China’s Ghost Cities Are a Problem for Europe’s Luxury Brands, Too

Chinese consumers watching the value of their homes fall are losing the confidence to spend on designer goods

3 min

3 min")

How closely is demand for $3,000 handbags tied to home prices in China? Quite closely, it turns out, which is unfortunate for luxury brands.

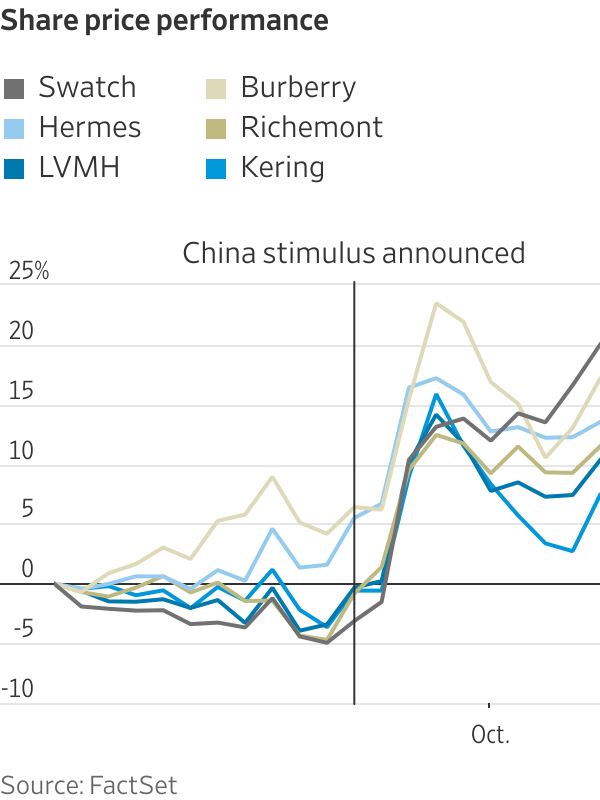

Europe’s luxury stocks fell in early trading Tuesday after China’s economic planning agency failed to announce additional measures to kickstart growth that some investors had hoped for. The sector is still up 10% on average since Beijing launched its initial stimulus plans late last month.

Beijing hopes a cut to mortgage rates, and lower down-payment requirements for buyers of second homes, will jump-start the country’s troubled housing market. A package of loans to brokers and insurers to buy Chinese shares has had initial success at lifting the stock market.

Luxury spending in China has traditionally been more correlated with its home prices than with the financial markets or overall economic growth. Around 60% of net household wealth was tied up in property before prices peaked in 2021. Barclays estimates that falling home prices have destroyed about $18 trillion in household wealth since then, which is equivalent to roughly $60,000 per family.

This, along with worries about the wider economy, is hurting consumer confidence. Retail sales rose just 2.1% in August compared with the same month last year, according to data from China’s National Bureau of Statistics. When global luxury brands start to report their third-quarter results next week, Chinese demand is expected to have slowed since they last updated investors.

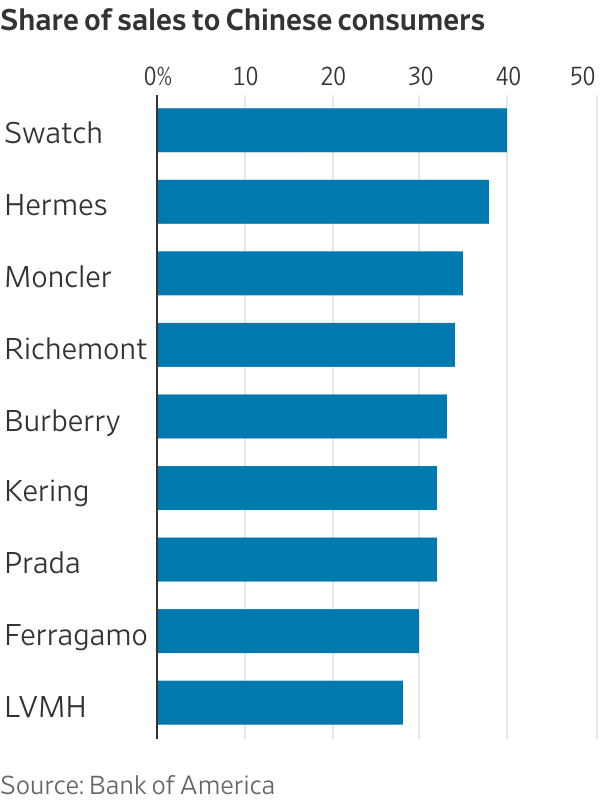

Flagging sales come at an unhelpful time for Europe’s luxury companies, which rely on Chinese consumers for a third of global luxury spending. After several bumpy years during the pandemic, luxury brands and their investors hoped that a comeback in Chinese spending would compensate for a slowdown among Europeans and Americans.

This looks increasingly unlikely. Luxury sales to Chinese shoppers are expected to shrink 7% in 2024 and by 3% next year, according to UBS estimates. As luxury brands have high fixed costs, including the most expensive retail rents in the world, a slowdown with such key customers could have an outsize impact on profit margins.

The last time the luxury industry went through such a rocky patch in China, barring the pandemic, was between 2014 and 2016 when Beijing was cracking down on corruption, including officials who were gifting Louis Vuitton handbags and Rolex watches in exchange for political favours. The global luxury industry barely grew for two years during China’s anticorruption drive, which also coincided with a property-market correction in the country. It didn’t help that shoppers in other markets were also tiring of logos back then.

Europe’s luxury stocks look expensive today compared with that time. As a multiple of expected earnings, listed brands’ shares now trade at a roughly 40% premium to their 2014 to 2016 average.

To justify the higher price tag, Beijing’s housing and wider economic stimulus would need to indirectly lift luxury demand. Measures rolled out so far may not be enough to slow the slide in home prices. China’s housing market is oversupplied by around 60 million units, according to Bloomberg Economics estimates.

New incentives to kick-start consumption are expected soon but will probably target mass-market products like white goods. China already rolled out trade-in subsidies for home appliances earlier this year and a range of consumption coupons.

None of this is very helpful for sellers of expensive luxury goods. For brands to see a recovery, Chinese consumers that spend anywhere from $7,000 to $43,000 a year on luxury products would need to feel much better about their finances than they currently do. Spending by this group has fallen 17% so far this year compared with the same period of 2023, according to a report by Boston Consulting Group.

Half-finished, abandoned housing estates are a big headache for China’s government, and are also on the mind of executives in Paris and Milan. Though the fortunes of luxury bosses likely isn’t high on Chinese officials’ priority list, their fates may be intertwined.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

From bushland greens to valley reds, the country’s most awarded designers are proving that the best colour palette was never on a swatch card; it was outside the window all along.

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

The influencer and fitness entrepreneur is offloading the four-bedroom Main River residence she has called home since 2020 following her split from ex-husband Matt Zukowski.

< 1 min

Fitness entrepreneur and social media personality Tammy Hembrow has put her Broadbeach Waters mansion on the market, ending a six-year stint in the riverfront home she has regularly featured in content shared with her millions of followers.

Hembrow bought the property in June 2020 for $2.88 million.

Sitting on an oversized 979sqm allotment with north-east orientation and more than 30 metres of river frontage, the double-storey residence is set behind security gates at the end of a quiet cul-de-sac.

The home has been a fixture of Hembrow’s online presence for years, serving as the backdrop to family life and business updates for the mother-of-three, who also lived there with her former husband, Love Island Australia star Matt Zukowski, before the pair separated in mid-2025 following a brief marriage.

Inside, the residence centres on an open-plan kitchen, lounge and dining area that opens onto the pool and alfresco entertaining space, designed to make the most of the Gold Coast’s indoor-outdoor lifestyle.

Upstairs, the master suite includes a walk-through robe, dedicated dressing room and ensuite, alongside two further bedrooms, while a fourth bedroom downstairs offers separate access for guests or extended family. A multi-purpose room adds flexibility for use as a media room, home office or children’s retreat.

Outdoor features include a tiled pool, built-in barbecue and bar area, firepit and private boat ramp — amenities suited to the waterfront entertaining lifestyle the Broadbeach Waters pocket is known for.

The property is being marketed by Jay Helprin of Ray White through an expressions of interest campaign, with private inspections only and no scheduled public opens.

Hembrow, who built her public profile from 2014, documenting her fitness journey through three pregnancies, went on to launch fitness app TammyFit, which has since been downloaded more than a million times.

A divide has opened in the tech job market between those with artificial-intelligence skills and everyone else.

International AI strategist Justin Kabbani will headline the Kanebridge Property Summit in Sydney on June 18, with tickets selling fast.