Spring is here and so too is one of the busiest auction weekends of the year, with vendors feeling confident and buyers out in force – a trend economists expect to continue.

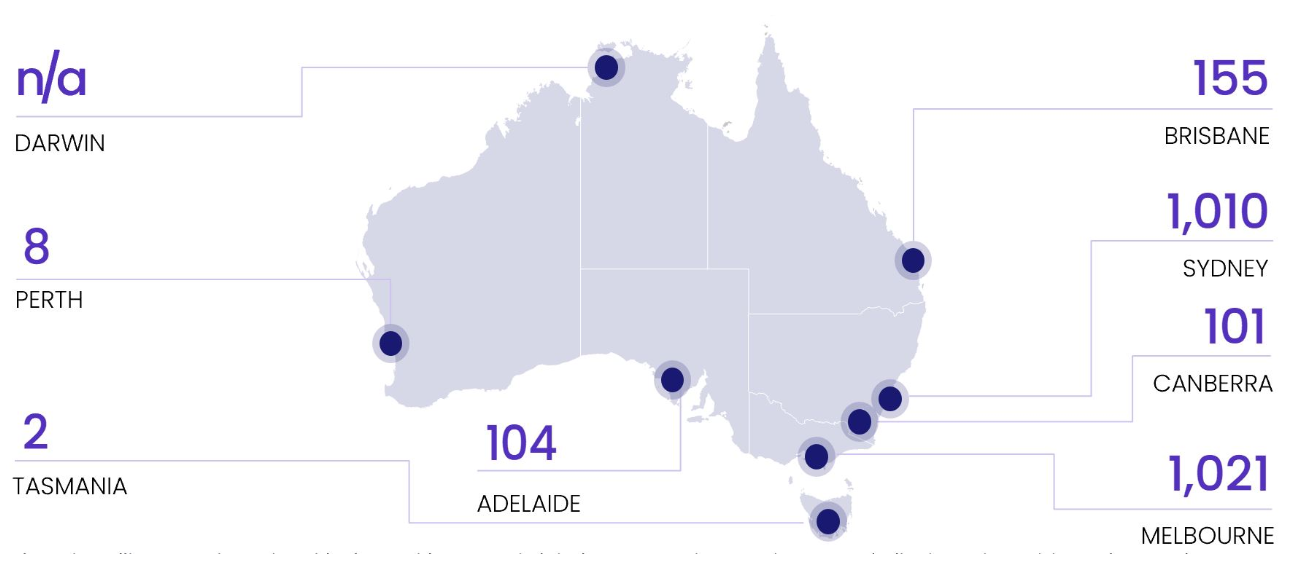

Research firm CoreLogic reports a whopping 2401 homes are set to go under the hammer across the country on Saturday, up 5.4 percent on last weekend and the third largest volume of 2023 thus far.

“Auction activity across Sydney is set to exceed 1000 for the second time this year, with 1010 homes currently scheduled to go under the hammer this week… up 16.5 percent,” CoreLogic economist Kaytlin Ezzy said.

Strong momentum in property markets continues to defy expectations.

About this time last year, most pundits were predicting steep price falls throughout 2023 on the back of soaring interest rates.

Instead, values rose for the sixth consecutive month in August, up 0.8 per cent nationally and now 4.9 per cent higher since bottoming out in February, data released today shows.

Sydney has led the recovery trend, with a rise of 8.8 per cent since prices found a floor at the start of 2023, while Brisbane has also seen values jump 6.2 percent in that time.

Cameron Kusher, director of economic research at data house PropTrack, said the “better-than-expected price growth” had reversed virtually all the declines seen in the backend of 2022.

“Property prices have increased despite rising interest rates and reduced borrowing capacities,” Mr Kusher said.

“From here, the direction of the housing market will likely be influenced by the volume of housing stock available for sale. Low volumes of new and existing properties persisted In June, but this may soon change.”

PropTrack’s newest Property Market Outlook report has forecast national home prices to be between 2 percent and 5 percent higher by the end of the year.

It is a marked turnaround on a previous prediction of a fall of between 7 percent and 10 percent, Mr Kusher said.

“Forecasts for 2024 are considerably more difficult, given the uncertainty of many factors. At this stage, we are forecasting modest price growth in 2024.

“However, significant changes to the overall economic performance, interest rates or lending conditions, could result in vastly different price growth outcomes.”

He predicts prices nationally could be up to 3 percent higher by the end of 2024, with modest growth across most capitals, including up to 2 percent in Sydney and up to 3 percent in Melbourne.

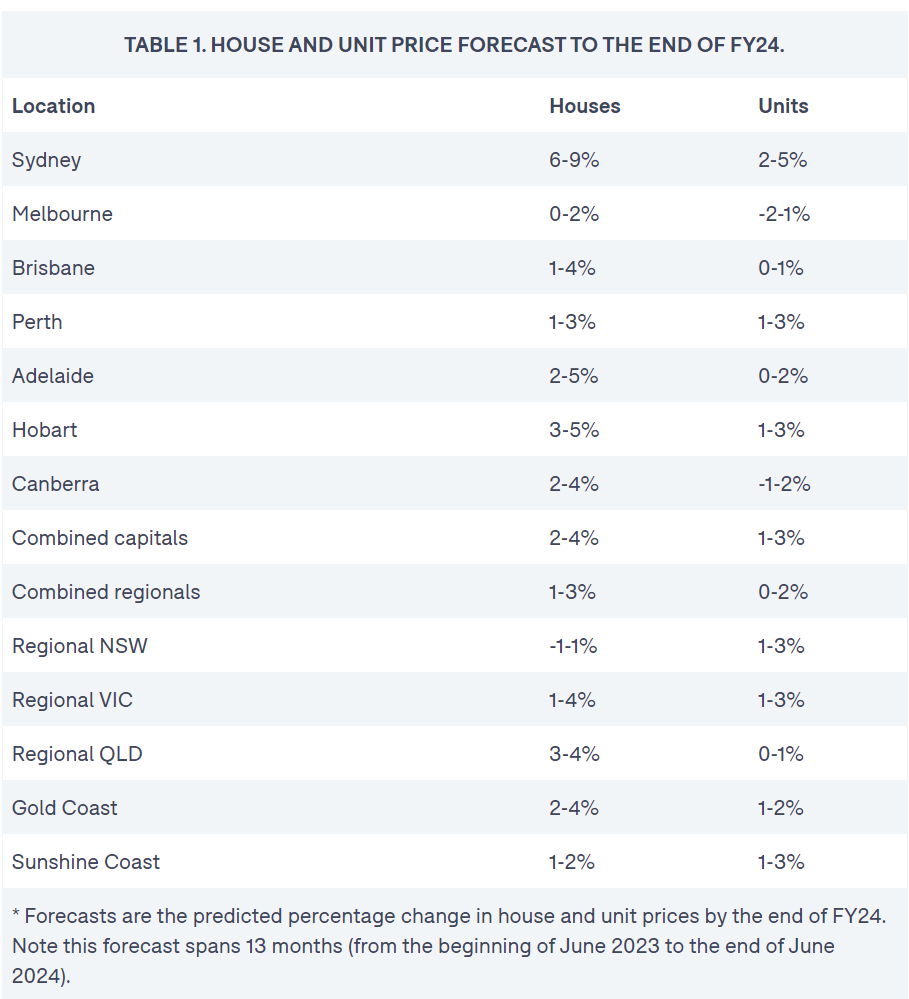

Domain’s recently released Forecast Report is a tad more optimistic, predicting the housing market will be in a “well-established, steady recovery” by mid-next year.

“House prices in Sydney, Adelaide and Hobart will record the largest gains,” the report predicts.

Forecasts are for house prices in Sydney to end the current financial year up to nine per cent higher, with modest growth in Melbourne of up to two per cent and a rise in Brisbane of up to 4 percent.

“House prices in Sydney, Adelaide, Perth and the combined capitals will be at a new record high [while] Brisbane house prices will be close to a new record high,” the report predicts.

Strong population growth is set to put “greater and more immediate pressure” on housing demand, which sees an additional 300,000 dwellings needed to meet needs.

“Typically, overseas migrants rent on arrival, but, with a tight rental market Australia-wide, we may see some arrivals transition to home ownership sooner as they seek more stable housing alternatives.

“This is occurring at a time the construction industry has experienced unprecedented headwinds – skills shortages, supply chain disruptions, and soaring construction costs.”

While prices are expected to rise, affordability pressures, high interest rates and restrictive serviceability buffers will contain the pace of growth, the report reads.

Look, when you drive an electric car, you have to toss out what you know about gas guzzlers. Beyond the bonkers acceleration and quiet-as-a-librarian ride, you have to tackle new complexities like how to tell if the car is…on. Get good and you might even master the art of driving one-pedal without puking.

Plenty of readers know what I’m talking about—and may have already aced the course. But if you’re thinking of buying an EV, or even renting one, you need to anticipate a learning curve.

Why is the Journal’s tech columnist talking about this? Don’t they have a car guy?

As you may have seen in my column and video last week, I tested five leading EV options under $60,000 in search of a second car for my family. Sitting in my garage is the winner, a leased Ford Mustang Mach-E. And yes, I am teaching my sons how to shine it up, Karate Kid style.

My EV exercise wasn’t merely about finding my next car. I wanted to clock just how much the shift to battery power is turning our cars into gadgets, not unlike smartphones and computers. Technology is upending a century-old industry.

For EV adopters, that means waving goodbye to a lot of things we’ve known about driving. I may be an expert at USB-C dongles and buried iPhone menu settings, but I am new to this hot gadget on wheels. Here are things I wish someone had told me before I went electric.

Welcome to Dri-EV-er’s Ed.

How to open the car

“Car door handles, they’re just too easy to use,” said no one ever. And yet EV makers thought they were begging for disruption.

On the Ford Mustang, you press a circular button on the door and it pops open. On the Kia EV6 and Hyundai Ioniq 5, the handle is flush with the car and pops out when the car is unlocked. With the Tesla Model Y, you need to push in the wide part of the handle then pull the longer skinnier part toward you. Thankfully, there’s a GIF for that.

The Volkswagen ID.4’s handle looks like a handle—but you don’t have to pull it out. Nestled under the handle is a sensor. Obviously, you learn how to open the door when it’s your own car, but you’ll always enjoy watching the uninitiated try to get in.

How to turn on the car

My least favourite car game? Power-button hide-and-seek.

“How to turn Tesla on” will be forever burned into my Google search history. I really couldn’t find a power button anywhere because…there isn’t one.

The Ford Mustang Mach-E has a traditional push-button. PHOTO: KENNY WASSUS/THE WALL STREET JOURNAL

Instead of a physical key fob, Tesla provides a hotel-style keycard. You can also use Tesla’s smartphone app as a key. As soon as you open the Model Y’s door, the touch screen powers on and you can operate all controls. To get it moving, you step on the brake and move the gear shifter to Drive.

Volkswagen’s ID.4 is similar: If you have the app or the key fob with you, the car powers up when you sit in the driver’s seat. Press the brake pedal and the drive system activates.

Ford, Hyundai and Kia stick to start/stop push buttons. There are key fobs, but you can also set up the apps as keys.

How to drive the car

OK, you know how traditional automatic-transmission cars creep forward when you take your foot off the brake? That generally isn’t the case with EVs. To move, you tap the accelerator. (Even in reverse, which can be a little unnerving.) As soon as you take your foot off the accelerator, the car slows and brakes on its own. You only hit the brake pedal itself if the car isn’t slowing quickly enough.

Most EVs let you do “one-pedal driving”—that is, driving with only the accelerator.

Why change how we’ve driven for so long? Regenerative braking. These brakes use motors that capture energy and return it to the battery. Hybrids often have a variation of this too, but EVs are all about it. (Here’s a deeper discussion of how it works.)

The rapid, automatic deceleration can be unsettling at first. And some people told me it can make passengers nauseous or queasy. Don’t worry! On many EVs, you can turn off the setting or minimise its intensity. The Volkswagen doesn’t even prioritise it—you have to select the mode. Its default drive mode feels much more like a regular car.

But I’m a total one-pedal convert now. In fact, when I get back in my gas-powered Volvo, I have to remember to hit the brake.

How to know if the car is running

Unlike internal combustion engines that go “vrrrrr vrrrrr VROOOM” when you start them up, EVs sound like futuristic golf carts. I’ve definitely ended up restarting the Mach-E because I wasn’t sure it was on.

The National Highway Traffic Safety Administration has set guidelines for “quiet cars” to protect pedestrians—especially people who are blind or have low vision. Under 19 mph, the cars must emit some sound. My Mach-E beeps when I reverse. The Model Y’s whirring sounds like the spaceship in “E.T.”

Some automakers use synthetic sounds to make these new cars sound old school. In the Mach-E, when I put the car in Unbridled mode and press on the accelerator, it hums like an internal combustion engine.

How to pull in for a charge

I think we can all agree on the greatest automotive invention of all time: the little arrow on the gas gauge telling you which side the fuel cap is on. There’s no standardisation for charging-port location on an EV. (This diagram is proof.) I didn’t see any handy arrows inside the cars I tested. Turns out Hyundai and Kia show a little arrow on the screen (I didn’t see it) and Volkswagen does have a cool map of the car showing the charging port, but it’s a few taps into the settings.

Tesla displays clear instructions on how to back into your Supercharger spot. PHOTO: KENNY WASSUS/THE WALL STREET JOURNAL

Again, you learn when it’s your own car. What’s not as easy to get used to? Reversing into a spot to plug in, a must at many charging stations with shorter cords.

Let me be clear, this is guidance, not a gripe fest. You’ll love driving an EV…as soon as you figure out how to get inside and turn it on.

As a Capricorn, John McIlwee considers himself a spiritual person. But when his psychic told him in late 2021 that he was going to buy another house, he didn’t believe it. McIlwee and his husband, entertainment executive Bill Damaschke, already owned a portfolio of three architecturally significant California homes, and they’d decided not to take on any more projects.

“I said, ‘Hell, no. You’re wrong on this one,’” recalled McIlwee, 56, a Hollywood business manager.

Two days later, they’d signed a contract to buy a circa-1960s house in Rancho Mirage, roughly 10 miles from Palm Springs.

Sometimes, McIlwee just can’t help himself. The idea that someone might tear down or alter a beautiful old house is more than he can bear. In the case of the low-slung Rancho Mirage home, he couldn’t stand the thought that a developer might destroy it.

“I know myself,” he said. “If I let that house fall into the wrong hands and get ruined, it would piss me off every time I drove by.”

Over the past few decades, McIlwee and Damaschke, 59, have purchased and restored multiple houses, including former President Gerald Ford’s onetime estate and John Lautner’s Garcia House, an almond-shape structure considered one of L.A.’s most significant midcentury houses. McIlwee and Damaschke typically hold their houses long term and live in them, hosting parties and sometimes allowing commercial photo shoots.

“We’re living in a world now that is unsustainable with what people are destroying,” McIlwee said. “I didn’t particularly sign up to be some weird preservationist, but I look at these things as kind of like a mark in history.”

The couple admire how billionaire grocery tycoon Ron Burkle has restored a number of important trophy homes across California, McIlwee said. In comparison, he said he and Damaschke might be considered “Ron Burkle Light.”

“Ron’s doing the $50 million things,” he said. “We’re doing the $10 million things.”

McIlwee, a California native, serves as business manager to celebrities such as “The Batman” director Matt Reeves and “Glee” star Jane Lynch. Damaschke grew up in Chicago, where he admired the local Frank Lloyd Wright houses and took high school drafting classes. He originally harboured notions of becoming an architect himself, but eventually wound up in the theatre, working as a Broadway actor and later transitioning to the business side of the L.A. entertainment world. He is now president of Warner Bros. Pictures Animation, and is also a producer of Broadway shows such as “The Prom” and “Moulin Rouge,” for which he won a Tony Award in 2021.

John McIlwee creates social-media accounts for all the couple’s homes. PHOTO: JULIE GOLDSTONE FOR THE WALL STREET JOURNAL

When it comes to their homes, the two said they typically work with the same “rat pack” of professionals, including landscape architect John Sharp, interior designer Darren Brown and architecture firm Marmol Radziner. McIlwee also sets up Instagram accounts for all the homes, posting historic photos and images from their parties and photo shoots.

“They are consummate cheerleaders for their houses,” said Leo Marmol, a California architect who has helped the pair restore several homes. “Their goal is not to pour liquid amber over a historic object to kind of freeze it. It’s the opposite. It’s to invite the world in to celebrate the home.”

McIlwee said he handles most of the logistics and the execution of their projects, while Damaschke is more of a creative thinker and would spend more money if McIlwee didn’t rein him in. Though he doesn’t consider the homes as investments so much as passion projects, “I never want to lose money,” he said.

The pair mostly agree about design choices, with a few exceptions.

“Sometimes we have huge screaming fights and don’t agree on anything,” Damaschke said with a laugh. “But we end up in a good place.”

One of Damaschke’s pet peeves: McIlwee is “classic California” and leaves all the windows and doors of their homes open. “Sometimes I’ll walk through and close the shades or drapes. He’ll come right behind me and open every one of them up after I leave the room.”

Read on for a closer look at the couple’s collection.

The couple’s primary residence for roughly 20 years was the Lautner-designed Garcia House, which sits 60 feet off the ground on concrete caissons. Dating to the 1960s, the three-bedroom home is perhaps best known for its star turn in the 1989 movie “Lethal Weapon 2,” where it appeared as the headquarters for a South African drug-smuggling cartel. McIlwee and Damaschke bought the roughly 2,600-square-foot house for $1.2 million in 2002, property records show.

When it comes to architecture, Damaschke said he’s often fascinated by the narrative behind a home, which was the case here. The original owners, film composer and conductor Russell Garcia and his wife, Gina Garcia, “were real trailblazers,” he said, “because the house was unbuildable. The lot was unbuildable. So, I’m like, ‘What possessed these people to build this amazing structure against the tide of what was popular at the time?”

After living in the property for more than a year to get a feel for the space, McIlwee and Damaschke embarked on a roughly $5 million restoration project at the house, which had fallen into disrepair. They also added an ellipse-shaped pool based on Lautner’s original plans.

Living in the house forced them outside, Damaschke said, since getting from the bedrooms to the main living room requires taking an external staircase. “The flow of it actually invited you to be a part of nature,” he said.

However, “it can be overwhelming, like you’re living in an art piece,” he said. “So we worked hard to make it super cozy and comfortable, like a home.”

Damaschke also called it “the best party house in the world.” The pair hosted numerous parties there, including one for the whole cast of “Moulin Rouge.”

After years in the house, the couple was ready to move on to their next adventure, they said. Earlier this year, the couple sold it for $12.5 million to Nicholas C. Pritzker, a member of the famed Pritzker hotel family.

The Ford Estate in Rancho Mirage was designed in the 1970s for Gerald and Betty Ford after they left the White House. Located less than 2 miles from the Betty Ford Center, the rehabilitation centre founded by the former first lady, the roughly 6,300-square-foot, five-bedroom house faces one of the fairways of the Thunderbird Country Club.

McIlwee and Damaschke caught their first glimpse of the property decades ago during Palm Springs Modernism Week, when they were doing research for their renovation of the Garcia house.

When the house came on the market in 2012 following Betty Ford’s death, they jumped at the chance to see it, and quickly fell in love. The house had its original décor in place, including the 7-foot-tall portrait of Betty Ford in the entryway, the red panic button in the president’s personal bathroom and the lime-green dining room, with its leafy mural and lattice chairs. They signed a contract within just 11 days of the listing going live, paying about $1.6 million.

McIlwee said he enjoys the irony that a Republican president’s home has fallen into the hands of “two gay Democrats.” He said he considers Betty Ford a trailblazer and forward-thinking for her day. “She was very sympathetic to a lot of people,” he said. “That’s the problem with American politics today. Nobody talks to each other.”

The house was designed by Welton Becket & Associates, the company behind the Galactic-style Capitol Records Building in Hollywood, in Desert style, with swaths of glass and a flat roof with overhangs. The vividly colored interiors were designed for the Fords by Laura Mako, who also designed homes for the likes of Gregory Peck and Jimmy Stewart.

The couple did significant work to the property with help from Marmol, but with the goal of maintaining the original structure. “We weren’t looking to make dramatic changes,” said Marmol. “We were actually trying to preserve the original drama of the home, while making subtle interventions to make the house more functional by today’s standards.”

Because of security concerns, the Fords had left the house relatively unexposed to the outside, so McIlwee and Damaschke added several windows and skylights. They opened up the entertainment areas to the outdoor pool and replaced the kitchen, which had been designed more as a service area than as the heart of the house, McIlwee said.

They preserved much of the interior design and furniture, including the Betty Ford portrait, which the Ford family had originally intended to sell at a Gerald R. Ford Presidential Foundation event to raise money. The couple donated to the foundation instead, they said.

“We were like, ‘No, this has to stay with the house,’” Damaschke said. “It’s a showstopper.”

The couple uses the property as a weekend and vacation getaway and frequently host friends and clients there, McIlwee said. They have no plans to sell it.

In 2021, McIlwee made a snap decision to buy a second house in Rancho Mirage, just down the street from the Ford Estate on Sand Dune Road. The move flew in the face of a conversation the couple had recently had about taking a step back from their renovation projects, which take up a lot of time and money.

The rationale? He was concerned that a developer would buy and ruin the house, a modest 1960s home that he believes was designed by the architect William Francis Cody.

“He was very anxious about it,” Damaschke said.

McIlwee chalked his anxiety up to the flipping frenzy that took over the Palm Springs and Rancho Mirage markets during the pandemic. Developers, he said, were buying houses, putting “maybe $100,000” into them, painting them white, adding a cactus and reselling. He found the bright white paint jobs especially abhorrent, preferring the traditional sand tones of desert houses.

“I wasn’t going to let that happen on my street,” he said.

At the time of the purchase, Damaschke said, he was in London and sick with Covid. “I didn’t really have a say in that one,” he said with a laugh. “He snuck it in under the radar.”

“I just said, ‘Sign this,’” McIlwee said.

They paid about $1.4 million for the three-bedroom house, which also sits on the golf course at Thunderbird. Spanning about 3,400 square feet, it has travertine floors and 16-foot sliding doors leading to the pool deck.

The house had undergone several “bad” renovations that have “glommed on to each other,” McIlwee said, and needs a lot of work. They plan on peeling back much of the block siding and basework and removing an addition that a previous owner put on the house. He estimated the cost at around $1 million.

McIlwee said they are unsure of their long-term plans for the property, but they might rent it out.

This year, the couple bought a four-bedroom Modernist house in Beverly Hills designed by the little-known Mexican architect Raul F. Garduno.

Located in the tony Trousdale enclave, the roughly 5,400-square-foot home was built in the early 1970s and has long, curving hallways, a step-down living room and a rounded swimming pool. Its design is unusual, Marmol said, because the various wings of the house seem to splay out from a single point like an off-centre windmill. The house also steps up as the site slopes down, so the house seems to respond directly to the shape of the earth.

McIlwee and Damaschke said they first saw the property when a friend who runs a design company rented it as a show house. “When Bill and I walked in, we were immediately like, ‘We’re going to get this house,’” McIlwee said.

At the time, the property was still owned by the same family it had been built for five decades prior. The original owner’s daughter, Lynne Corazza Anderson, had been fielding offers, McIlwee said, but most of the competitive ones had come from developers, who planned to tear down the house and replace it. Though he was aware of the proliferation of spec developments in the Trousdale neighbourhood, which has drawn celebrities like Jennifer Aniston and David Spade, McIlwee said he found the notion of tearing down the house “dumbfounding.” The couple decided to sell the Lautner house and use the capital to restore the Garduno house.

McIlwee convinced Anderson to hold off on accepting any of the offers for several months so that he and Damaschke had time to sell the Lautner house. Eventually they bought the Garduno house for $9.6 million in April. He estimated that they will spend at least another $3 million renovating it. They already have plans to redo the kitchen and bathrooms. They also intend to wall up some doors in the hallway to create an art corridor.

McIlwee said he also intends to amplify Garduno’s name.

“In every magazine right now, people are talking about Mexico City. Well, this is the perfect example of Mexican Modernism,” he said. “I’m taking it upon myself to give this guy some air.”

The house will be the couple’s new primary home; it is their first time living in the coveted 90210 ZIP Code. Two friends who came to lunch earlier this summer brought the couple a “Welcome to 90210” cake. “I’m still laughing about that,” McIlwee said.

A single-family home is the exception to the rule in high-rise Singapore, where most of the city-state’s 5.5 million residents live in apartments. So when it came time for Mark Tan and Stella Gwee to trade in their starter bungalow for something larger and grander, they decided to stay put, tear down and begin again on their rare 1/10th-acre lot.

In 2009, Tan, now 48, and Gwee, 46, paid 2.2 million Singapore dollars, or about US$1.6 million, for their original 1,500-square-foot house, located in a single-family enclave in Singapore’s North-East region. The couple then spent $2.6 million to replace the three-bedroom, semidetached structure, built in a Balinese-fusion style, with a four-story, seven-bedroom brick house that combines Asian and Western elements across 7,400 square feet.

In all, Tan and Gwee have invested just over $4.2 million in their new home. Multi-bedroom Singapore homes of a similar size could sell now for twice that.

The couple—Gwee works with her husband, a local entrepreneur—began demolition in 2020, relocating with their two children, Xavier, now 17, and Andrea, 13, to a nearby rental for the two years of construction. The family, along with dogs Furry and Brownie, moved into the finished house in early 2022.

The new home’s standout feature is a landscaped vertical courtyard, rising nearly 40 feet. “A lot of Singaporeans won’t sacrifice the space to build a courtyard like this,” says Tan, a Singapore native, who grew up nearby.

Enclosed by a skylight, the space is outfitted at the top with a large industrial fan 8 feet in diameter that is powerful enough to ventilate a factory floor. Made by Southern California’s MacroAir, the fan helps the family keep cool in Singapore’s year-round tropical weather. It is part of a $74,000 climate-control system that allows every room individual air-conditioning units.

The flora-rich courtyard, featuring an indoor koi pond and fronted by an open-air outdoor swimming pool, opens to the street at its base between the pool and the pond. The house can be closed off and revert entirely to air conditioning on especially hot days.

The open-plan first floor includes living and dining areas, and has space enough for a Steinway piano for music student Andrea. The second floor is given over to a mahjong room that doubles as a guest bedroom and a study. The bedrooms are on the third floor. The fourth floor serves as a penthouse recreation room for the kids and their friends.

The elevator makes for easy transitions, but Tan says his health-conscious wife takes the stairs.

Windows and terraces orient the house around the courtyard. Designing an expansive vertical courtyard was a challenge, says the couple’s architect Han Loke Kwang, principal in Singapore’s HYLA Architects, which specializes in upscale single-family projects (or landed properties, as locals call them). Immense vertical spaces like this are seen in commercial structures but are unusual in a residential setting, says Han.

The goal in the Tan-Gwee home, he says, was “to make sure the scale of the courtyard wasn’t overwhelming.”

Foliage—chosen to flourish in the courtyard’s shaded conditions and kept fresh with an elaborate irrigation system—and the koi pond help ornament the space. The pond gives the first floor a waterfront feel.

The couple spent $148,000 on the pool and pond areas. Tan filled the pond with $59,000 worth of top-dwelling adult koi, mostly imported from Japan, and several bottom-dwelling freshwater stingrays, costing $22,000.

Singapore, which is smaller than Los Angeles County, is a blending of cultures, bringing together East Asian, South Asian and European influences. The Tan-Gwee home has a decidedly cosmopolitan flair, combining Italian designer furniture, British and Canadian lighting, kitchen appliances from Germany’s Miele, and bathroom details inspired by vacations in Dubai and the Maldives.

The fortresslike facade, which preserves the privacy of the home, is in keeping with Asian residential models, says Han.

Many of Han’s clients have two kitchens—an open area for Western-style cooking and a closed-off Asian-style cooking space with wok stations, requiring extra ventilation. While finishing the house, Tan and Gwee decided to forgo the planned Asian kitchen, converting it into a kitchen terrace equipped with an $11,000 barbecue.

Back inside, the kitchen was outfitted with a steam oven, two conventional ovens of different sizes and a built-in Miele coffee machine.

These are booming times in Singapore. The city-state now has a per capita GDP of more than $91,000, higher than anywhere else in Asia and one of the world’s strongest residential markets.

Overall residential real-estate prices rose 7.5% between the second quarters of 2022 and 2023, with those of landed residences increasing by 9.4% in the same period, says Nicholas Keong, senior director of Knight Frank’s Singapore affiliate. Also, Singapore came in first in Knight Frank’s Prime Global Rental Index—far exceeding London, New York, Monaco and Tokyo—with rent prices rising 28% in 2022.

The couple seem to have exhausted their wish list. When you have everything from three ovens to a stingray budget, there isn’t much left. What about a home spa? “No sauna here,” counters Tan, who relies on the primary bedroom’s three air conditioners to maintain comfort. “It’s already too hot in Singapore.”

OTHER COSTS

Foundation and framing: $589,400

Electrical work: $148,000

Designer Lighting: $74,000

Elevator: $88,400

Kitchen (including appliances): $222,000

Bathrooms (7): 148,000

Brickwork/masonry: $222,000

Glazing, including windows and sliding glass doors: $222,000

Landscaping, including indoor plants and irrigation: $73,700

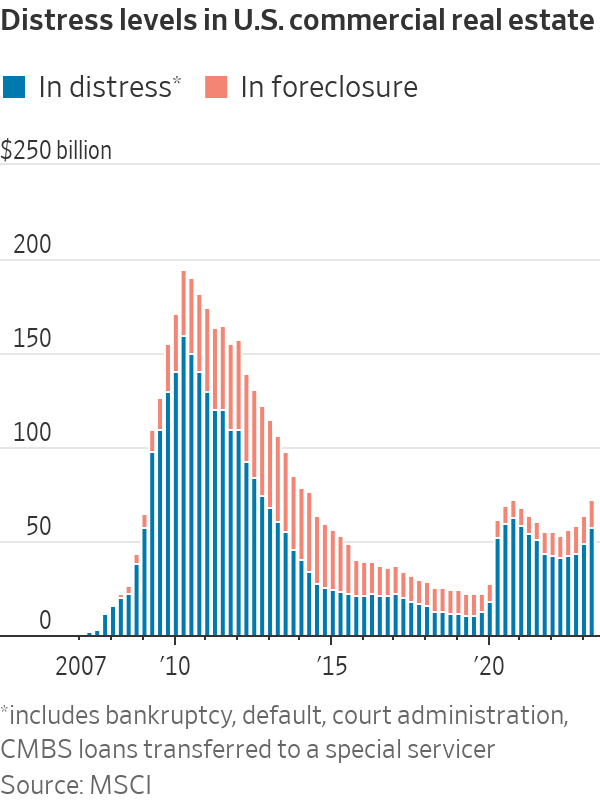

Is the pain over yet for U.S. commercial real estate? The answer might be yes for stocks but no for the assets they own.

A record $205.5 billion of cash is earmarked for investment in U.S. commercial real estate, according to dry-powder data from Preqin. But good deals may not be available for another six to 12 months. Here are some trends investors can watch for signs of when it is the right time to buy.

How Much Are Values Down Already?

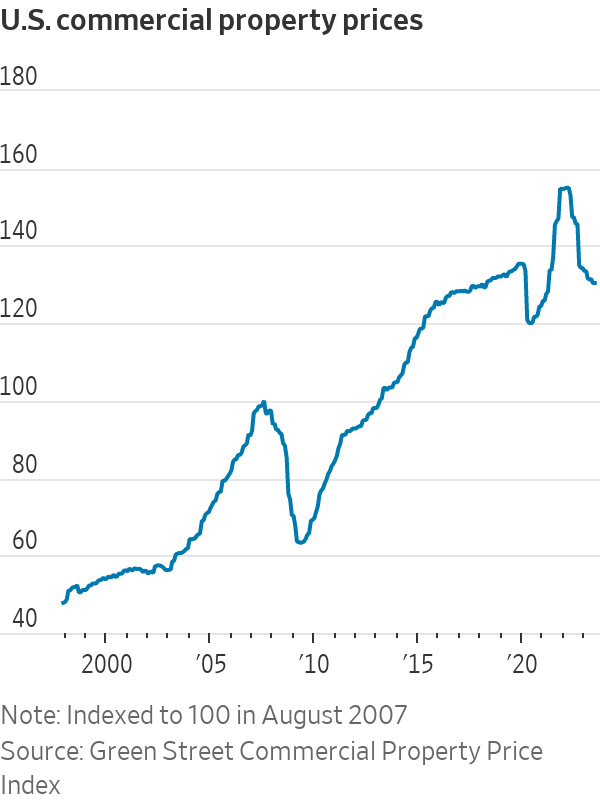

U.S. commercial property prices have fallen 16% on average since their peaks in March 2022, according to real-estate research firm Green Street. Unlike the 2008 crisis, when a lack of credit hurt the value of all real estate, today’s downturn has hit some types of properties much harder than others.

Unsurprisingly given remote working, offices are the worst performers, having lost 31% of their value since the Fed first began raising interest rates. The discount isn’t as enticing as it sounds, as troubled buildings need heavy investment to bring them up to a standard that will attract tenants, or to be redeveloped for new uses.

Meanwhile, prospects for snapping up America’s e-commerce warehouses at knockdown prices look slim. Warehouse values are down just 8% from peaks to reflect higher financing costs, and top industrial stocks like Prologis don’t look cheap either, trading close to net asset value.

Apartments might be a better bet for those hunting for distressed assets. Prices for multifamily apartment buildings have fallen by a fifth since March 2022. Some owners who paid top dollar for properties during the pandemic using short-term, floating-rate debt may be forced to sell if mortgage repayments become unmanageable when their interest rate hedges expire.

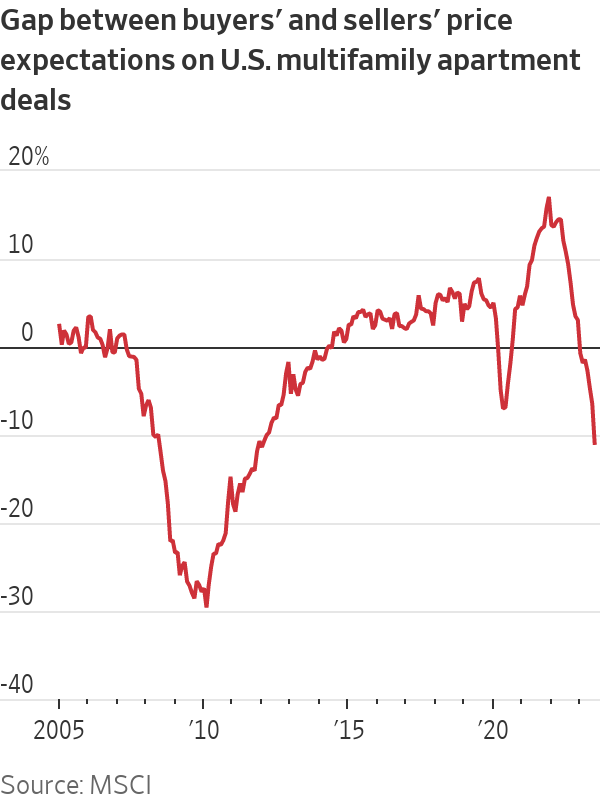

Property Sellers Are Still Demanding Yesterday’s Prices

Sellers are holding out for prices that are no longer realistic. MSCI’s bid-ask spread reflects the difference between what U.S. property owners are asking for and what buyers are willing to pay.

As of July, the gap for multifamily apartments was 11%, the widest it has been since early 2012, when the property market was still recovering from the 2008 crash. The gap for office and retail is a bit narrower at around 8%. Price expectations are closest for industrial warehouses, where sellers want just 2% more than buyers are willing to pay.

The market will be sluggish until one side caves. In the second quarter of 2023, investment in U.S. commercial real estate was down 64% compared with a year earlier, according to data from CBRE.

As the bid-ask gap narrows, it will signal that valuations are approaching more sustainable levels. But this will take some time. It was five years after the 2008 crash before buyers and sellers saw eye to eye on prices on the hardest-hit assets like apartments—although the adjustment should be much faster this time.

What Could Force Sellers to Slash Prices?

The number of properties that slip into distress will be key for bargain-hunters.

So far, there haven’t been many forced sales. Only 2.8% of all office deals in the U.S. in the second quarter were distressed, according to MSCI.

This may be because loans haven’t matured yet. “Owners don’t want to take a loss but once there are refinancing issues, they will have that come-to-Jesus moment with lenders,” says Jim Costello, chief economist at MSCI Real Assets.

Even if forced sales are still rare, the value of U.S. property in distress—in default or special servicing—is rising. In the second quarter, an additional $8 billion of assets got into distress, bringing the total to $71.8 billion, according to MSCI. Including properties that look at risk, the pool of potentially troubled assets is more than double this amount.

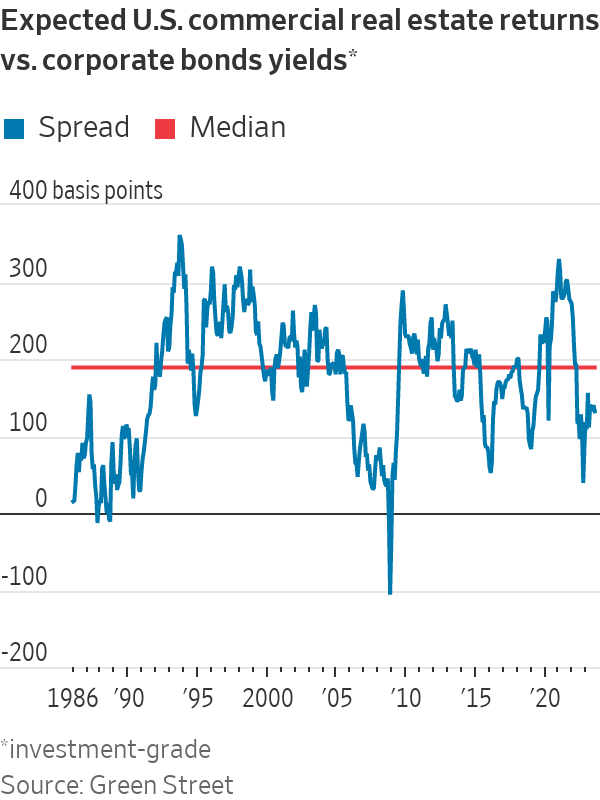

Investment-grade corporate bond yields suggest that property prices have further to fall

Owning commercial property is a bit like owning a corporate bond, only slightly riskier: You bet on the solvency of a tenant, with more uncertainty about the value of the capital you’ll get back. For at least the past 20 years, investors in U.S. real estate have required a return premium of 1.9 percentage points over the yield on investment-grade corporate debt, according to Green Street’s director of research, Cedrik Lachance.

Right now, real estate only offers a 1.3 percentage point premium. For the relationship to return to normal and make property attractive again, U.S. real-estate prices need to fall a further 10% to 15%.

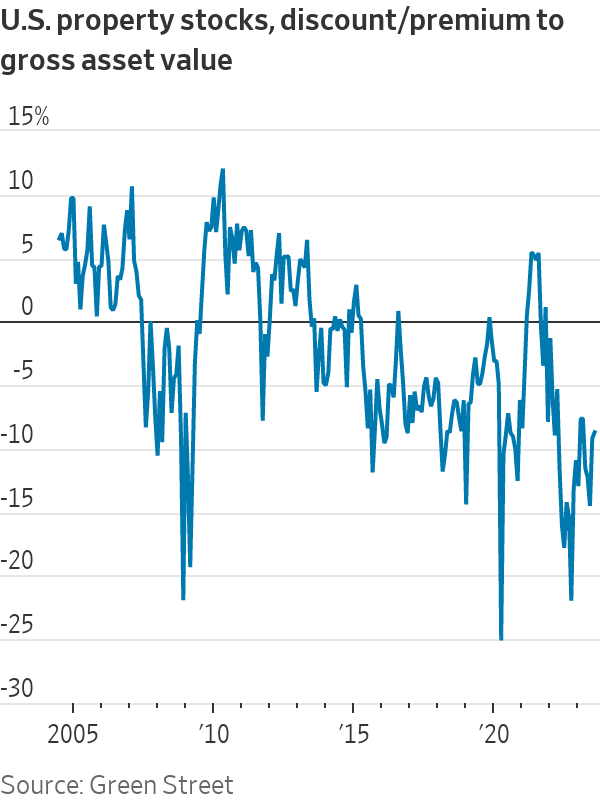

The share prices of listed property companies also point to further falls

Publicly traded real-estate stocks provide a live read of sentiment toward property markets. In the U.S., listed property companies currently trade at a 10% discount to gross asset values, based on Green Street data. This is a good proxy for the size of the price falls that investors still expect in private real-estate values.

Investors can also keep an eye on property stocks for signs of improvement. “Listed real estate is a leading indicator for private in downturns and also recoveries,” says Rich Hill, head of real estate strategy and research at Cohen & Steers, who points out that there are already green shoots. At the end of June, REITs had risen in value for three consecutive quarters and were 13% above their lowest point in the third quarter of last year. Based on how long it usually takes for a recovery to feed through to the private market, property values could hit the bottom within six to 12 months.

All this suggests the best strategy is to buy property stocks but to wait to purchase physical real estate. “If you want to bottom fish in real estate now, do it in the public markets,” says Green Street’s Lachance.

Australia’s vast and varied landscapes, combined with its unique climate conditions, mean that choosing the right paint is essential. Whether you’re painting an inner city home, a coastal retreat, or a bushland hideaway, your choice of paint needs to stand up to the elements. In this article, we will explore some of the best paints available in Australia for 2023 based on durability, finish quality, environmental considerations, and value for money.

Painting a home involves so many decisions, and choosing the right paint for the right job is tricky. Here we look at the top paint brands for the jobs at hand.

Taubmans All Weather

Exterior paints need strength to withstand the elements, they do this by adding additional and expensive, top quality resins so fading is less of an issue, and new technology that offers UV protection. Who wants to repaint a house, right? After years of advancement, you can now achieve great results with acrylic exterior paint, which has the primer built in. Taubmans All Weather and Taubmans Sun Proof are great options here.

Norglass

Exterior features such as fences and front doors are a chance to add extra zing to the design, and very often the best way to produce that effect is with a gloss or enamel paint. While there have been improvements in acrylic gloss products, purists and pros are still reaching for the oil based product – the finish is simply brighter and more reflective, and more to the point will last longer on high traffic spots such as doors. The lesser known Norglass brand offers a magnificent result, and comes in small cans, which is a bonus for feature trim jobs.

Dulux Wash and Wear

Interior walls cop the most passing traffic scuff and grime, especially if you are blessed with kids or pets. The ideal paint here is a washable, acrylic based paint that goes on smoothly, and wipes clean easily. A combination of huge colour range, and great coverage (meaning less coats to put on) is the Dulux Wash and Wear brand. You can actually feel the extra weight on the brush or roller, which is a good thing, but tougher on older hands, or newbies to the roller game.

British Paints Paint and Prime

Kate from @roadtorenovation // British Paints Australia

Getting on top of ceilings is perhaps the most difficult of paint jobs; back breaking and neck stretching, it is a job with little pay off – but is critical to achieve a perfectly finished room. A dead matte finish is ideal, usually in white (but don’t let that stop you from playing with colour), and always acrylic. While you can use a cheaper matte paint, a purpose designed one will go on easier and offer better coverage – it’s designed to be a one stop wonder. British Paints Paint and Prime is reputed to have be a good ceiling paint that goes on thickly, and works particularly well with a long nap roller, reducing spray.

Berger Paints

Houses have damp zones, and yes they need extra care because paint that doesn’t deflect the wet will get mould, mildew and then peel. The elasticity of acrylic paint is great here, and Berger Paints have a product, Kitchen and Bathroom Everlast which offers a five-year guarantee against mould and mildew. Best tip here is to steer clear of a matte ceiling paint, but the soft or lo sheen bathroom paint.

Haymes

A secret of professional painters is the top paint brand Haymes. Haymes is perhaps a lesser known brand to the home decorator but it has been rated by Canstar as the top paint in Australia for the last six years. Haymes has been produced by the one family in Australia for generations, and commands respect from those who spend their lives up a ladder. They don’t need expensive ad campaigns, because those in the know don’t need reminding of this solid and impressive brand. Always consider checking out their products when starting a project.

Environmental Considerations

As environmental awareness grows, many Australians are seeking eco-friendly paint options. Look for paints labeled as low VOC or zero VOC. These paints emit fewer chemicals, making them healthier for the environment and for the inhabitants of the painted space. Brands like Haymes and Porter’s have taken commendable steps in this direction.

Choosing the Right Paint

Remember, the best paint for your project depends on the specific requirements of the job:

Surfaces: Different paints are formulated for different surfaces such as wood, brick, or metal.

Location: Consider the specific climatic challenges of your region. Coastal homes might need salt-resistant paints, while homes in tropical areas might benefit from mould-resistant options.

Finish: Decide if you want a matte, semi-gloss, or gloss finish. This can affect the look and feel of the space as well as the paint’s durability.

Australia has a broad range of paints tailored to its unique environments. From the intense sun to the coastal breeze, our selection of paints have been tried, tested, and emerged as top picks for 2023. Remember to consider the specific needs of your project and, when in doubt, consult with a local professional for guidance.

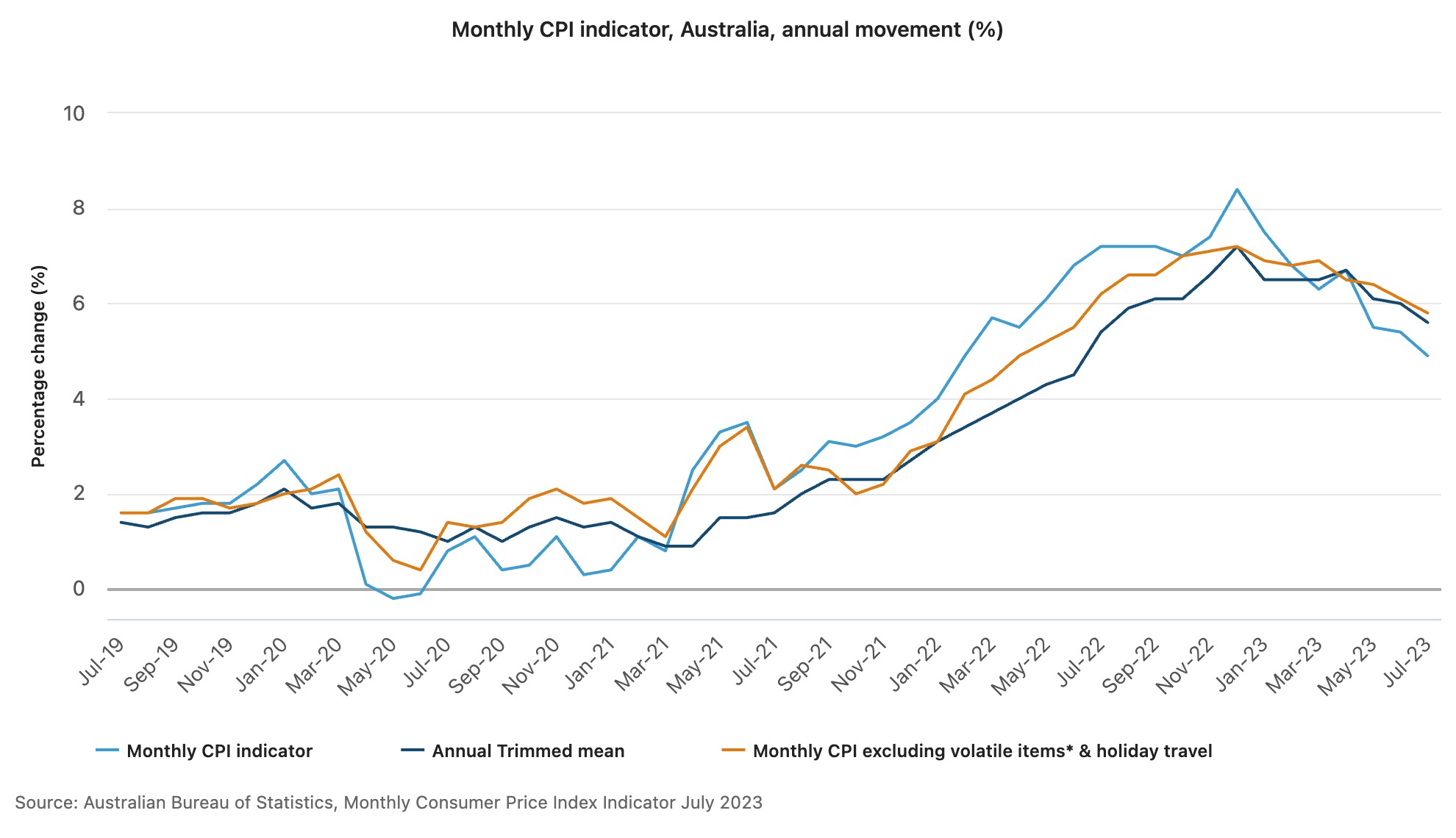

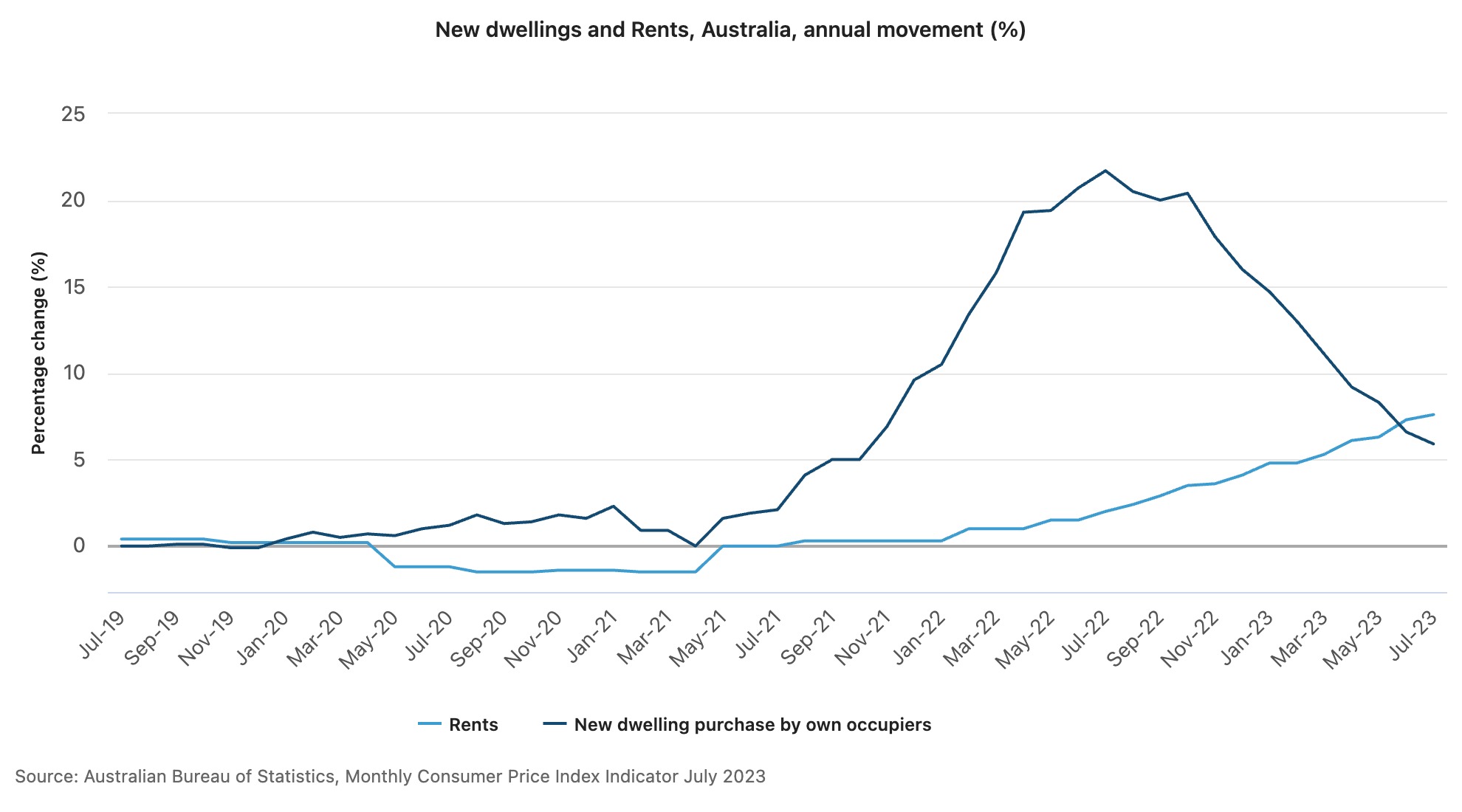

Further interest rate hikes may well be at an end with news that the inflation rate has fallen to its lowest levels in 17 months.

New data from the Australian Bureau of Statistics released today shows the consumer price index (CPI) for July came in at 4.9 percent seasonally adjusted, down from 5.4 percent in June. Markets had widely forecast a CPI of 5.2 percent.

Housing accounted for the most significant rise, up 7.3 percent, followed by food and non-alcoholic beverages, which increased by 5.6 percent. At the other end of the spectrum, the price of automotive fuel fell by -7.6 percent.

While the fall in the rate of inflation rate is good news for borrowers as the RBA approaches its monthly board meeting next week, there was further news for the property market, with the price of new dwellings rising by 5.9 percent, the lowest annual rise since October 2021.

However, rental demand remains strong, with rent prices up 7.6 percent in the 12 months to July 2023.

The RBA expects inflation to reach a more manageable 2-3 percent range by mid 2025.

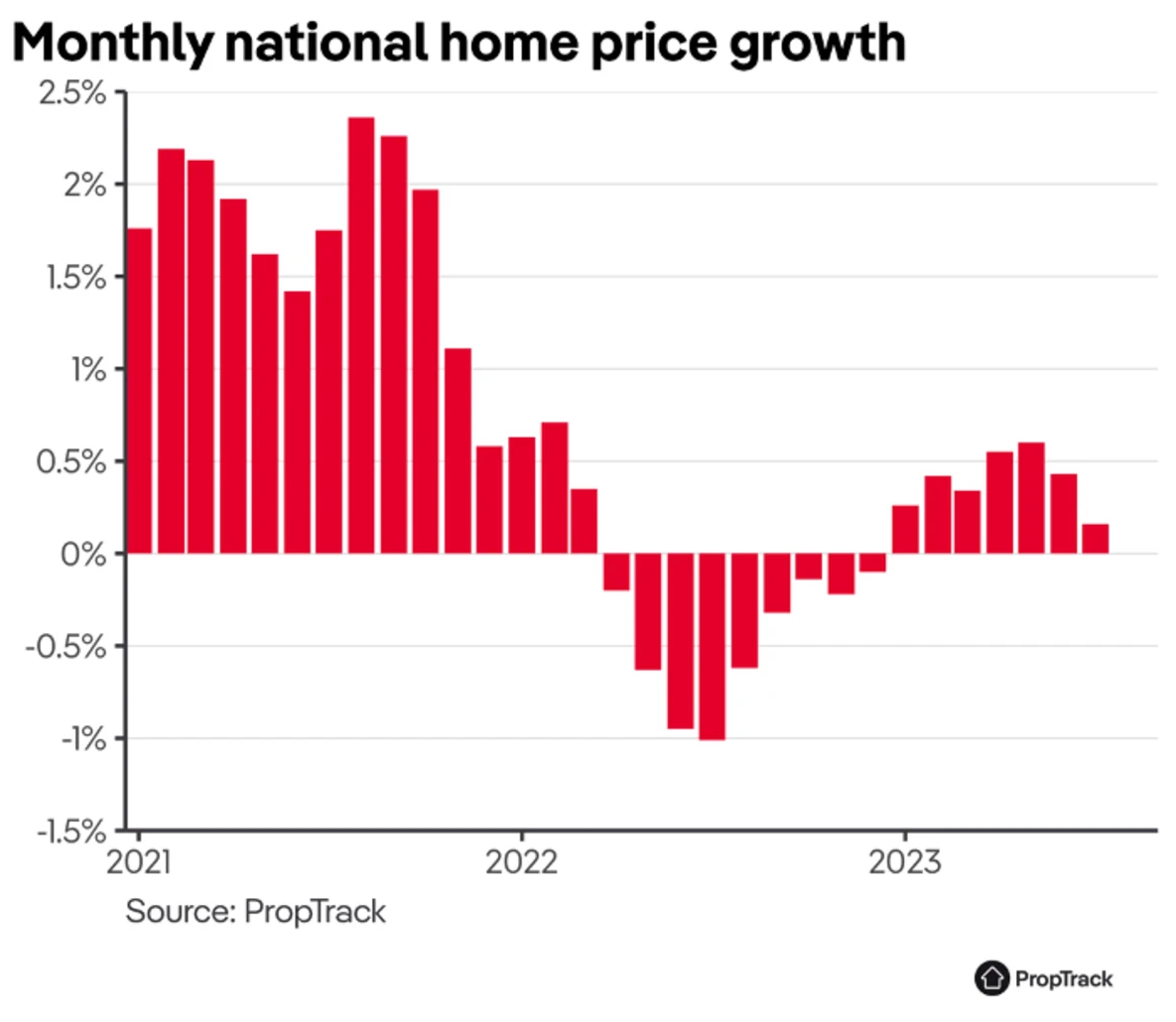

The number of new for-sale listings has been stubbornly sluggish for much of the year, but there are growing signs would-be vendors are finally feeling confident to go to market.

New analysis indicates this surge in supply is likely to put the brakes on a renewed boom in property prices being seen across much of the country.

According to data from research firm CoreLogic, national home values rose 2.9 percent in the three months to July – the highest quarterly movement since January.

Across the capital cities, values were up 0.8 percent last month – down slightly from a 1.2 percent lift seen in June.

Prices are rising fastest in Sydney, with a whopping 4.5 percent jump in the three months to July.

Prices rose 4.2 percent in Brisbane in the quarter, while Adelaide and Perth each recorded a 3.2 per cent increase. Values in Melbourne were up two per cent.

“Home values are down 3.4 percent annually, but declines are quickly subsiding from an eight per cent drop in the year to March,” Eliza Owen, head of residential research at CoreLogic, observed.

Data shows the number of new listings nationally hit 33,616 in the four weeks to 30 July, trending slightly higher through the month, which she noted is unusual for this time of year.

“The flow of new listings added to the market has been rising since mid-June, in contrast to the usual seasonal trend where new vendor activity would be trending lower through the colder months.”

With more homes hitting the market ahead of the traditionally busy spring selling season, Paul Ryan, economist at data house PropTrack, said price growth could dampen in the months ahead.

“There have been some tentative signs that sellers are responding to continued strong buyer demand and higher prices by bringing more listings to market,” Mr Ryan said.

PropTrack modelling shows a low level of new listings could be responsible for as much as a quarter of the price growth seen this year, and the impact of low supply can be felt within a few months.

“This analysis suggests that a stronger flow of listings could weigh on home price growth later this year as the market gears up for the spring selling season,” Mr Ryan said.

“And importantly, it shows the impact on prices is likely to be felt quite quickly after any new listings are brought to market – within one to two months.”

Mr Ryan said property markets have “displayed a remarkable turnaround in 2023”.

“Home prices fell persistently over 2022, down 4.1 percent from April to December, during the sharpest episode of interest rate increases ever implemented by the Reserve Bank,” he said.

“But 2023 has seen national home prices increase each month, up 2.8 percent so far this year, despite continued increases in interest rates.”

One major factor for the rapid turnaround in price movements is the low supply of new listings hitting the market, he said. Buyer demand has remained strong.

“The flow of new listings over the first half of 2023 was around 15 percent below the level seen over the same period in 2022, which represents a significant decrease.

“By contrast, the total number of homes on the market has mostly drifted upward as homes take longer to sell compared to the strong market conditions in 2021.”

BERLIN—Two decades ago, Germany revived its moribund economy and became a manufacturing powerhouse of an era of globalization.

Times changed. Germany didn’t keep up. Now Europe’s biggest economy has to reinvent itself again. But its fractured political class is struggling to find answers to a dizzying conjunction of long-term headaches and short-term crises, leading to a growing sense of malaise.

Germany will be the world’s only major economy to contract in 2023, with even sanctioned Russia experiencing growth, according to the International Monetary Fund.

Germany’s reliance on manufacturing and world trade has made it particularly vulnerable to recent global turbulence: supply-chain disruptions during the Covid-19 pandemic, surging energy prices after Russia invaded Ukraine, and the rise in inflation and interest rates that have led to a global slowdown.

At Germany’s biggest carmaker Volkswagen, top executives shared a dire assessment on an internal conference call in July, according to people familiar with the event. Exploding costs, falling demand and new rivals such as Tesla and Chinese electric-car makers are making for a “perfect storm,” a divisional chief told his colleagues, adding: “The roof is on fire.”

The problems aren’t new. Germany’s manufacturing output and its gross domestic product have stagnated since 2018, suggesting that its long-successful model has lost its mojo.

China was for years a major driver of Germany’s export boom. A rapidly industrialising China bought up all the capital goods that Germany could make. But China’s investment-heavy growth model has been approaching its limits for years. Growth and demand for imports have faltered.

Instead of Germany’s best customers, Chinese industries have become aggressive competitors. Upstart Chinese carmakers are competing with German incumbents such as VW that are lagging in the electric-vehicle revolution.

More broadly, the world has become less favourable to the kind of open trade that benefited Germany. The shift was expressed most clearly in then-President Donald Trump imposing tariffs not only on imports from China but also those of U.S. allies in Europe. The U.K.’s 2016 decision to leave the European Union and Russia’s annexation of Crimea in 2014, leading to EU sanctions, also signaled a shift toward a more hostile environment for big exporters.

Germany’s long industrial boom led to complacency about its domestic weaknesses, from an ageing labor force to sclerotic services sectors and mounting bureaucracy. The country was doing better at supporting old industries such as cars, machinery and chemicals than at fostering new ones, such as digital technology. Germany’s only major software company, SAP, was founded in 1975.

Years of skimping on public investment have led to fraying infrastructure, an increasingly mediocre education system and poor high-speed internet and mobile-phone connectivity compared with other advanced economies.

Germany’s once-efficient trains have become a byword for lateness. The public administration’s continued reliance on fax machines became a national joke. Even the national soccer teams are being routinely beaten.

“We’ve kind of slept through a decade or so of challenges,” said Moritz Schularick, president of the Kiel Institute for the World Economy.

In March, one of Germany’s most storied companies, multinational industrial-gas group Linde, delisted from the Frankfurt Stock Exchange in favor of maintaining a sole listing on the New York Stock Exchange. The decision was driven in part by the growing burden of financial regulation in Germany. But also, Linde, whose roots go back to 1879, said it no longer wanted to be perceived just as German—an association that it believed was depressing its appeal to investors.

Germany today is in the midst of another cycle of success, stagnation and pressure for reforms, said Josef Joffe, a longtime newspaper publisher and a fellow at Stanford University.

“Germany will bounce back, but it suffers from two longer-term ailments: above all its failure to transform an old-industry system into a knowledge economy, and an irrational energy policy,” Joffe said.

“I think it’s important to remember that Germany is still a global leader,” German Finance Minister Christian Lindner said in an interview. “We’re the world’s fourth-largest economy. We have the economic know-how and I’m proud of our skilled workforce. But at the moment, we are not as competitive as we could be,” he said.

Germany still has many strengths. Its deep reservoir of technical and engineering know-how and its specialty in capital goods still put it in a position to profit from future growth in many emerging economies. Its labor-market reforms have greatly improved the share of the population that has a job. The national debt is lower than that of most of its peers and financial markets view its bonds as among the world’s safest assets.

The country’s challenges now are less severe than they were in the 1990s, after German reunification, said Holger Schmieding, economist at Berenberg Bank in Hamburg.

Back then, Germany was struggling with the massive costs of integrating the former Communist east. Rising global competition and rigid labor laws were contributing to high unemployment. Spending on social benefits ballooned. Too many people depended on welfare, while too few workers paid for it. German reliance on manufacturing was seen as old-fashioned at a time when other countries were betting on e-commerce and financial services.

After a period of national angst, then-Chancellor Gerhard Schröder pared back welfare entitlements, deregulated parts of the labor market and pressured the unemployed to take available jobs. The controversial reforms split Schröder’s Social Democrats, and he fell from power.

Private-sector changes were as important as government measures. German companies cooperated with employees to make working practices more flexible. Unions agreed to forgo pay raises in return for keeping factories and jobs in Germany.

Germany Inc. grew leaner. Meanwhile, the world was demanding more of what Germans were good at making, including capital goods and luxury cars.

China’s sweeping investments in industrial capacity powered the sales of machine-tool makers in Bavaria and Baden-Württemberg. VW invested heavily in China, tapping newly affluent consumers’ appetite for German cars.

Schröder’s successor, longtime Chancellor Angela Merkel, presided over years of growth with little pressure for further unpopular overhauls. Booming exports to developing countries helped Germany bounce back from the 2008 global financial crisis better than many other Western countries.

Complacency crept in. Service sectors, which made up the bulk of gross domestic product and jobs, were less dynamic than export-oriented manufacturers. Wage restraint sapped consumer demand. German companies saved rather than invested much of their profits.

Successful exporters became reluctant to change. German suppliers of automotive components were so confident of their strength that many dismissed warnings that electric vehicles would soon challenge the internal combustion engine. After failing to invest in batteries and other technology for new-generation cars, many now find themselves overtaken by Chinese upstarts.

A recent study by PwC found that German auto suppliers, partly through reluctance to change, have suffered a loss of global market share since 2019 as big as their gains in the previous two decades.

More German businesses are complaining of the growing density of red tape.

BioNTech, a lauded biotech firm that developed the Covid-19 vaccine produced in partnership with Pfizer, recently decided to move some research and clinical-trial activities to the U.K. because of Germany’s restrictive rules on data protection.

German privacy laws made it impossible to run key studies for cancer cures, BioNTech’s co-founder Ugur Sahin said recently. German approvals processes for new treatments, which were accelerated during the pandemic, have reverted to their sluggish pace, he said.

Germany ought to be among the nations winning from advances in medical science, said Hans Georg Näder, chairman of Ottobock, a leading maker of high-tech artificial limbs. Instead, operating in Germany is getting evermore difficult thanks to new regulations, he said.

One recent law required all German manufacturers to vouch for the environment, legal and ethical credentials of every component’s supplier, requiring even smaller companies to perform due diligence on many foreign firms, often based overseas, such as in China.

Näder said his company must now scrutinise thousands of business partners, from software developers to makers of tiny metal screws, to comply with regulation. Ottobock decided to open its latest factory in Bulgaria instead of Germany.

Energy costs are posing an existential challenge to sectors such as chemicals. Russia’s war on Ukraine has exposed Germany’s costly bet on Russian gas to help fill a gap left by the decision to shut down nuclear power plants.

German politicians dismissed warnings that Russian President Vladimir Putin used gas for geopolitical leverage, saying Moscow had always been a reliable supplier. After Putin invaded Ukraine, he throttled gas deliveries to Germany in an attempt to deter European support for Kyiv.

Energy prices in Europe have declined from last year’s peak as EU countries scrambled to replace Russian gas, but German industry still faces higher costs than competitors in the U.S. and Asia.

German executives’ other complaints include a lack of skilled workers, complex immigration rules that make it hard to bring qualified workers from abroad and spotty telecommunications and digital infrastructure.

“Our home market fills us with more and more concern,” Martin Brudermüller, chief executive of chemicals giant BASF, said at his annual shareholders’ meeting in April. “Profitability is no longer anywhere near where it should be,” he said.

One problem Germany can’t fix quickly is demographics. A shrinking labor force has left an estimated two million jobs unfilled. Some 43% of German businesses are struggling to find workers, with the average time for hiring someone approaching six months.

Germany’s fragmented political landscape makes it harder to enact far-reaching changes like the country did 20 years ago. In common with much of Europe, established centre-right and centre-left parties have lost their electoral dominance. The number of parties in Germany’s parliament has risen steadily.

Chancellor Olaf Scholz and his Social Democrats lead an unwieldy governing coalition whose members often have diametrically opposed views on the way forward. The Free Democrats want to cut taxes, while the Greens would like to raise them. Left-leaning ministers want to greatly raise public investment spending, financed by borrowing if needed, but finance chief Lindner rejects that. “We need fiscal prudence,” Lindner said.

Senior government members accept the need to cut red tape, as well as for an overhaul of Germany’s energy supply and infrastructure. But party differences often hold up even modest changes. This month the Greens lifted a veto of Lindner’s proposal to reduce business taxes only after they extracted consent for more welfare spending. As part of the deal, the government agreed to pass another law drafted by one of Lindner’s allies, Justice Minister Marco Buschmann, to trim regulation for businesses.

Scholz recently rejected gloomy predictions about Germany. Changes are needed but not a fundamental overhaul of the export-led model that has served Germany well throughout the post-World War II era, he said in an interview on national TV recently.

He cited the inflow of foreign investment into the microchips sector by companies such as Intel, helped by generous government subsidies. Scholz said planned changes to immigration rules, including making it easier to qualify for German citizenship, would help attract more skilled workers.

But Scholz has struggled to stop the infighting in his coalition. The government’s approval ratings have tanked, and the far-right populist Alternative for Germany party has overtaken Scholz’s Social Democrats in opinion polls.

“The country is being led by a bunch of Keystone Kops, a motley coalition that can’t get its act together,” Joffe said.

A year after the Inflation Reduction Act (IRA) was signed into law it’s a good reminder that there’s opportunity in infrastructure investments in the U.S., particularly green technology or those that profit from the transition from fossil fuels to renewable-energy sources.

“This is a really good time to be investing in the sector,” says Michael McGown, head of North American infrastructure private markets at Mercer Alternatives. “There is a real need to transition away from carbon, and the fact that the U.S. government has gotten behind this makes it a win.”

Yes, there is some political pushback against the law—and there are still those who want to rely on fossil fuels and other traditional forms of energy production. But many experts point to the IRA’s transformative potential, and its impact on energy-transition spending in particular, as a good opportunity for savvy investors.

“I don’t think in my career I’ve ever seen a law have a greater impact on economic development in this country,” Gregory Wetstone, chief executive officer of the American Council on Renewable Energy, a clean energy lobbying group, said in July.

Wall Street agrees. Calling themselves “positive” on greentech opportunities, analysts at UBS wrote in July that they forecast US$40 trillion to US$50 trillion of global energy-transition investments in the years 2021–30, in support of net-zero efforts.

“We also expect to see technological developments and a broad-based move to global electrified vehicles (i.e., battery-electric vehicles and plug-in hybrid electric vehicles),” the UBS team wrote in a note. “Such sales may account for a 30% share of the global market by 2025 and a 60%–70% share by 2030, in our view.”

Within the category of energy transition, there are some infrastructure themes that may appeal more than others, either because of their promise of innovation or potential monetary returns.

Mercer’s McGowan points to investments in carbon reduction and abatement, those dedicated to decommissioning old power plants to replace them with renewable or hybrid technologies, and investing in ammonia, which is often used to transport clean hydrogen.

More cutting-edge technologies are likely to offer investors better total returns, says Steven Novakovic, director of curriculum for the Chartered Alternative Investment Analyst Association. In contrast, the more mature, stable, user-fee oriented investments are less return-oriented, but better bets for income investors.

“Generating, moving, or storing energy tends to be income-oriented,” Novakovic says.

Importantly, even though energy infrastructure may be capital-intensive, higher and rising interest rates aren’t likely to be a negative for the sector.

“High barriers to entry and the monopolistic positioning of many infrastructure assets tend to make them less sensitive to the economic cycle,” the UBS analysts said. “In addition, they can help stabilise income generation in a multi-asset class portfolio, particularly when accounting for long-term inflation. Since 2003, infrastructure has typically performed best when global inflation has been high (based on Cambridge Associates Infrastructure Index data).”

With interest rates higher across the board, some investors may simply choose to stick with safer fixed-income assets, Novakovic says. But, he says, “Ultimately infrastructure still has a diversifying effect for portfolios.”

Where to Invest

What are the best ways for investors to access the sector? Qualified investors, or those with at least a few million to spend, can put money directly into private-market plays, such as private-equity funds or even venture-capital funds, which are likely to pay the most in total returns.

There are, of course, typical concerns with private-market strategies, the UBS team said: “illiquidity, longer lockup periods, leverage, concentration risks, and limited control and transparency of underlying holdings. While risks can’t be fully eliminated, it is possible to mitigate them through strong due diligence and strict manager selection.”

They add a shout-out for global industrial stocks, writing that the “sector’s composition has become increasingly diversified and no longer behaves like a traditional cyclical play, in our view.”

In a July note to clients, J.P. Morgan Private Bank analysts wrote about the opportunities in the semiconductor industry driven by the IRA in addition to last year’s CHIPS and Science Act. Semiconductors, for instance, can be used in the process of decarbonisation, particularly for powering “smart” electric grids and other forms of infrastructure

“The semiconductor industry is poised for growth as chips penetrate the clean energy value chain: in photovoltaic solar cells, wind turbines, EVs, batteries, charging stations, and power grids,” the note said.

CHIPS alone allocates more than US$50 billion to subsidise domestic manufacturing of advanced semiconductors. “These government incentives, combined with the wide variety of uses for semiconductors, have pushed companies to ramp up supply,” J.P. Morgan said.

For investors who want to access a basket of energy-transition stocks, several exchange-traded funds may fit the bill. The Global X Lithium & Battery Tech ETF (ticker: LIT) “invests in the full lithium cycle, from mining and refining the metal, through battery production,” according to fund documents, while the Sprott Energy Transition Materials ETF (SETM) says it, “provides pure-play access to a range of critical minerals necessary for the global clean-energy transition.”

And for those who prefer bonds, or just want a more tax-efficient strategy, many municipalities are also issuing debt to fund cleaner energy. In June, the California Community Choice Financing Authority sold nearly US$1 billion in bonds to finance the acquisition of clean energy—including geothermal and solar-plus-storage—by the Clean Power Alliance of Southern California. The projects could affect as many as 3 million residents.

After strong yields in recent years, rent growth is set to slow across Australia next year, according to new data.

Research by property data and analytics provider CoreLogic shows after 35 consecutive increases in rent values to July this year, they have begun to slow in recent months.

The trend is most obvious in regional areas where rent values have been slowing since April last year and appear to have flattened out. In regional Tasmania, where data from 40 suburbs was analysed, rents have fallen by 47.5 percent. This was followed by regional NSW, where of the 353 suburbs analysed, 38.4 percent have recorded a decrease in rents. However, data shows the capitals have also been impacted, with more than 90 percent of Hobart suburbs recording a fall in rent over the past quarter, followed by Canberra at 88.9 percent. In Sydney’s suburbs, there’s a strong contrast between rent values for houses and apartments, with the former recording a fall of 19 percent, while apartment rent values fell just 6.9 percent.

CoreLogic Australia head of research Eliza Owen said there were several factors at play signalling that the trend would continue into 2024. A predicted decline in interest rates could encourage more investors into the market, leading to an increase in the rental supply and therefore lower rent growth. More first homebuyers might also be ready to enter the property market as confidence around the cash rate grows.

Slowing income growth, which was strong during the pandemic, could also lead some renters to reassess their decision to move into more spacious single households and back into more affordable share house options, freeing up more rental stock.

Apartments continue to represent the best yield compared with houses for investors, with significantly lower falls in rents in all Australian capitals, with the exception of Canberra and Hobart where they are in par with corresponding falls in rents for houses.

Workers are waking up to emails and team-meeting requests with a jarring message: They aren’t fired, but their jobs are gone.

People on the receiving end of these memos describe running through a range of emotions, from relief that they’re still employed to a sense of dread that their bosses secretly want them to leave. They are also facing a labor market that isn’t as robust as a year ago, leaving many to believe that the best option is to stay put and hunt internally for a better fit.

Adidas, Adobe, IBM and Salesforce, among others, have reassigned employees as part of corporate restructurings. Mentions of reassignment, or similar terms, during company earnings calls more than tripled between last August and this month, according to data from AlphaSense, a financial-research platform.

“Reassigning is definitely a huge part of the dynamic right now,” said Andy Challenger, senior vice president at Challenger, Gray & Christmas, an outplacement firm.

For companies that spent several years—and significant money—to hire top talent, reassigning workers to new roles can be a way to fill jobs vital to future plans while trimming costs associated with old strategies, say human-resources executives.

It can also be a waiting game. Employees to whom it would be costly to pay severance or months of unemployment benefits might decide to leave on their own if they feel stuck in a job they don’t want, executive coaches say.

U.S.-based companies announced 42% fewer job cuts in July than they did in June, Challenger said. July job cuts were also 8% lower than the prior-year period, marking the first time this year that monthly job cuts were lower than in 2022.

In interviews and online forums, many workers said they worried whether their reassignment meant they would eventually be pushed out the door. They also wondered how to work their way out of job purgatory and back into a position they actually want.

“I got the sense that it was like: ‘We appreciate everything you did so we didn’t lay you off, so you can either make the best of this or go find another job somewhere else,’ ” said Matt Conrad, a 34-year-old senior sales-enablement specialist at IBM who went through two reassignments in two years before landing his current role last fall.

In Conrad’s first reassignment in 2021, a manager scheduled a call to notify him that his manager role was eliminated. He was given a new job selling software he had no experience with, a move he said took a toll on his mental health.

Later that year, Conrad found a new job at IBM through a former manager that was better suited to his skill set. Then, in January 2022, that team was eliminated and he was reassigned again. Conrad asked the HR department to help him to find his remote, senior sales-coach role, a process that took six months.

Not quitting when he was reassigned was a matter of principle, he said: “I wouldn’t give in because I was a top performer and it just wasn’t fair.”

IBM didn’t respond to requests for comment.

Getting caught up in a reorganisation can create anxiety for workers, but it’s sometimes a genuine move on the company’s part to avoid letting people go, said Roberta Matuson, an executive coach and adviser to businesses including General Motors and Microsoft on human-resources issues.

“They’re basically signalling to you: ‘Look, this is the only way for me to have a job here for you, I need to reassign you, so wink, wink, if I were you, I would take the assignment,’ ” she said.

Other times, workers are purposefully pushed into jobs management knows they will be miserable in, prompting them to quit.

“They could be putting you out to pasture,” Matuson said.

Signals to look for include reassignment to a job that is far below the pay or skill level you currently have, Matuson said. Other warning signs: Being offered a role that requires relocating when your boss knows moving isn’t a viable option for you, or being reassigned to a division that’s rumoured to be on the chopping block.

Employees suspicious or nervous about a reassignment should ask their managers why, specifically, it’s happening and what the reassignment means for their career path, said Naomi Sutherland, a global lead of talent development with Korn Ferry, a consulting firm. The answers could reveal whether a job transfer is personal.

Without good information, “people are going to fill a void of information with whatever story they’re going to tell themselves,” she said.

Most of the time, there is little legal recourse for workers if their company reassigns them, employment lawyers say.

One exception is when a worker can demonstrate the reassignment was retaliatory, said Angela L. Walker, an employment attorney with Blanchard & Walker in Ann Arbor, Mich. The bar is high, she added. The employee would have to show prior evidence of discriminatory treatment or that they were unfairly singled out.

“I’ve seen lots of examples in my practice where employees are told they’re being let go in a ‘restructuring’ and it turns out that they’re the only one affected, or they’re the only one affected in their group,” Walker said.

Grant Gurewitz, 32, said it took time to adjust to a new role in Seattle earlier this year when his software company eliminated his position as head of growth marketing for employee experience in North America. He was given 24 hours to make a choice between two other jobs, or leave. He picked a global head of growth marketing role that came with more responsibilities but without a pay increase.

He chose to look on the bright side, because a global role probably would’ve been the next position he wanted and it builds on his existing skill set.

“There’s still a lot of runway for me to learn and grow and develop in this role, which is the glass-half-full approach to all of this that’s happened,” he said.

An eco-chic oasis in Bali, Indonesia, is up for auction and will sell to the highest bidder with no reserve.

Spanning more than 15,000 square feet, the turnkey nature-lover’s estate, known as Villa Krtajna is in Canggu, a resort village on the south coast of the island that’s surrounded by terraced rice paddies and known for its surf beaches.

Consisting of a primary residence and a separate loft, the property—currently on the sales market with a $1.95 million asking price—has a total of six bedrooms and nine full bathrooms.

The Concierge Auctions sale, in cooperation with Vivi Aprilia of OXO Group Indonesia, opened up to bids this week and will run until the hammer falls on Sept. 7.

Built with polished concrete, aluminium and recycled antique teak, the biophilic spread “embodies a fusion of nature and sustainable living, designed to enhance well-being and create a healthier environment,” the listing said.

No artificial colours can be found across the home, making for an organic palette of soft greys and warm browns from the concrete and wood construction.

Inside, a wooden walkway over a shallow pool in a double-height foyer leads into the home where walls of glass open up much of the property to the outdoors. There’s a sun-filled and open-plan living, kitchen and dining space, and a floating wooden staircase leads upstairs, where there’s the primary suite, two offices and a roof garden.

“Overall, this home prioritises sustainability, a connection to nature and utmost wellness for its future owners,” the listing said.

One of those priorities is underlined by the spa, which is fitted with a steam room, a cold plunge and a multipurpose sound dome, to be used for meditation, sound therapy or a massage space.

The semi-detached two-bedroom loft house has a pool and a sun deck and can be used for extra space or to provide a source of income.

The home also boasts a host of green-approved amenities, including a solar-powered energy system, a water treatment plant for pure drinking water, a rainwater harvesting system and low-chemical pools.

Mansion Global couldn’t determine the owner of the home.

Demand for new homes is surging after a lacklustre year – and one property type is proving particularly popular among would-be buyers.

The latest New Homes Report from research firm PropTrack shows a 16 per cent increase year-on-year in search enquiries for new developments on realestate.com.au in July.

Boutique luxury apartments are especially in-demand, data shows. Enquiries for unit projects in inner Melbourne are the highest in the country.

The Victorian capital accounts for 34 per cent of all current residential construction projects in the country, with most underway in the inner-city.

Enquiries are the second highest on the Gold Coast, home to nine per cent of all current apartment developments.

Adelaide’s central and Hills regions have the most enquiries per development, but the number of projects underway in the city are particularly low, meaning more would-be buyers for fewer listings.

Analysis of demand shows premium unit complexes with rooftop swimming pools, wine rooms and gums are popular.

In July, Elysian Residences in Sherwood in Brisbane’s inner-south saw the most enquiries, followed closely by Murcia in Wollongabba in the inner-city.

The Walmer project in Melbourne’s Abbotsford came in third for the most enquiries sent by property seekers on realestate.com.au.

The New Homes Report also reveals the pace of building cost increases has slowed over the past year, with prices stabilising as supply chain issues improve.

Input prices rose by 0.6 per cent in the June quarter, which is the lowest increase in 18 months, Australian Bureau of Statistics data shows.

The cost of certain essential building materials, like concrete and plumbing products, has risen. However, the extent of those increases has been offset considerably by a slump in steel prices.

It marks good news for the construction sector, which has struggled through a tough period of time.

PropTrack senior data analyst Karen Dellow said the development of new dwellings slowed significantly over the past few years.

“The pandemic caused supply chain issues, increasing the price of essential building materials, which increased building costs, while labour shortages have also been a growing problem,” Ms Dellow said.

Frequent construction site shutdowns during Covid-19 stalled work and slowed down new home completions, she added.

“As a result, the higher cost of new properties led to decreased demand, compared to its peak in September 2021, when the government’s HomeBuilder Grant drove many property seekers to build houses to take advantage of the government subsidy.

“The combination of labour shortages and increasing prices has led to a backlog of work impacting the approval and commencement of future developments.”

However, ABS data shows easing construction costs might be helping to get work out of planning phases and into production.

There was a 14 per cent increase in new commencements in the March quarter, the latest figures reveal, totalling 46,546 dwellings. That has been driven by a whopping 57 per cent increase in apartment and townhouse commencements.

The prime years for making smart financial decisions are, on average, 53 and 54.

At around that age, people have accumulated knowledge and experience about money, spending and saving, but haven’t begun losing key analytic cognitive skills. It’s also roughly the age when adults make the fewest financial mistakes, related to things like credit-card use, interest rates and fees.

Knowing what leads to the financial strength of your early 50s is valuable. Younger adults can delve more deeply into basics like inflation and interest rates to hedge against lack of experience, and those who are older can work to keep their analytical skills sharp.

“As we get older, we seem to rely more on past experience, rules of thumb, and intuitive knowledge about which products or strategies are better,” says Rafal Chomik, an economist in Australia at the ARC Centre of Excellence in Population Ageing Research.

Chomik led a 2022 study that looked at financial literacy, which is the ability to understand financial information and apply it to managing personal finances. Financial literacy typically peaks at age 54 and then declines, according to the study.

The study gauged financial literacy using questions about inflation, interest rates and diversification. One question: If in five years, your income has doubled and prices have doubled, will you be able to buy (A) less, (B) the same, (C) more than today. (Answer: B)

People can—and do—make good financial decisions from their 20s to their 40s, as well as into their 60s and 70s. Chomik, who is 45, says some of his best financial decisions came earlier in his life and involved his 401(k)-type savings account. Contributions were mandatory when he started his first job at around age 18, but once enrolled, he actively chose funds that benefit those who have a longer investment horizon.

Financial decision-making requires a combination of reasoning skills that differ by age. Those in their 20s are better at absorbing and processing new information and computing numbers—so-called fluid intelligence—but don’t have as much life experience or crystallised intelligence—the accumulation of facts and knowledge. Crystallised intelligence tends to improve with age.

Getting help

Beverly Miller, a financial coach who often works with people who are in debt, says she did most things right before her 50s, avoiding credit-card debt, paying off car loans and paying off a 30-year mortgage in 12 years.

But she didn’t invest as wisely as she could have. For example, she moved money in a retirement savings account out of growth funds and into fixed-income funds.

“We would let market changes scare us into making changes we shouldn’t have,” says Miller, 65.

Miller says she and her husband could have made more money if they had left it in growth funds. Likewise, she invested in rental properties, which she thought could be an easy source of income but weren’t.