in residential and commercial real estate. In recent years, his team has acquired over $300 million worth of assets for 250+ clients across Australia.

The 1860s Darlinghurst mansion Stoneleigh could become Sydney’s most expensive home ever sold under the hammer when it goes to auction. Clint Ballard is giving buyers a $28 million guide for the heritage-listed mansion on Darley Street, opposite Iona, the former home of Hollywood royalty Baz Luhrmann. Stoneleigh is being offered for sale for the …

Set on one of the city’s last absolute riverfront sites, The Riversdale by Mosaic combines irreplaceable waterfront ownership with one of Brisbane’s most significant residential opportunities.

3 min

3 min

The 1860s Darlinghurst mansion Stoneleigh could become Sydney’s most expensive home ever sold under the hammer when it goes to auction.

Clint Ballard is giving buyers a $28 million guide for the heritage-listed mansion on Darley Street, opposite Iona, the former home of Hollywood royalty Baz Luhrmann.

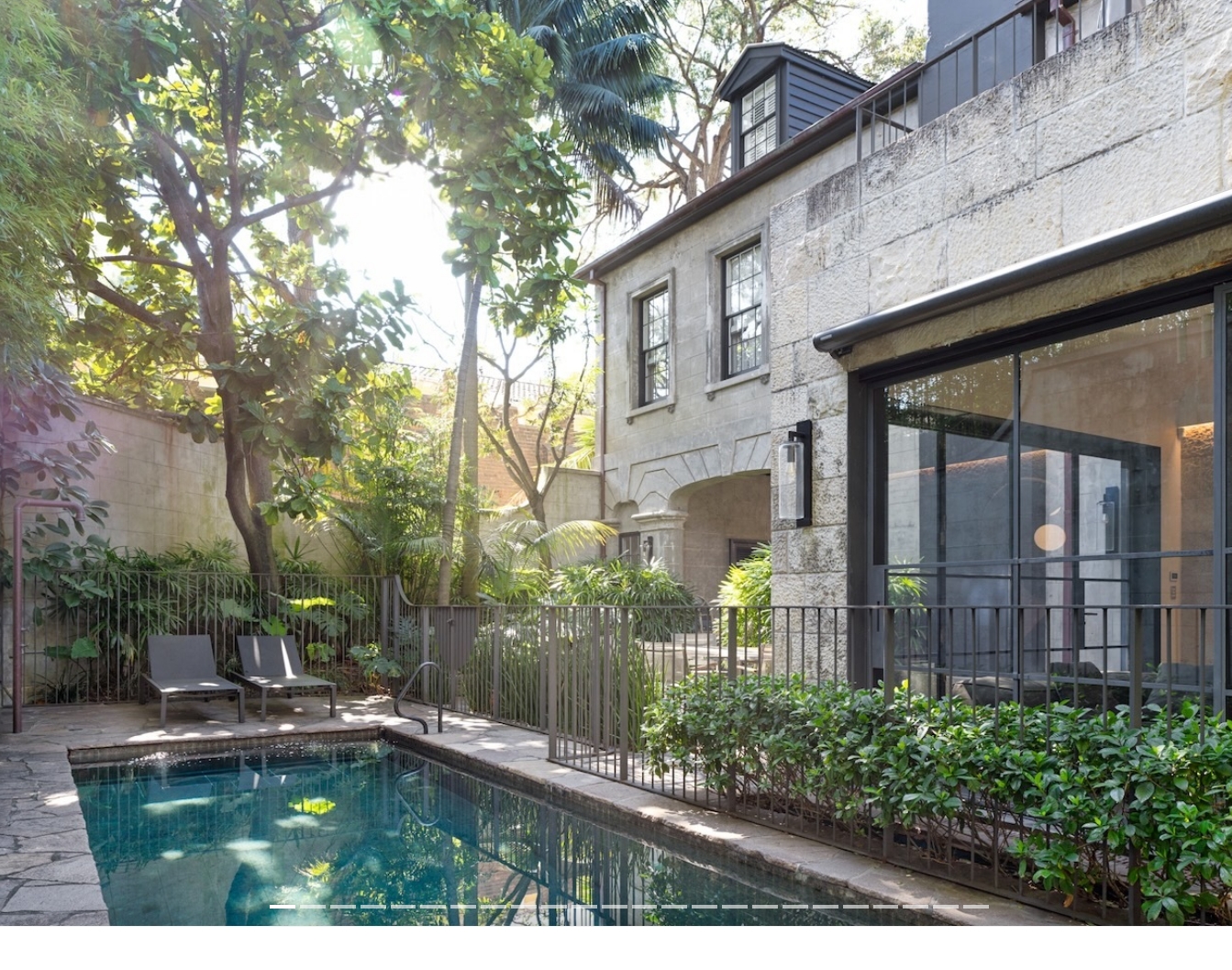

Stoneleigh is being offered for sale for the first time in 36 years. The home is owned by jeweller Vanessa Wong, who took the keys in 2016, after the Wong family paid $3.18 million in 1990. Wong renovated the home shortly after taking ownership, adding a pool to its 650 sqm grounds.

A Landmark on the Heritage Register

‘Stoneleigh’ is recognised on the NSW State Heritage Register for its architectural elegance and historical significance, and remains a defining presence within the tightly held Darlinghurst Ridge heritage precinct, an enclave prized for its concentration of intact colonial and Victorian-era residences just minutes from the CBD.

While the bones of the home date to 1860, its current form reflects a considered architectural transformation by Brian Hess, with landscaping by Dangar Barin Smith, that reconciles the villa’s historic fabric with the demands of contemporary living.

Stoneleigh was added to the State Heritage Register in 1999. It features a hipped corrugated steel roof, a bank of 12 paned timber framed double hung windows to the first floor, and arched colonnade to the ground floor, all set behind a Victorian cast iron palisade fence and colonnade extends around one side of the building.

Two of its previous owners have included Richard Jones, who was Chairman of the Commercial Banking Company of Sydney and the founder of the Maitland Mercury newspaper. He owned the home for around two decades from 1870. From the mid-1890s, J. Russell French, who was General Manager of the Bank of New South Wales, had the keys.

Grand Interiors, Resort-Style Grounds

Inside, the home unfolds across multiple levels, anchored by a statement marble kitchen with integrated dining that flows into expansive formal and informal living zones. These spaces open out to a private terrace and tropical gardens, blurring the line between indoor and outdoor living in a way that’s become the calling card of Sydney’s top-tier renovations.

The outdoor offering is a standout in its own right: a 3-metre-deep mineral pool with geothermal heating anchors a resort-style entertaining garden designed for year-round use, an increasingly sought-after feature among buyers at the top of the market.

Accommodation is generous with six bedrooms in total. There are two master suites, including a primary retreat built around a Japanese Hinoki bath, along with additional bedrooms, terraces and substantial storage, a rare inclusion in an inner-city heritage home of this era.

Finishes throughout run to French Oak flooring, hand-applied Marrakech plaster walls, bespoke lighting by Michael Anastassiades and a Stuv fireplace, all supported by advanced geothermal climate control, ducted air conditioning and a full security system. A cellar on the lower ground floor houses a functioning heritage well, a genuinely rare survivor that underscores just how much of the property’s 19th-century character has been preserved.

Perhaps most notably for an inner-city heritage property, ‘Stoneleigh’ offers secure parking for up to five vehicles, a feature agents will no doubt lean on heavily, given how scarce multi-car garaging is within walking distance of the city.

Key Features

- Architecturally redesigned by Brian Hess with landscaping by Dangar Barin Smith

- Landmark c.1860 Victorian Regency residence with a refined contemporary transformation

- Resort-style outdoor living with mineral pool, geothermal heating and tropical gardens

- Designer marble kitchen with integrated dining and Sub-Zero, Wolf and Miele appliances

- Multiple formal and informal living zones flowing to an outdoor entertaining terrace

- Two master suites, including a primary retreat with a Japanese Hinoki bath, plus additional bedrooms

- French Oak flooring, Marrakech plaster finishes and bespoke lighting throughout

- Advanced geothermal heating/cooling, ducted air conditioning and full security system

- Stuv fireplace, Michael Anastassiades lighting, retractable awnings

- Secure parking for up to five vehicles — a rare inner-city offering

- Level walk to fine dining, bars, cafes and train stations; 2km to the CBD

- Moments from some of Sydney’s finest schools, including Ascham, SCEGGS and Sydney Grammar

A New Record?

The highest price ever paid for a residential house sold under the hammer in Sydney is $24.6 million, for a home in Vaucluse in September 2020.

Bidding opened at $13 million for the 1,085-square-metre block against an $11 million price guide, and the hammer fell at $24.6 million — well above the $14 million reserve. A young Australian-Chinese couple who’d never bid at auction before walkedaway with the keys. That result broke the previous auction record of $23 million, set by media scion Lachlan Murdoch’s purchase of the Bellevue Hill mansion “Le Manoir” in 2009.

Late last year, Iona, across the road from Stoneleigh, sold by private treaty for $37.5 million. It was bought by Bryant Stokes, son of the billionaire Channel 7 chairman Kerry Stokes, and his wife Dominique. It was sold by investment banker Tim Eustace and his partner Salvador Panui, who bought it from film director Baz Luhrmann for $16 million in 2015.

The PG rating has become the king of the box office. The entertainment business now relies on kids dragging their parents to theatres.

A cluster of century-old warehouses beneath the Harbour Bridge has been transformed into a modern workplace hub, now home to more than 100 businesses.