DOUBLE-DIGIT HOUSE PRICE GROWTH ARRIVES AHEAD OF EXPECTATIONS

Australia’s housing market defies forecasts as prices surge past pandemic-era benchmarks.

2 min

2 min

Australian house prices are surging again, delivering double-digit annual growth months ahead of schedule.

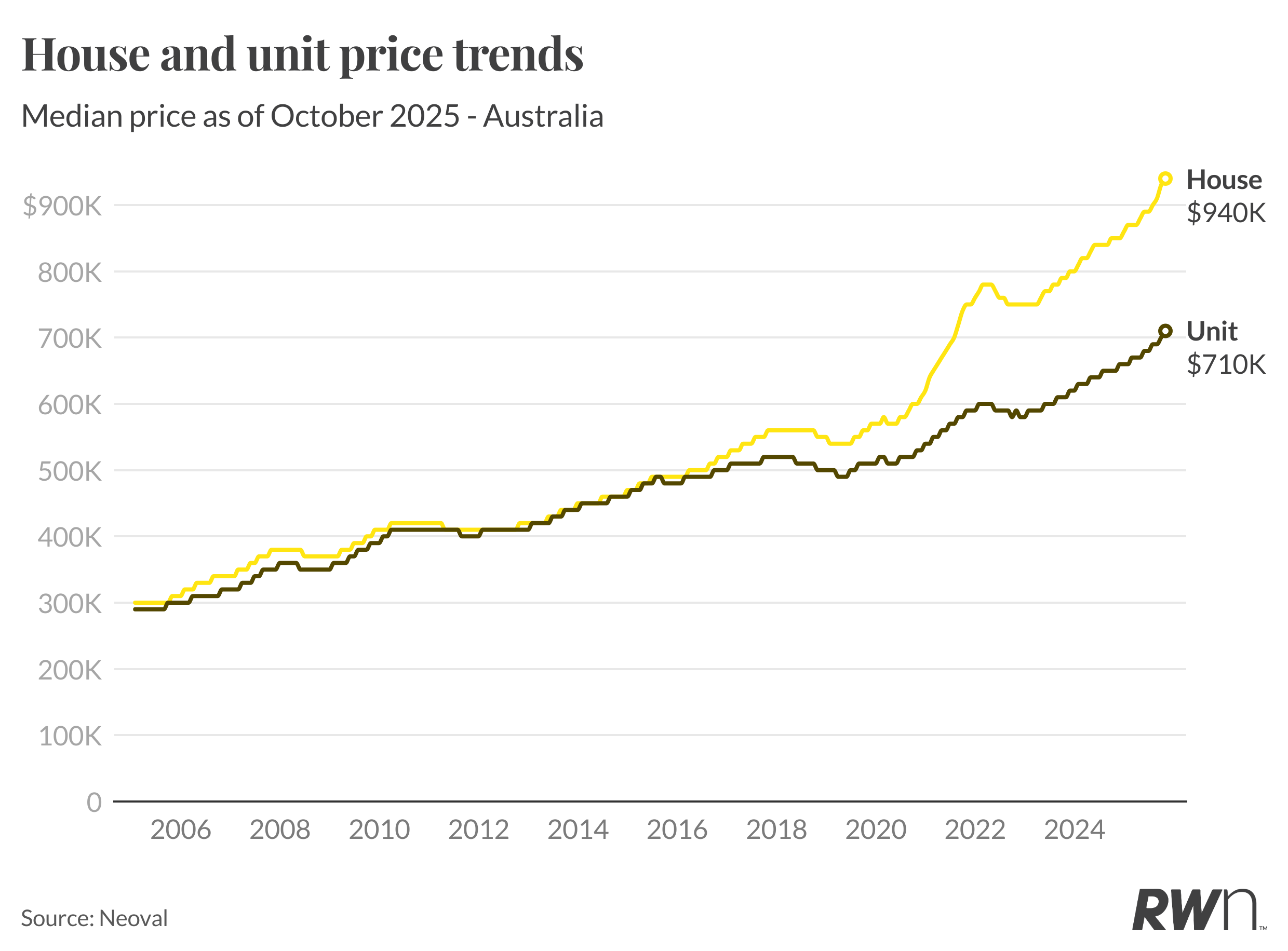

Nationally, the median house price climbed 1.1 per cent in October to $940,000, lifting annual growth to 10.6 per cent, the first double-digit increase since the 2021–22 property boom.

Market Resilience Surprises Analysts

The acceleration comes earlier than expected, according to Ray White Group Chief Economist Nerida Conisbee, who says the milestone was originally forecast for the end of the year.

“Stronger-than-expected October gains and continued tight supply across most markets have pushed growth ahead of schedule,” Conisbee said. “This shows how resilient demand has remained through spring.”

Perth (+14.8 per cent), Brisbane (+12.5 per cent) and Adelaide (+10.8 per cent) continue to lead the charge among capital cities, while Sydney (+8.6 per cent) and Melbourne (+6.5 per cent) show steady, consistent increases.

Regional Markets Extend Their Lead

Beyond the capitals, regional Australia is powering ahead, particularly in the resource states.

Regional Western Australia jumped 16.4 per cent year-on-year, and regional Queensland followed close behind at 14.5 per cent, as population growth and affordability continue to drive demand.

Units Outperform Houses

Unit prices rose even more sharply in October, up 1.4 per cent to $710,000, marking 9.2 per cent annual growth. Conisbee said affordability pressures, new first home buyer incentives, and a lack of available stock are pushing more buyers into the apartment market.

“Units are now seeing stronger monthly gains than houses, reflecting both affordability constraints and renewed first-home-buyer activity,” she said.

The biggest monthly jumps were in Perth (+1.6 per cent), Adelaide (+1.5 per cent), and Brisbane (+1.4 per cent). Melbourne’s unit market also firmed, up 1.6 per cent, as buyers returned to lower price brackets.

Spring Demand Defies Higher Listings

Despite an influx of spring listings, new stock has failed to match the intensity of buyer demand. Nationally, house prices have now risen every month since February, and unit prices every month since March.

“The pace of growth shows demand hasn’t been dampened by higher supply,” Conisbee said.

Outlook: Steady Growth Into 2026

The data comes as the Reserve Bank prepares for its Melbourne Cup Day meeting, where rates are expected to remain on hold at 3.6 per cent.

With inflation easing only gradually and unemployment sitting around 4.5 per cent, analysts expect monetary policy to stay steady for now.

Ray White’s forecast suggests 2025 will close with high single- to low double-digit annual growth nationally, with smaller capitals and regional areas tipped to outperform well into 2026.

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

As interest rates, inflation and market sentiment fluctuate, investors are being urged to focus on data, not panic.

A record-breaking $11 million sale at The Centennial Collection has set a new benchmark for luxury apartment living in Bondi Junction.

3 minThe Centennial Collection, the new apartment development on the edge of Centennial Park in Bondi Junction, continues to break local residential property records.

A local Eastern suburbs buyer has splashed $11 million on a three-bedroom, sub-penthouse on level 10 of the development, topping the previous record within the same development.

At 266 sqm, including internal and external space, the north-facing residence achieved more than $55,000 per sqm, making it one of the most expensive apartment transactions ever recorded in Sydney’s eastern suburbs outside the harbourfront enclaves of Double Bay and Darling Point.

The buyer had originally purchased a three-bedroom apartment in The Centennial Collection in 2025 for $6.5 million before deciding to secure the larger half-floor sub-penthouse.

Ray White Projects Director of Sales Marcello Bo, who is managing sales for the project, said the transaction highlighted the continued strength of demand for premium apartments in Sydney’s eastern suburbs.

“This sale is a clear indication of buoyancy in the upper end of the market and reinforces the strong demand and appetite for primely located, larger-sized apartments with all the luxurious inclusions you would expect with a development of this calibre,” Bo said.

“It also demonstrates that superbly-designed, lifestyle-driven residences in tightly held locations continue to outperform, particularly when they deliver scale, privacy, rarity and long-term liveability that aligns with how buyers want to live today.”

The Centennial Collection occupies a prominent gateway site overlooking Centennial Park at the junction of Bondi Junction, Woollahra and Paddington. Following recent State Significant Development approval, the project now comprises 79 apartments across two adjoining towers rising 13 and 16 storeys.

The development has been designed to target owner-occupiers seeking larger-format apartments, with residences featuring inclusions more commonly associated with standalone homes, including private rooftop pools, bedroom fireplaces, wet bars, butler’s pantries and full-sized wine fridges.

The record-setting residence was originally designed as one of the project’s penthouses before the approval process allowed additional levels to be added to the scheme.

Positioned on Level 10, the apartment occupies half a floor and has no common walls. It offers 270-degree views spanning Sydney Harbour, the Harbour Bridge, Opera House, Centennial Park and both the northern and southern headlands.

The purchaser said that proximity to Centennial Park, transport connectivity, and the surrounding lifestyle amenities ultimately drove his decision.

“I’m constantly looking at developments everywhere in the east, from Darling Point to Rushcutters Bay, Double Bay, all the beaches, Bondi, Bronte, Tamarama, Woollahra. I wanted something new,” he said.

“Everywhere you go, there’s a trade-off. It might have a great floor plan, but it doesn’t have a view. Working in the city, your daily commute impacts everything, so Bondi Junction train station was a huge factor in my decision.”

The buyer, an avid cyclist who rides regularly in Centennial Park, said his view of the location changed significantly as he spent more time assessing the eastern suburbs market.

“At first, I thought, who would want to live there? It’s one of the busiest intersections in the eastern suburbs. But when you peel it all back, it’s one of the best locations in Sydney. You’re close to everything, you can walk to everything, the amenity is incredible, and the views are amazing.”

Bondi Junction is slated to look materially different in the coming decades, with a draft 100-page masterplan proposing a regeneration of the suburb which would include thousands more apartments as well as a revitalised commercial, retail, and dining precinct.

A restored 1860s Brisbane residence transformed by GRAYA has smashed Paddington’s house price record, selling for more than $12 million.

ABC Bullion has launched a pioneering investment product that allows Australians to draw regular cashflow from their precious metal holdings.