Even in Its Priciest Neighbourhoods, Buying in Rome Remains a Bargain

Compared with other luxury housing markets in Europe, buyers get more bang for their buck in Italy’s capital

6 min

6 min

Gianluca and Selene Santilli have all of Rome at their feet.

Their four-storey penthouse apartment in an early 20th-century villa sits atop a hill in the Italian capital’s Parioli district. With 360-degree views from sitting rooms and outdoor areas, the property provides glimpses of the dome of St. Peter’s Basilica, residential Parioli’s towering pine trees and the winding course of the Tiber River.

The 4,010-square-foot home has free-standing pavilion-like spaces that suggest an urban compound more than an individual apartment. Now, after nearly two decades in the custom-designed space, the couple have listed the four-bedroom unit with Italy/Sotheby’s International Realty. It has an asking price of $6.1 million.

A similar level of luxury in Milan, Italy’s financial and fashion capital, would cost a lot more, says Gianluca, a 67-year-old attorney. “Rome is cheap,” he says, of both the homes for sale and for rent.

Gianluca and Selene, a 64-year-old office manager, priced their home at just under $1,500 a square foot. In Milan, by comparison, a smaller three-bedroom, 2,750-square-foot unit in a decade-old high-rise, with lavish views and similarly upscale fittings, is listed for $6.445 million, or about $2,350 a square foot.

Roman-style luxury was once associated with the gargantuan villas of ancient emperors and the frescoed palaces of Baroque-era princes, but these days it conjures up another phrase: a bargain.

Affordable Luxury

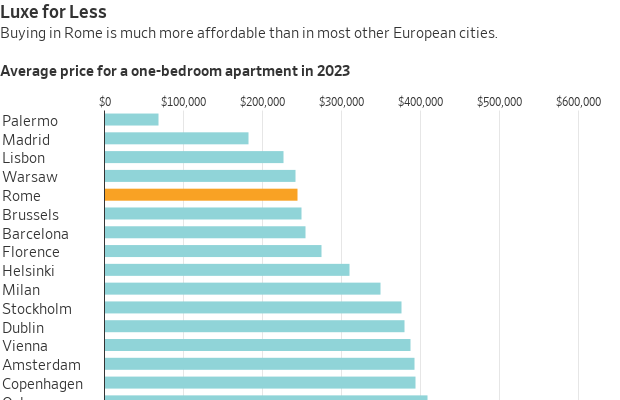

Rome’s average home prices, as of August, were about $350 a square foot—less than Italy’s Florence and Bologna, and around a third less than Milan, according to Immobiliare.it, a real-estate website.

Prices in Rome peaked in 2007, and the city has been slow to encourage new development and investment, says Antonio Martino, the Milan-based real-estate advisory leader for PwC Italy. In Milan, on the other hand, an increase in supply has been outpaced by a greater increase in demand, he says.

A one-bedroom apartment in Rome is far more affordable than the average for major European cities, coming in below Barcelona, Amsterdam and Vienna, according to an affordability index compiled by Savills, the international real-estate company, which analyzed apartments outside of the historic city centres.

An average-earning Roman might need only four years’ salary to buy the apartment, while a Parisian would likely need more than twice that, according to Savills.

Rome’s luxury sector is showing new signs of life, outpacing the rest of the market, says Danilo Orlando, managing director of Savills Residential Italy. Comparing 2023 sales of homes over $1.1 million with prepandemic 2019 levels, he says, prices in Rome have increased 4% while the number of luxury-level transactions has risen 3.6%. Overall real-estate transactions were up 3% in the second quarter of this year, compared with a year earlier, says PwC’s Martino.

Orlando says that residential luxury sales in Rome are traditionally concentrated in three nearby areas that are the city’s most expensive: The Centro Storico, or the historic center, is where centuries-old palaces are often broken up into lavish multi-bedroom apartments. Parioli is a hilly district known for its Midcentury Modern flare. And a short walk away is Trieste, which has clusters of early 20th-century apartment buildings that vie in splendour with their Baroque counterparts down in the centre.

Centro Storico and Trieste

Centro Storico is by far the most expensive, says Orlando, with average prices in the premium sector reaching $1,493 a square foot in 2023. Luxury units in Parioli average about $950 a square foot, while those in Trieste are about $900 a square foot.

Tourists may flock to Centro Storico’s celebrated sites, like the Trevi Fountain, or make their way through the Villa Borghese, a massive landscaped garden that serves as a green space for both Parioli and Trieste. But they are likely to miss the three districts’ prime residential areas, which can seem discreet, if not outright hidden.

Centro Storico’s Via Giulia, running just east of the Tiber, and Via Margutta, tucked under Piazza del Popolo, are hard-to-find streets if you’re not looking for them. Via Giulia was once the address of choice for Roman nobles, and it can still lay claim to being one of the city’s most prestigious streets. A two-bedroom Via Giulia triplex, located in a building dating back to the 16th century and outfitted with vintage coffered ceilings, is listed with Italy/Sotheby’s, with an asking price of $2 million.

The centrepiece of Trieste is the Coppedè quarter, a neighbourhood of towering 1910s and ’20s apartment buildings, decorated with Moorish arches and ghoulish gargoyles, and built around a storybook-like frog fountain. Conceived by an eccentric Florentine-born architect named Gino Coppedè, the quarter combines Art Nouveau elements with a range of historical styles.

Exclusive RE/Christie’s International Real Estate has a well-maintained, four-bedroom Coppedè listing for $3.56 million. Original details in the 3,770-square-foot home include stained-glass windows, mosaic tile floors and painted ceilings.

Parioli and Pinciano

Parioli, with its many steep streets, is a bit more remote, while Trieste is flatter and more urban. For many luxury-minded Romans, a fine compromise is Pinciano, a neighborhood beneath the heart of Parioli that is as rarefied as its hilly neighbour but as accessible as Trieste.

In 2007, Dr. Claudio Giorlandino, a Roman gynaecologist, created a sprawling family home in a Pinciano building that had been commissioned just before World War I, he says, by a member of the House of Savoy, then the Kingdom of Italy’s ruling family. Designed by a noted Venetian-Jewish architect and decorated with marble recovered from a Palladian villa in northeast Italy, the building has a small number of units, with Giorlandino’s 6,200-square-foot apartment taking up a whole floor.

“I love the elegance and the extremely refined, aristocratic atmosphere,” Giorlandino, now 70, says of his neighbourhood, which borders the Villa Borghese.

Now that two of his three children are grown and living on their own, he has listed the home with Exclusive RE/Christie’s for $6.89 million.

Rome’s three most expensive districts can seem like a self-contained world, with residents moving around between them. Giorlandino, who relocated from the Centro Storico to Pinciano, is now thinking about moving back to the historic centre. The Santillis, who moved to Parioli from Trieste, are considering looking for a more compact rental still in Parioli, which they say feels insulated from the Italian capital’s notorious traffic.

“We have the historic centre nearby, but we are not in the chaos of the centre,” says Gianluca Santilli, adding that he considers “the jewels” of his unique penthouse to be the home’s three parking spaces.

Vatican views

American buyers, traditionally drawn to the Centro Storico, are also open to Parioli and to the Aventine Hill, a very steep, purely residential area on the edge of the historic centre, says Diletta Giorgolo, head of residential at Italy/Sotheby’s.

Known for its jaw-dropping views of the Vatican and for its sedate, almost suburban quality, the Aventino, as Italians call it, may be Rome’s most elusive address. Premium listings rarely come up for sale.

Lionard Luxury Real Estate currently has a ¼-acre Aventino compound, with an early 20th-century 10,800-square-foot villa, listed for $22.2 million.

Mother-daughter apartments

A new Centro Storico development proved too good to pass up for Delphine Surel-Chang, a U.S.-born student studying business in Rome, and her French mother, former actress and investor Francoise Surel, who will also relocate.

The two are putting the finishing touches on their new homes in the Palazzo Raggi, where 21st-century details are being installed in a renovated 18th-century palazzo situated between the Trevi Fountain, Piazza Navona and the Pantheon. This summer, Surel purchased a 1,460-square-foot, two-bedroom apartment for herself, and Surel-Chang says her parents helped her buy a 645-square-feet one-bedroom. The units cost $1.88 million and about $944,000, respectively. They are set to move in later this year.

Surel-Chang, 20, says she loves how the project’s contemporary elements—which she and her mother, 60, are augmenting with kitchens and bathrooms from Italy’s sleek Boffi brand—are housed in a classical setting. And she appreciates amenities like a concierge and home automation, allowing residents to control temperature, lighting and appliances via app.

She was able to customise her unit’s interiors, she says, by drawing inspiration from her two favorite local hotels, the Bulgari Hotel Roma and Six Senses Rome. She plans to furnish the unit, where she says they will stay for at least three years, with Italian Midcentury Modern pieces.

The duo bought the apartments—which are a five-minute walk from Via Condotti, Rome’s premier shopping street—for between $1,200 and $1,500 a square foot, using Italy/Sotheby’s, which also helped develop the project.

The apartments can seem like a bargain compared with similarly situated units in other major cities. For instance, a two-bedroom, 2,025-square-foot apartment in London’s Mayfair district—a five-minute walk from Bond Street, Via Condotti’s U.K. shopping district equivalent—is asking nearly $10,000 a square foot.

Affordability played a part in their choice of the Eternal City, says Surel-Chang. They considered relocating to Paris, she says, but soon realised that “for the price of an apartment in Paris, we can afford two in Rome.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

Australia’s housing affordability crisis is being fuelled by chronic undersupply, planning delays and rising development costs, as politicians continue to focus on the wrong solutions.

3 min

Australia’s housing crisis will not be solved by first-home buyer incentives or tax changes alone, with leading property figures warning governments must tackle supply constraints if affordability is to improve.

Speaking at the Kanebridge Quarterly Property Leadership Summit in Sydney last week, expert project marketing specialist Sam Elbanna, property investor and fund manager Paul Miron and property consultant Karla McNeice said that a lack of housing supply remained the central issue facing the market.

Elbanna, Director of CPM Realty with more than 30 years’ experience in project sales, argued that successive governments had focused too heavily on stimulating demand rather than addressing the barriers preventing new housing from being delivered.

“The misconception is that politicians think the way to solve the housing crisis is to drive demand,” he said.

“The reality is that’s not the way. This is a supply-side problem, and it needs to be solved on the supply side.”

Drawing on his experience in project sales, Elbanna said policies designed to help first-home buyers often had unintended consequences, pointing to previous grants that ultimately flowed through to higher property prices.

Instead, he said developers were facing increasing red tape, approval delays and rising costs, which were discouraging new housing supply.

“In the absence of stock, demand exceeds supply,” he said.

Miron, a Co-Founder and Fund Manager of Msquared Capital, said the housing debate had become overly focused on tax policy while overlooking broader structural issues.

He argued that affordability challenges stemmed from a combination of factors, including planning constraints, supply shortages, migration levels and interest rates.

“No-one can be 100 per cent certain on the real reason for property prices is going up,” he said.

“The reason why property prices are higher is a combination of interest rates, lack of supply, migration, vacancy rates and maybe taxes play a role.”

Miron was critical of recent federal housing policy changes, warning they could reduce the number of new homes being built and further constrain supply that was even highlighted in the budget.

He also highlighted the importance of the property sector to the broader economy, noting that residential real estate and related industries employed more than one million Australians.

McNeice, who advises developers on sales strategy and market intelligence, said understanding buyers had become increasingly important as affordability pressures intensified.

While affordability remained a major consideration, she said today’s buyers were focused on value rather than simply price.

“People are looking for value for money,” she said.

She said buyers were increasingly evaluating factors such as transport connections, walkability, nearby amenities and flexible living spaces that could accommodate changing family needs.

“What infrastructure is going on? Can I walk to the shops? Can I meet people at the local cafe?” she said.

The panel also discussed the mounting pressures facing developers, with Elbanna arguing that many projects become financially unviable from the moment a site is purchased.

“The viability of a development happens at the moment the site is bought,” he said.

He said rising construction costs, higher interest rates and overly optimistic feasibility assumptions had left some developers exposed as market conditions changed.

While acknowledging the growing number of smaller and first-time developers entering the market, Elbanna said property development required expertise across finance, construction, marketing and legal disciplines.

“It is actually a business that requires a level of expertise,” he said.

Looking ahead, the panel agreed opportunities remained in the market despite current challenges.

Miron said property should continue to be viewed as a long-term investment and cautioned against trying to time short-term market movements.

McNeice said success would increasingly depend on identifying projects that genuinely met changing buyer expectations.

Elbanna said affordable housing remained achievable, but developers needed to deliver more than just homes.

“We can provide affordable housing in this country,” he said.

“But we’ve got to wrap that affordable housing with the things that people want.”

As Australia’s housing affordability debate intensifies, the panellists agreed on one point: without a meaningful increase in housing supply, demand-side measures alone are unlikely to solve the nation’s property challenges.

The sports-car maker delivered 279,449 cars last year, down from 310,718 in 2024.

Sydney Children’s Hospitals Foundation CEO Kristina Keneally says Australia’s culture of large-scale philanthropy is becoming more sophisticated as Gold Dinner raises $75.5 million for children’s health, research and innovation.