TOKYO—Toyota thinks the world outside of Japan may finally be ready to embrace its six-figure superluxury flagship car.

Toyota’s Century—often described as the Rolls-Royce of Japanese cars—is a frequent choice of corporate chieftains and government leaders in Japan, including the emperor.

Since it made its debut in 1967, the Century has been sold almost exclusively in Japan and the model has changed little from its original boxy sedan shape and classic styling.

Toyota on Wednesday showed off a new, larger, plug-in hybrid version of the model that “from the start had its eye on the world,” Executive Vice President Hiroki Nakajima said, speaking at the unveiling event in Tokyo.

The new Century model will be introduced this year in Japan at a suggested retail price equivalent to around $170,000 and will be offered to customers in all regions of the world, Nakajima said. Toyota said select dealers in Japan would sell the model but didn’t describe sales procedures in other countries such as the U.S.

With its new Century, Toyota is targeting two segments—larger and luxury vehicles—that have continued to grow despite stagnation elsewhere in the car market. Until now, Toyota has primarily served the luxury market through its Lexus brand.

In 2022, global sport-utility vehicle sales grew 3% from the year earlier despite a slight decline in overall car shipments. That was due in part to strong demand for the vehicles in the U.S., India and Europe. Demand for luxury cars has also continued to rise through recent economic uncertainties.

One thing that won’t change is Toyota’s practice of having specially trained workers hand-make and customise the Century models in Japan. For now, Toyota said it wouldn’t produce more than 30 of the new Century models a month in addition to the existing sedan type it also continues to manufacture.

That means the new Century will likely have a bigger impact on Toyota’s brand image than its bottom line. Nakajima said the Century is a way to show off Toyota’s craftsmanship. He said details of overseas rollout plans would be determined based on initial reactions from customers.

Through the decades, Toyota’s Century has gained a following for being a decidedly Japanese take on a super luxury car. While little-known to most Toyota buyers in the U.S., it has attracted a following from some car enthusiasts such as comedian Jay Leno, who featured the model on a 2018 episode of his car-review series.

The vehicle’s grille features a badge inspired by the golden phoenix that adorns the Temple of the Golden Pavilion in Kyoto. The exit from the rear passenger cabin is lowered so that a person wearing a ceremonial kimono can easily get in and out.

It targets the Japanese upper crust who want to broadcast success, but not in a flashy way. The styling is boxy and understated, typically black with chrome accents.

When introducing the most recent iteration of the Century in 2018, Toyota said it had no plans to sell the vehicle outside of Japan because it didn’t think the car would appeal to foreigners.

The new models presented on stage Wednesday were a departure from the Century’s original styling—similar in shape to an SUV and showing a range of silver and gray shades.

Still, many of the Century’s interior features designed for chauffeured passengers remain. Those include rear seats that fully recline.

Chief Branding Officer Simon Humphries said the new Century was designed to maintain “the highest of Japanese sensibilities,” while also keeping in mind that customers are changing. The roomier new Century is designed for passengers who want to join online meetings from the back seat of their cars and drive without producing emissions, Toyota said.

“It’s a Century for the next century,” Humphries said.

Stop dwelling on what you’ve lost thanks to rising interest rates and take advantage of the opportunities they present.

High rates are expected to linger for a while and they are having a corrosive impact on some parts of our finances. Taking out a $500,000 mortgage to buy a home today will cost you about $400 more a month than it would have a year ago in a standard 30-year mortgage. That is not to mention higher rates on credit cards, personal loans and other products for borrowers.

The high-rate periods can also bring juicy, high yields on savings accounts, certificates of deposit and Treasury bills—that is, banks are paying you to let your money sit there. And anyone can take advantage, regardless of income.

Dena Bashri opened a SoFi savings account last fall. It now yields 4.5% a year. She wanted a higher return than she was getting at her local credit union.

Bashri, 25 years old, is a senior director at a fundraising firm and makes roughly $92,500 a year. She saves money on rent by living with her parents in Virginia so she’s able to contribute about $4,900 each month to her savings account. She’s already earned close to a few hundred dollars in interest and hopes to continue building her rainy-day fund, she said.

“Emergency savings offers me the flexibility to take risks but also financially anticipate any life changes that may happen,” Bashri said.

Here’s a financial road map for making the most of great yields while staying on track with your short- and long-term money goals.

Level 1: Nothing to spare

Living paycheck to paycheck is now the norm for most Americans.

Financial advisers urge those holding large amounts of debt to first pay down high-interest balances. About half of people carrying credit-card debt allow those balances to roll over into the next month, according to a recent Bankrate survey.

Credit-card interest rates are at record highs, making that debt even more expensive to maintain. Putting money in a savings account with a 4.5% rate will help little if you haven’t paid down your Visa balance with the current average rate of 22.16%.

“Although you may be able to set aside a certain amount of money in a savings account, if you’re potentially offsetting that with not paying off higher debt, that’s an important consumer consideration,” said Courtney Mitchell, head of consumer deposits, products and payments at TD Bank.

For avid debit-card users, high-yield checking accounts are worth consideration, financial advisers say. These accounts can be found at credit unions and online banks and are yielding up to 6%. That interest can then be linked to a high-yield savings account. This is a good option for debit-card users who want to get a start on their emergency fund.

But try not to keep more than one month’s worth of expenses sitting in a checking account, said Rob Williams, managing director of financial planning and wealth management at Charles Schwab. Research shows money sitting in a checking account is more likely to be spent than money in a savings account.

Level 2: $0—$1,000

For those who can sock away at least a little bit each month, even putting $25 in a high-yield account can make a difference, said Mitchell.

If you contribute $25 a month to a savings account yielding 4.5%, you will have roughly $300 in a year including interest.

Putting that money toward emergency savings? Liquidity is key so that when something unexpected happens, like a flat tire, you can get the money quickly. High-yield savings accounts are the best places for emergency savings because they allow easy withdrawals, financial advisers say.

“You really need emergency savings to be in something you can get at as soon as possible and also without a penalty,” said Mark Hamrik, senior economic analyst at Bankrate.

Financial advisers recommend building up six months to one year of expenses in an emergency-savings account. Homeowners should save a little more for unexpected repairs.

Level 3: $1,000+

Once you’re comfortable with your emergency savings, you can set aside money for holiday gifts, vacations and other short-term goals such as a down payment on a car.

The run of interest rate increases has made certificates of deposit popular again. If you are comfortable locking money away for a period of time, consider a CD for some of these short-term goals. Many six-month to one-year CDs are offering yields above 5%.

It can be helpful to divvy up your high-yield savings for coming expenses.

Erin Confortini, 24, is a freelance marketing consultant based in Pennsylvania who made about $120,000 last year. She has three high-yield savings accounts for her short-term savings goals.

Each month, Confortini puts $150 aside for car insurance, $300 for coming vacations and $200 toward Christmas and birthday gifts, she said.

“It’s really great that now that rates are increasing, we do have an option to earn a little bit of money,” Confortini said.

Level 4: Investing for long term

You’ve got at least one month of expenses in your checking account, you’ve beefed up emergency savings and you’ve set aside buckets of money for anticipated expenses.

Maybe it’s time to get more money out of high-yield savings. Keeping all of your money in savings isn’t a strategy for wealth building because the interest gained on high-yield accounts likely won’t outpace inflation in the long run, said Kyle McBrien, a certified financial planner at Betterment.

One simple way to take advantage of rates and get out of high-yield savings is Treasurys.

Take Victor Cipolla, a 33-year-old entrepreneur in New York.

Cipolla moved $30,000 from his high-yield savings account into a Treasury bill after he noticed that rates were going up. The bill currently yields more than 4% and he reinvests the money in another Treasury bill every six months when it matures, he said. The average yield on a six-month Treasury bill is 5.3%.

“We’ve always had this low interest rate environment, so this is a new area to navigate,” said Cipolla.

Ray White boss Dan White is forecasting a bumper spring selling season for Australia’s property market, after the real estate company wrote a staggering $6.9 billion in sales last month.

August’s stellar result was 14 percent higher than the same month last year and only four percent down on 2021 when record home price growth was seen.

“Our August sales results officially certified the renewed and broad-based resurgence in the residential market that we have been seeing since late May,” Mr White said.

Dan White, managing director at Ray White

May was when Ray White saw a small “but identifiable” lift in new listings coming to market, particularly in the eastern states, he said.

“This was very unusual as new listings normally drop in the winter months. Interest rates were still rising, and given that the expectation was for an increasingly depressed market, was this a blip? But the trend became firmer in June, and stronger again in July.”

Ray White Group listed 10,500 homes in August, up 12 percent on last year and more than 20 percent higher than 2021.

And Mr White revealed the company’s pre-listing data shows a “strong” flow of more listings in the next few weeks.

“Buyers, including potential sellers that intend to repurchase, now have a lot more property to choose from. The market is very well-stocked for spring.”

Despite an increase in supply, buyer demand remains elevated across much of the country, meaning prices are likely to continue rising in the months ahead.

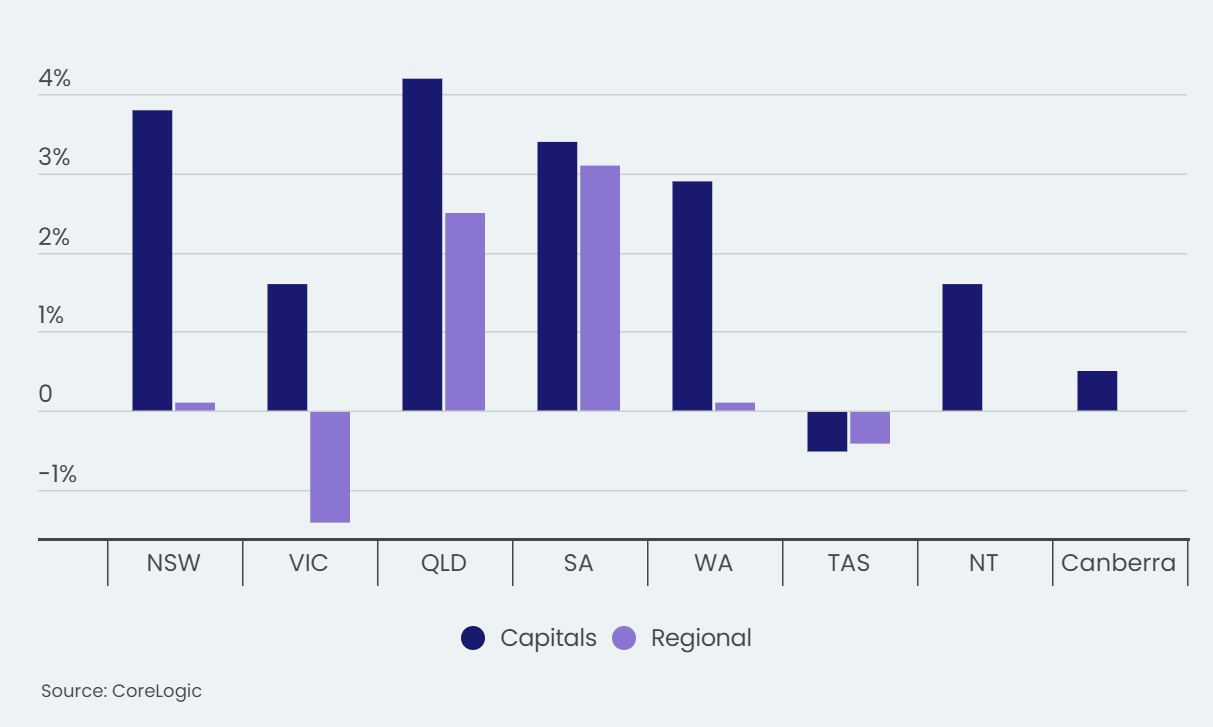

CoreLogic’s latest Home Value Index, released this week, shows home prices nationally inched upwards by 0.8 percent in August – the sixth consecutive month of growth.

Since bottoming out in February, prices at a national level are 4.9 per cent higher, adding $34,000 to the median value of a dwelling.

Sydney has led the recovery trend, with a gain of 8.8% since values found a floor in the Harbour City in January, while Brisbane has also seen values up 6.2% since bottoming out in February.

Ray White’s Lower North Shore Group posted $216 million in sales in August while Ray White Quakers Hill sold 135 homes.

Mr White is expecting the coming months – traditionally the busiest in real estate – to be just as busy.

“There will be enough stock to record some big results – maybe not at 2021 levels but not too far off,” he said. “So much depends of course on the broader economic sentiment and how that influences buyer behaviour.”

One likely driver of sustained buyer confidence is the decision this week by the Reserve Bank to leave interest rates on hold, which has led many economists to believe the tightening cycle is on hold for now.

Demand for historic, inland homes is driving the latest housing boom in Ibiza—Spain’s party-loving island in the Mediterranean that’s better known for attracting celebrities and business tycoons to rent seaside villas or bask in their mega yachts along the coast.

Prices for renting or buying a property on the island have long been a pricey proposition, with demand high and inventory low. Since the start of the pandemic, however, this interest has grown significantly, along with prices. Waterfront properties are perennially popular and glamourised in the global press, but the residential market on the inner part of the island away from the sea has underpinned this recent spike, according to Jack Harris, a partner in the International Residential Department at the London-based firm Knight Frank.

“The coastal areas are more touristic, and as a result, they’re more transient and seasonal, with a fluctuating population that peaks in summer,” he said. “The centre of the island is a year-round destination with a variety of villages that bustle with life that include festivals, Christmas markets, art galleries, restaurants and more.”

Located off Spain’s eastern coast and one of the main Balearic islands, Ibiza may rank as the world’s most legendary party destination. It’s a culture that’s epitomised by the electronic dance music scene and nightclubs such as Pacha and Hi, where all-night bashes are the norm and tables command up to $50,000. According to Serena Cook, the founder of the luxury lifestyle company Deliciously Sorted Ibiza and a local resident, Ibiza has always been a hub for creatives.

Cook added that Ibiza’s mild winters, which see plenty of sunny days, have attracted home buyers to move there full time. People also come for the free-spirited vibe

“It’s a free-spirited place where anything goes, and there’s a melting pot of different nationalities,” she said. “In the last half-decade or so, it has gotten more and more luxury-focused.”

Booming Inland Towns

Santa Gertrudis is at the epicentre of inland living and has numerous notable restaurants and cafes as well as the international children’s school Morna International College, where transplants and locals enrol their children. Other towns include Sant Joan de Labritja and Sant Josep de sa Talaia.

In contrast to the contemporary villas typically near or on the water, these inland areas stand out for their fincas—either traditional homes dating to the 18th and 19th centuries that are constructed of mud and stone or new properties built in the classic finca style but reinterpreted for modern-day living. Harris and Cook said that the latter are hard to come by because the local government is stringent about protecting the landscape and doesn’t grant permits easily.

Fincas feature views of hills and olive trees instead of the ocean, and over the last three years, Harris said, the market for them has appreciated in the double digits.

“The advent of remote working is in large part behind this rise,” he said. “People are drawn to the serenity of the countryside, the amount of outdoor space you can get and the fact that you’re surrounded by nature.”

Given Ibiza’s relatively small size, the coast from any of these inland towns is less than a 30-minute drive away.

“If you feel like going snorkelling one day, you can choose the beach with the calmest water, and if windsurfing is what you’re after, you’re never too far from the beach with the best wind,” Harris said.

Local real estate firms also report an increase in sales of inland properties. It’s a local boom that’s defying a global slowdown that’s impacted high-end markets from London to Berlin in the face of rising interest rates and economic uncertainty.

Javier Medina, an agency manager at the real estate firm John Taylor Ibiza, said that his company has seen “soaring sales” in the past two years. “We had an increase of 30% in the first half of 2023 compared with 2022,” he said.

Meanwhile, Cook said her business “has gone through the roof.”

“We’ve jumped by 20% and sold five countryside homes last year for US$5 million or more,” she said. Inland homeowners include buyers from the U.S., especially New Yorkers and tech entrepreneurs from the West Coast, Europeans from countries such as England, France and the Netherlands. Several notable examples include the French designer Isabel Marant and the New York art gallery owner Howard Greenberg.

In following the trend, Cook herself sold her coastal home in 2021 and moved to a countryside property because she wanted more outdoor space and a garden to grow her own produce. Cook is the founder of Ibiza Preservation, a nonprofit that protects the local environment. The group recently reported that organic farming in Ibiza has jumped 20% in the last 10 years, with many inland homeowners growing their own fruits and vegetables.

Not Exactly a Bargain

A finca’s lack of sea views doesn’t mean bargain pricing, Harris said.

“With pricing high, your money shall certainly go further inland in comparison with the coast,” he said. “That said, properties historically hold their value no matter where they are.”

A countryside finca that’s in good condition and has four bedrooms, open views, a swimming pool, pool house, multiple outdoor terraces and possibly some olive trees, costs at least US$3.5 million, Harris said. Coastal properties of the same caliber are more than US$5 million and can be higher if they offer especially dramatic views.

The architecture firm Blakstad Ibiza is behind the most sought-after and priciest inland homes. Founded by Rolf Blackstad in the 1960s, it’s now run by his son, also named Rolf. The company refurbishes rundown fincas and also builds new ones, the younger Blakstad said, with prices averaging between US$6 million to US$18 million for a property.

“We had a half dozen or so projects a year pre-Covid, but now work on a dozen,” he said.

Blakstad’s fincas typically span between 5,000 and 6,000 square feet and feature sustainably sourced timber, bedrooms with outdoor showers, solar energy, large doors that open to outdoor spaces such as terraces and gardens that may blend into farmland.

As an example, Knight Frank is currently offering a renovated turnkey Blakstad-designed finca in the village of San Rafael that costs close to US$6.5 million and is set on a hillside. Surrounded by pine forests and Mediterranean plants, it has five bedrooms spread over a main and guest house, five baths, an abundance of outdoor space including a landscaped garden and a swimming pool.

“Ibiza’s parties will forever be iconic and appeal to tourists,” Harris said. “Look a little deeper, however, into the middle of the island, and you’ll discover why so many people are choosing to make it their home.”

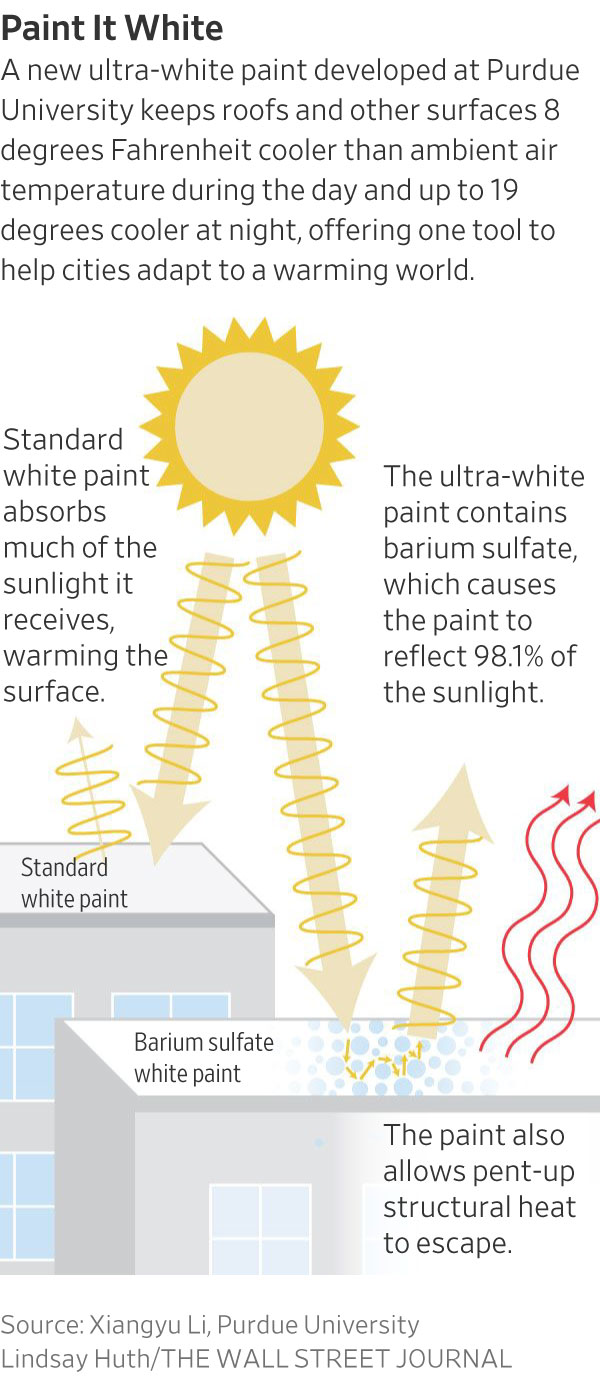

Cities across the U.S. have found relief from this summer’s record-setting heat with the help of technologies that shield roofs, pavement and other surfaces from the sun’s scorching rays.

Some of these technologies have been around for more than a decade but are experiencing greater demand as global temperatures rise. Washington, D.C., for example, has built more than 3,200 green roofs covering 9 million square feet—up from about 300,000 square feet in 2006, according to federal and city officials.

Other technologies, such as super-reflective coatings for pavement, streets and windows, are just now becoming effective and affordable enough for widespread use.

The Los Angeles neighbourhood of Pacoima, a densely packed location sandwiched between freeways and an industrial area, has created a partnership with GAF, a New Jersey-based roofing manufacturer, to paint a basketball court, local park and neighbourhood streets with a reflective coating.

“There’s a lot of asphalt and lack of investment for tree canopies,” said Melanie Paola Torres, 24 years old, a community organiser with the group Pacoima Beautiful. “Given the fact that we are in an industrial zone, that contributes to the urban heat-island effect.”

The reflective coating has reduced air temperatures in the test area at 6 feet above ground by 3.5 degrees Fahrenheit during extreme heat days, and surface temperatures by 10 degrees, according to Jeff Terry, GAF’s vice president of corporate social responsibility and sustainability.

Sweltering conditions are worse in urban heat islands, which can be 10 degrees hotter than surrounding suburbs and occur as buildings, roads and other infrastructure absorb and re-emit the sun’s energy.

Cooling technologies mitigate this. Green roofs absorb heat before it penetrates the buildings beneath. Super-reflective coatings reflect the sun’s visible light and invisible infrared radiation away from surfaces to keep them cooler. And an ultra-white paint developed at Purdue University promises even more protection, although the product isn’t commercially available yet. Each strategy helps reduce energy use.

“The important thing is to help people cool their homes and workplaces affordably,” said Jane Gilbert, chief heat officer for Miami-Dade County, which experienced a record 46 straight days of a 100-degree-plus heat index this summer. “The more efficient we can make both the buildings and the AC systems themselves, the less we’re contributing both to greenhouse gases and also waste heat that goes to our urban heat islands.”

Miami is one of the most vulnerable cities to the urban heat-island effect, along with San Francisco, New York, Chicago and Seattle, according to an analysis by Climate Central, a New Jersey-based nonprofit that researches the effects of climate change. Its analysis found that 41 million people living in 44 cities face an urban heat-island effect of at least 8 degrees. Nine U.S. cities had at least one million people exposed to urban heat of 8 degrees or higher because of the local built environment.

To fight the heat, some cities are leveraging federal money and other incentives to persuade local builders to turn office buildings greener and cooler.

In Miami-Dade County, officials used federal funds to outfit 1,700 public housing units with new low-energy air-conditioning units. Local officials also offered a successful amendment to the Florida state building code requiring cool reflective roofs on all new commercial buildings beginning in 2024, and enrolled 150 structures in a voluntary energy-audit program to track improvements to cut energy use and keep temperatures down.

New York, Chicago, Philadelphia, Toronto and other cities are pushing green roofs with tax breaks and other incentives in an effort to lower energy bills and reduce ambient temperatures, according to Steven Peck, president of Green Roofs for Healthy Cities, a Toronto-based green-roof and -wall industry association. Peck said green roofs can be 30 to 40 degrees cooler than a similar-size blacktop roof, while also cutting waste heat from air-conditioning units.

In the Los Angeles neighbourhood of Pacoima, Torres says residents tell her the streets and playgrounds feel cooler since the reflective coating was completed in August 2022.

“The number-one thing that always comes up is the heat waves when you’re looking down the street,” Torres said. “They don’t see those anymore.”

The next step is to install reflective roofing material on a handful of homes as part of the neighbourhood cooling effort. “We want to keep stacking the solutions to overall create a cool community with multiple strategies,” Torres said.

Altering the urban landscape to adapt to extreme heat requires money and technical know-how, according to city leaders and academic experts. But they also acknowledge the need to keep people safe as global temperatures rise.

“Any one solution is not going to necessarily be able to address the entire problem, but by systematically applying solutions that work in each individual location, we can make a dent in the urban heat-island effect,” said David Sailor, professor of geographical sciences and urban planning at Arizona State University.

Interest rates will remain on hold for another month, the RBA Board announced today.

In a statement released by Dr Philip Lowe – his last as governor of the RBA – he said the current 4.1 percent interest rate is creating ‘a more sustainable balance’ between economic supply and demand.

“In light of this and the uncertainty surrounding the economic outlook, the Board again decided to hold interest rates steady this month,” Dr Lowe said. “This will provide further time to assess the impact of the increase in interest rates to date and the economic outlook.”

The news was widely expected among economists and the major banks following the announcement that the rate of inflation had fallen to 4.9 percent in July, down from 5.4 percent in June.

Dr Lowe said inflation had passed its peak but it was still too high.

“While goods price inflation has eased, the prices of many services are rising briskly,” he said. “Rent inflation is also elevated. The central forecast is for CPI inflation to continue to decline and to be back within the 2–3 percent target range in late 2025.”

CoreLogic research director Tim Lawless said rents would most likely continue to put pressure on inflation for some time yet.

“CPI rents, which are allocated the second largest weighting within the CPI ‘basket’, remain a major inflationary driver, with the monthly CPI indicator reporting a 7.6 percent rise in the cost of rents in the year to July, accelerating from 7.3 percent in June.

“The trend indicates no slowdown in growth for rents paid.”

Acknowledging the two speed economy, Dr Lowe said some Australians were feeling the financial pinch of elevated interest rates more than others.

“The outlook for household consumption also remains uncertain, with many households experiencing a painful squeeze on their finances, while some are benefiting from rising housing prices, substantial savings buffers and higher interest income,” he said.

However, he did not rule out further rate increases.

“Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will continue to depend upon the data and the evolving assessment of risks,” he said. “In making its decisions, the Board will continue to pay close attention to developments in the global economy, trends in household spending, and the outlook for inflation and the labour market.

“The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that.”

Dr Lowe will step down as governor in two weeks’ time. He will be succeeded by Michele Bullock.

Interest rates are expected to stay on hold when the Reserve Bank of Australia Board meets this afternoon, the last with Dr Philip Lowe as governor.

While economists have been split in recent months ahead of RBA Board meetings, they are unanimous that today’s decision will be to keep the interest rate at 4.1 percent.

This follows news that the inflation rate has continued to fall, with July figures from the Australian Bureau of Statistics showing it had dropped to 4.9 percent, down from 5.4 percent in June. The board had repeatedly cited high inflation for its decision to increase the cash rate, which has risen 400 basis points since May 2022.

However, the inflation target is between 2 and 3 percent. In his statement at last month’s board meeting, Dr Lowe flagged that further increases were still possible.

“Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will depend upon the data and the evolving assessment of risks,” he said last month. “In making its decisions, the Board will continue to pay close attention to developments in the global economy, trends in household spending, and the outlook for inflation and the labour market.

“The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that.”

The meeting marks Dr Lowe’s last as governor. Economist Michele Bullock will step into the role in mid September, the first woman to be appointed RBA governor.

For some investors seeking to diversify their portfolios, emerging markets are looking increasingly attractive.

There are 169 emerging-markets stock ETFs available to fund investors, with total assets of about $296 billion, according to fund researcher Morningstar Direct.

Some analysts and financial advisers say there is a lot to like about this sector right now. What is the argument for putting money into these exchange-traded funds? And what’s the argument for getting out, or not starting at all? Here’s a look at the pros and cons.

The Pros

One factor driving interest in emerging-markets ETFs is that emerging economies are growing faster than advanced economies, and that isn’t forecast to change soon. The International Monetary Fund forecasts real GDP growth of only 1.4% in advanced economies in 2024 due to inflation, monetary policy and other factors. In contrast, the IMF projects real GDP growth of 4.1% for emerging and developing economies, helped by countries such as India, which is expected to grow at a rate of 6.3%.

“The biggest reason to invest in emerging-markets ETFs today is to gain exposure to high-growth markets with burgeoning middle-class consumers such as China, India, Mexico, Taiwan, South Korea and Vietnam,” says Aniket Ullal, senior vice president and head of ETF data and analytics at CFRA Research. He says emerging markets are home to more than 4.3 billion people, and they account for about half of global GDP.

Crowds in the Ximen shopping district in Taipei, Taiwan., in June. Taiwan is one of the emerging economies that some ETFs focus on. PHOTO: AN RONG XU FOR THE WALL STREET JOURNAL

Another attraction is that valuations on emerging-markets stocks are low. While the price-to-earnings ratio of the S&P 500 was 22.4 based on trailing 12-month reported earnings as of July 31, the P/E ratio of the MSCI Emerging Markets—which includes the stock of most liquid large- and midcap companies in 25 emerging-market countries—was 14.13.

“This is a smart contrarian play for investors who want to diversify their portfolios geographically,” says Gabriel Shahin, president of Falcon Wealth Planning, an investment adviser in Los Angeles. “There is a fire sale going on in emerging-market stocks, and this is one of the smartest plays in equity investing right now.”

Some see these investments as a hedge, considering this year’s U.S. stock rally—dominated by a small number of large-cap technology companies—could end at any time.

Emerging-markets ETFs come in many varieties, so investors can choose those that align with their macroeconomic outlook and financial goals.

While some of these funds invest in a broad basket of emerging-market countries that span the globe such as the $72.1 billion iShares Core MSCI Emerging Markets ETF (IEMG), others invest in geographic regions such as Asia or Latin America or are country-specific.

The $64.2 million Franklin FTSE Latin America ETF (FLLA), for example, invests in large-cap and midcap companies in Brazil, Chile, Colombia and Mexico. It has returned more than 19% year-to-date through Aug. 29 and 15.6% over the past year. The $175.8 million Franklin FTSE Taiwan ETF (FLTW) invests in midcap and large-cap Taiwanese companies. It has a year-to-date return of 14.7% and a one-year-return of 8.2% as of Aug. 29.

For investors concerned about the economic slowdown in China, there are emerging-markets ETFs that exclude Chinese equities such as the $5.16 billion iShares MSCI Emerging Markets ex-China (EMXC). Its top holdings are Taiwan Semiconductor Manufacturing, Samsung Electronics and Reliance Industries.

Some emerging-markets ETFs target small- or large-cap stocks. One is the $34.2 million VanEck Brazil Small-Cap ETF (BRF), which is up about 32% year-to-date and 11.4% over one year as of Aug. 29. Others focus on industry sectors such as technology and e-commerce.

While most emerging-markets equity ETFs track indexes, an increasing number of newer funds are actively managed. Of the 11 emerging-markets ETFs that have launched this year, eight are actively managed, including Global X Brazil Active ETF (BRAZ), a $2.61 million fund that invests in Brazilian companies such as Petrobras, a multinational petroleum company, and Vale, the world’s largest iron-ore producer.

There are even emerging-markets ETFs that pay dividends, such as the $243.5 million SPDR S&P Emerging Market Dividend ETF (EDIV), which is up 28.2% year-to-date through Aug. 29 and has a dividend yield of 3.78%.

According to Morningstar Direct, the top-performing emerging market ETFs this year through Aug. 29 are VanEck Brazil Small-Cap, SPDR S&P Emerging Market Dividend and iShares MSCI Brazil Small-Cap (EWZS), which is up 24.1% so far this year and 5.7% over one year.

The Cons

Some advisers, however, say investors looking at emerging-markets equity funds should proceed with caution.

“Emerging-markets equity ETFs are more volatile than international ETFs that focus on stocks in advanced economies,” says Lan Anh Tran, a research analyst at Morningstar Direct. Over the past 10 years ended July 31, 2023, the standard deviation of the MSCI Emerging Market Index was 16.2% higher than the MSCI World Index—a proxy for global developed-market stocks, she notes. Standard deviation measures volatility, with a higher number representing more volatility.

That’s because any sudden geopolitical event (such as the war in Ukraine) or any economic shock (like soaring inflation or a global supply-chain disruption) can have a jarring effect on emerging-market economies that are dependent on commodity exports, tourism and the health of advanced economies, investment strategists say.

There also is the risk of government influence and regulation on emerging-markets stocks, says Tran. A government, for example, can decide to nationalize an industry at any time, or exercise control over an industry sector.

Currency movements are another risk factor to consider, says CFRA’s Ullal. “If the dollar strengthens against local currencies, your fund returns will erode,” he says.

“It’s important that investors understand this is a high-risk, high-reward investment before they dive into them,” says Andrew J. Feldman, the founder of A.J. Feldman Financial in Chicago. “These funds can be highly volatile due to a host of systemic risks in emerging-market countries, including economic risk, geopolitical risk, currency risk and liquidity risk.”

These challenges make some investors skittish about investing in emerging-markets ETFs, says Kevin Shuller, founder and chief investment officer of Cedar Peak Wealth Advisors in Denver. “They believe that companies domiciled in the U.S. do a lot of business in emerging markets, so if you own the S&P 500 or MSCI EAFE index you have all the exposure you need.”

“It’s a good counterargument,” he says, “but [it] doesn’t take into account that the party in the U.S. stock market may not go on forever.”

Many investment advisers instead suggest individual investors take a step-by-step approach when choosing an emerging-markets ETF and allocate 5% to 10% of their equity portfolio in such vehicles.

“Country selection matters most so check the fund’s geographic exposure,” says Perth Tolle, founder of Life + Liberty Indexes and the $625.4 million Freedom 100 Emerging Markets ETF (FRDM), which invests in about 100 companies in 10 countries that aren’t autocracies but freer markets such as Chile, Poland, South Korea and Taiwan.

Also look at the methodologies and metrics the ETF uses when choosing stocks for its index or portfolio, as well as the fund fees. The average expense ratio for this ETF group is 0.51%, according to Morningstar Direct.

“A good way to assess a fund’s value is to look at its weighted average price to cash flow,” a measure of the price of a company’s stock relative to how much cash flow it generates, says Kevin Grogan, chief investment officer at Buckingham Wealth Partners in St. Louis. It gives a pulse reading on how cheap or expensive the emerging-markets stocks are in the fund.

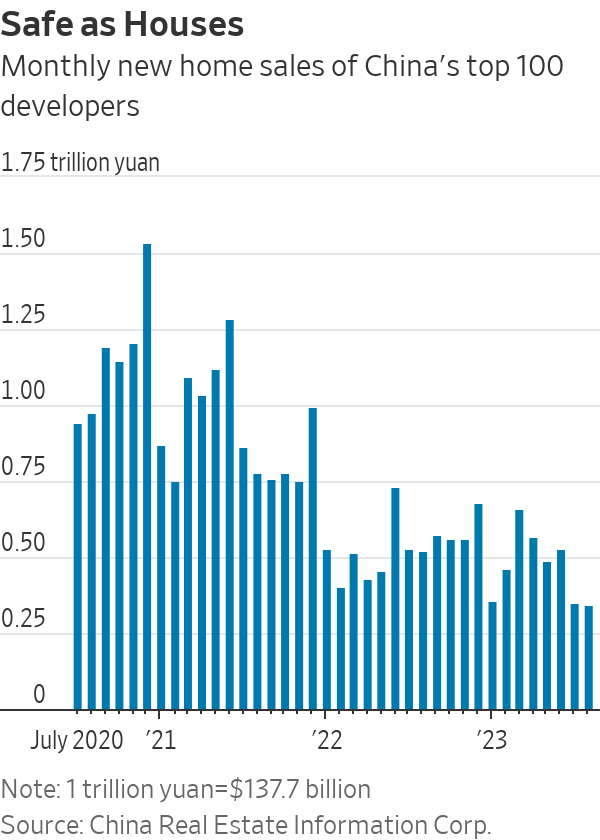

HONG KONG—China’s top surviving private developer bought more time to sort out its liquidity problems, giving investors hope that it will cobble together enough cash to avoid defaulting on its U.S. dollar bonds this week.

Country Garden Holdings on Friday said it got approval from investors in mainland China to extend the maturity date of $537 million in domestic bonds by three years. The yuan-denominated debt was originally due Monday. An offshore unit of the 31-year-old property giant separately made an interest payment of around $600,000 on a bond denominated in Malaysian ringgit on Monday, according to a person familiar with the matter.

The debt extension and bond payment created optimism that Country Garden can address a debt load that includes a range of foreign currency bonds—and a make-or-break interest payment this week.

The developer’s Hong Kong-listed shares jumped 15% on Monday, closing at their highest level in about three weeks. Other Chinese property stocks also gained, while the broader Hang Seng Index rose 2.5%.

Country Garden’s bond prices also edged higher, although most of its dollar bonds remained below 10 cents on the dollar, levels that indicate a high probability of default.

Chinese authorities have taken more steps in recent days to shore up the country’s beleaguered housing market, where sales have declined for most of the last two years. Last Thursday, the People’s Bank of China lowered minimum down payments on first and second home purchases and told banks they can lower the rates on existing mortgages. Regulators also recently expanded the definition of a first-time home buyer, a category that comes with lower mortgage rates and smaller down payments.

The rule changes helped to draw more people to real estate showrooms over the weekend. Demand for new homes in Shanghai increased noticeably after the new measures were implemented, according to Chen Julan, a senior analyst with China Index Academy. In Beijing, some developers withdrew discounts and adjusted their prices slightly higher, the research firm said.

The new rules could give a temporary boost to home sales in about a dozen major cities, said Song Hongwei, a research director of Tongce Research Institute, which tracks and analyses China’s real-estate market. He said lower-tier, poorer cities may not reap similar benefits and predicted that the overall housing market will eventually weaken again.

Country Garden’s recent cash crunch has largely been a result of slumping home sales in many parts of China. The company is one of the biggest surviving privately run developers and has a large presence in the country’s poorer regions. In August, it sold homes valued at a total of around $1.1 billion, almost three-quarters lower than a year earlier.

The company missed $22.5 million in coupon payments on bonds with a total face value of $1 billion in early August, and has a 30-day grace period to come up with the money. That grace period expires this week.

Even if it does pay the interest on its dollar bonds this week, it has many more coupon payments due in the coming months. Investors are skeptical that it can avoid default—unless its sales start growing again. Country Garden’s most recent financial report said that as of June 30, it had the equivalent of $15 billion in bonds, bank debt and other borrowings due within a year.

The company lost more than $7 billion in the first half of 2023, its worst financial performance since it went public in 2007, after its contracted sales for the period shrank 30%. Country Garden told investors it was “deeply remorseful” but said it was committed to turning things around.

China’s economy has struggled through much of this year, with falling exports, weak manufacturing and a slowdown in consumer spending all pointing to problems broader than a property slowdown. But cracks in the property sector, which was once seen as a major source of wealth creation in China, are exacerbating the broader economic malaise.

Chinese property developers’ falling property margins and weak sales will weigh on earnings until the end of next year, according to analysts at S&P Global Ratings. Not all developers will feel the same degree of pain. Those with links to the government or with good access to financing are better positioned to endure the fall in margins, the S&P analysts said in a note on Monday.

When the newly appointed CEO of King Living, David Woollcott, first started with the Australian furniture retailer last year, he admits he was puzzled by the price point for their popular range of sofas.

“I was questioning why we don’t charge more for our product,” he said. “With the Jasper (sofa), which starts from around $4000, we could charge $7000 or $8000.”

The galvanised steel-framed sofas, which come with a 25-year warranty, have a strong following in Australia where they are a popular choice for those looking for affordable style that will last. The range includes sofas and armchairs in a variety of styles designed to be flexible enough to suit any space, or lifestyle, at a price point that is deliberately accessible.

King Living CEO David Woollcott

Central to the success of King Living, which started as a mother and son enterprise with David King and his mother Gwen in the 1970s, has been the decision to keep design, manufacturing and retailing under the one roof. Woollcott said it places King Living in a rare position in the market.

“We are in control, which is exciting for the consumer,” he said. “We know how our product is made and where the materials are sourced and we are acting as one entity. That instils trust.”

It also means there are no additional players looking to add further costs.

“We don’t support a third party, so the additional margin we invest in quality,” he said.

King Living has marked their time in the Australian market with the re-release of its first piece of furniture, now known as the 1977 sofa. A surprisingly contemporary-looking chair designed to be ‘built’ piece by piece to create a modular sofa of your choice to suit small or large spaces, it embodies the kind of relaxed elegance Australian design has become known for.

The 1977 King Living sofa was recently re-released. It can be mixed and matched to any configuration.

It’s a design aesthetic and business model Woollcott said has been embraced as King Living expanded into markets in Singapore and Europe in recent years with North America to follow soon.

“What delineates us is that we are a designer, manufacturer and retailer of furniture — that is really unique,” he said. “There are many businesses who do the retail bit and they source from factories around the world. But we are in control, which is exciting for the consumer.”

While the size of living spaces vary significantly across Europe, Asia and North America, Woollcott said there is enough variation and flexibility in the range to accommodate customers’ needs, whether it is the generous proportions of the Jasper and Kato sofas or the more compact Aura and Fleur designs. While best known for their sofas, King Living also has an extensive range of dining furniture, as well as beds, floorcoverings, lighting and storage options. Their outdoor furniture range is also gaining a strong following, taking the same approach to the design and construction of their interior furniture and translating it for outdoor spaces.

And it’s not just the Australian market taking notice.

“Australian design is globally loved because it has a casual nature to it,” he said. “It’s informal, which doesn’t mean it is less sophisticated or less detailed.

“Coming from the UK where it is all about the class structure and formality, Australia is the antithesis. It’s warm, approachable and casual.”

The King Cove reclining sun lounge is part of the popular outdoor furniture range.

Having spent the past five years in Europe as managing director of Fisher & Paykel UK & Europe, Woollcott is aware that customers are increasingly concerned about the sustainability of their products. The ‘reduce, reuse and recycle’ ethos is nothing new to King Living, he said.

“What stunned me when I met (founder) David King, they have acted sustainably from day one because they have made that link with waste not being a good thing,” he said. “It’s all about resources. I don’t think there would be a business leader out there who would not see the link between preserving resources and saving money.”

King Living also offers their King Care service, a commitment to recover or completely refurbish sofas for a cost, whether they were manufactured in 1977 or 2023.

While it may seem like a lot of fuss over a sofa, Woollcott noted that this key piece of furniture is often the backdrop to family life for years.

“Memories are made on our furniture and the sofa can end up becoming a member of the family,” he said. “Our furniture is designed to last for generations — and to be reconditioned.

New data has uncovered the most tightly held suburbs across Australia, where happy homeowners very rarely sell up.

According to research firm PropTrack, the average time Aussies own their home has jumped by a quarter over the past decade to a whopping 11 years.

“The most tightly held suburbs tend to be those that appeal to a wide range of different people, from young families to retirees, and are often located in the middle and outer suburban rings,” PropTrack economist Anne Flaherty said.

These hot areas usually have sought-after amenities like good schools and shopping options, as well as appealing lifestyle characteristics such as parks or proximity to the water, Ms Flaherty added.

Clarinda in Melbourne’s southeast is the most tightly held suburb in the country, where houses are owned for an average of 24 years.

Houses in Clarinda in Melbourne’s south east rarely come to market

The top suburb for units is popular Cremorne Point on Sydney’s Lower North Shore, where apartment owners don’t budge for an average of 17 years.

Arncliffe in the city’s south is the tightest held for houses nationally at 21 years.

That suburb has seen soaring demand in recent times, particularly among young families and first-home buyers, with the median house price jumping from $1 million at the end of 2019 to $1.54 million currently.

Reflecting the strength of property markets in Australia’s two largest capital cities in the past decade, no Queensland suburbs made the top 10 list for houses.

However, Rochedale South in Brisbane’s south appeared in the units list with an average hold time of 15 years.

Two other areas outside of Sydney and Melbourne also appeared. Perth pockets Shelley and Kalamuna each have average hold times of 15 years.

Ms Flaherty said tightly held suburbs tend to have a high proportion of owner-occupiers and a higher median resident age.

The dominant dwelling type is also usually a detached house and areas are well-connected to CBDs via quality transport infrastructure, she added.

On the flipside of things, PropTrack also crunched the numbers on the suburbs with the shortest hold times, with semi-rural Pimpama on the northern fringe of the Gold Coast ranking first at four years.

When it comes to units, Hope Island, also on the Gold Coast, has the quickest tenure with four-and-a-half years.

China’s economic troubles have so far been a boon to other Asian markets. But if the world’s second largest economy continues to turn sour, things could start to look uglier for them too.

Major Asian stock markets have been doing well in 2023. Japan’s Topix index has gained 24% this year while Taiwan’s Taiex index has risen 18% and Korea’s Kospi is up 15%. That is in contrast to Chinese stocks: the MSCI China index has dropped 6%, despite a strong start of the year.

There are some fundamental reasons why Asian stocks outside of China have gone up. Buybacks and dividends are rising in Japan, while Warren Buffett’s endorsement gave the market another push. The hope of an eventual rebound in the semiconductor industry has lifted stocks in Taiwan and South Korea. But these markets also benefited from foreign investors fleeing Chinese stocks: markets such as Japan and South Korea have seen foreign inflows in recent months. Some multinationals have also been migrating manufacturing out of China and into other Asian countries to diversify their supply chains.

However, Goldman Sachs has noted that correlations between China and other markets in the region have risen lately, indicating potential concerns of spillover.

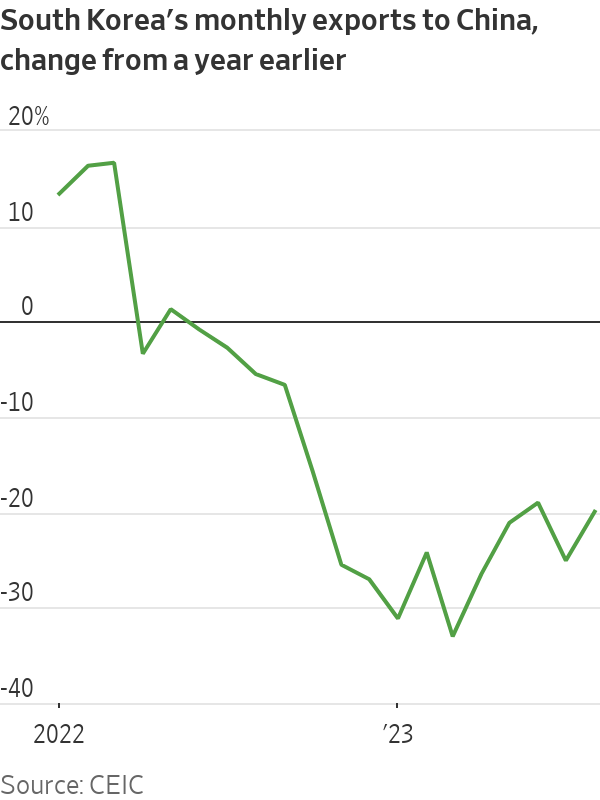

China is the top trading partner of many countries in the region like Japan and South Korea, and weak demand from China could ripple through to its neighbours. South Korea’s exports to China, accounting for roughly 20% of its total, fell 25% year on year in the first eight months of this year.

And falling investment in China—especially in the real-estate sector—could weigh on commodity prices. So far prices of commodities such as iron ore have been resilient this year as demand from sectors like autos and infrastructure have softened the blows from property construction. But commodity-exporting nations such as Australia, Malaysia and Indonesia could suffer if Chinese investment remains weak.

The confidence crisis in China could also hurt companies selling to the country’s consumers. The number of Chinese tourists, in particular, is still way down from pre-Covid levels for many countries like Japan and Thailand.

As China is the economic juggernaut in the region, the country’s pain is unlikely to be its neighbours’ gain for long.

Their buildings echo with empty offices, their borrowing costs have soared, and now owners of buildings in cities across the U.S. are facing a new tax on their carbon emissions.

Cities are toughening their climate standards and are beginning to tax buildings that don’t meet the new requirements. Landlords are left with a difficult choice between paying for expensive upgrades to reduce emissions or paying the tax.

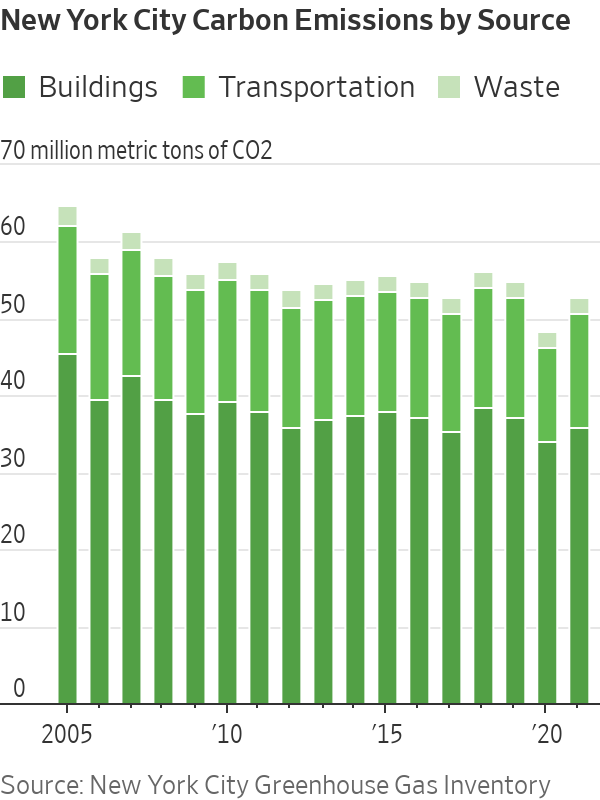

In New York City, which has one of the first and most expensive carbon taxes, landlords of large buildings (including owners of residential buildings) beginning next year will face a $268 fine for every ton of carbon dioxide emitted beyond certain limits.

“If you’re under cash flow pressure due to lack of tenancy, adding a tax on top of that isn’t a good sign,” said Bank of America CMBS Strategist Alan Todd. “It would be potentially pretty painful.”

The Wall Street Journal tallied the potential impact of the taxes on buildings that borrowed funds from Wall Street investors by issuing mortgage-backed bonds. The Journal also looked at properties owned by three of the country’s largest publicly traded landlords. The tax bill for 128 properties analyzed could add up to more than $50 million during the first five-year enforcement period, which begins in 2024, according to the Journal’s analysis of Department of Building data and financial disclosures.

Fines for the same buildings could jump to $214 million if their landlords don’t meet the city’s emissions standards during the period between 2030 and 2034, the Journal’s analysis shows. The Real Estate Board of New York, an industry group, and engineering consulting firm Level Infrastructure said that more than 13,000 properties could face fines totaling about $900 million annually.

Buildings are by far New York City’s largest source of carbon emissions, which come from the fossil fuels used to heat and to provide air conditioning for them.

More than a dozen local laws regulating buildings’ carbon footprints from Chula Vista, Calif., to Boston have gone into effect since 2021 or will come online by 2030, according to carbon accounting firm nZero. Compliance also begins next year for buildings in Denver, while St. Louis properties face penalties beginning in 2025. Four other laws from Cambridge, Mass., to Reno, Nev., will go into effect in 2026.

The impact of the emissions laws initially will be small but will come on top of other, more costly problems faced by landlords. The law, based on New York’s current projections, would cost the 51-story skyscraper at 277 Park Ave. in Manhattan just $1.3 million in fines in 2024. The revenue of the building, owned by private landlord The Stahl Organization, was $129 million last year.

The building’s vacancy rate has jumped from about 2% in 2014 to 25% currently, according to commercial property data provider Trepp. JP Morgan Chase accounts for about half of the building’s space, but its lease expires in 2026. The bank is constructing a nearby tower that aims to produce net-zero carbon emissions and is scheduled to be completed in 2025. It wouldn’t comment on its leasing plans.

Stahl’s $750 million mortgage on the building is scheduled to mature next August. Stahl is now faced with potentially higher rates if it takes out a new loan, the loss of its biggest tenant and fines for carbon emissions.

Stahl declined to comment.

Shares of the three big landlords whose properties were analysed by the Journal are trading at near historic lows. Shares of Vornado Realty Trust and SL Green, each of which has about 30 New York City office buildings, are down by roughly two-thirds since before the pandemic. Boston Properties Inc., one of the country’s largest office building owners, shares are down more than 50% from before the pandemic.

SL Green faces a potential carbon-tax liability of up to $6.6 million by 2030, according to the Journal’s analysis. The company declined to comment. More than 80 other properties financed using mortgage-backed bonds reviewed by the Journal could have a nearly $27 million carbon-tax bill by 2030.

The costly upgrades needed to comply with the law will hit some properties when they are on the block or when they are trying to attract tenants, who know they will effectively be paying for any improvements. “Tenants are looking to be in a building that is greener,” said Brendan Schmitt, partner in law firm Herrick’s Real Estate Department.

The library at the Manhattan office of Vornado Realty Trust, one of the landlords expected to be on the hook for a significant amount of New York City carbon taxes. PHOTO: VICTOR LLORENTE FOR THE WALL STREET JOURNAL

The new laws coincide with big government spending on climate. Landlords can get generous subsidies for projects that reduce emissions.

Ironically, landlords are also benefiting from emptier buildings, which burn less fossil fuel. New York City says about 11% of buildings covered under the law are projected to face penalties using the latest energy data, down from 20% using earlier data.

The city’s law was passed in 2019 and included a $268 fine for every ton of CO emitted by buildings over 25,000 square feet exceeding limits. Landlords will be required to report emissions to city officials starting in 2025 with penalties based on 2024 energy use.

Some big landlords are facing fines in multiple jurisdictions including Boston Properties, which will likely get hit on properties it owns in Boston, New York and Washington, D.C. The company’s eight New York City offices could face a $2.3 million dollar tax bill by 2030, according to city data.

Ben Myers, senior vice president of sustainability at Boston Properties, said complying with local building standards is important. “We have made energy efficiency a priority,” he said.

Artificial intelligence is starting to help buildings go greener.

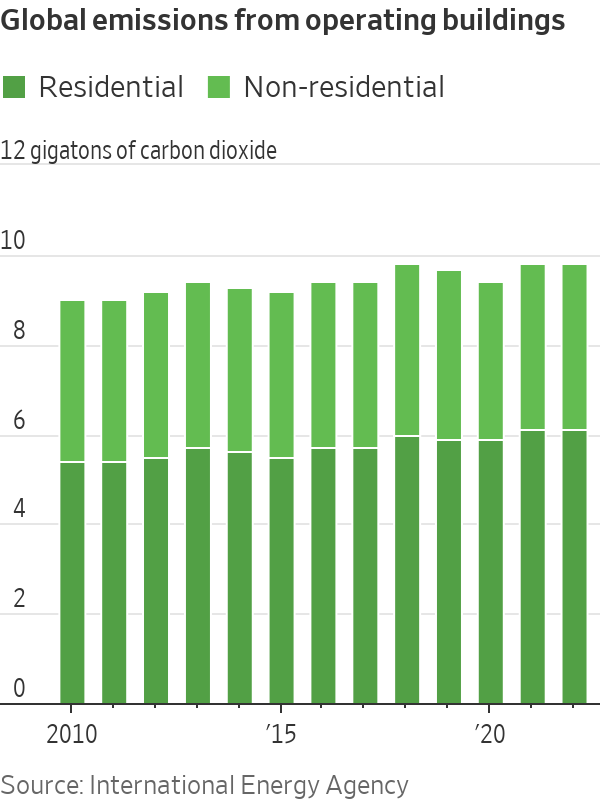

Keeping our buildings running contributed roughly 26% of global energy-related greenhouse-gas emissions in 2022, according to the International Energy Agency. For the world to reach net-zero emissions by 2050, the agency says the energy that these buildings consume per square meter (around 11 square feet) needs to decline by around 35% by 2030.

Developers and construction companies have pursued more-efficient energy use in buildings over the past couple of decades. Leadership in Energy and Environmental Design, or LEED, certifications are given to buildings that meet standards that conserve energy, water, waste and other environmental goals.

Governments are also introducing increasingly stringent energy codes for commercial spaces. Still, more than 80% of buildings don’t have smart systems to efficiently manage their energy use.

JLL, which manages billions of square feet of commercial real estate around the world, has been making a string of investments to bring AI systems to companies looking to cut their emissions. The business case: Eco-friendly buildings charge higher rents and are on the market for less time. JLL says it expects 56% of organisations to pay a premium for sustainable spaces by 2025.

“We want to make every building out there as smart as it can be,” said Ramya Ravichandar, JLL Technologies’s vice president, technology platforms—smart and sustainable buildings. “If you can’t measure what matters, you can’t make the change.”

JLL’s investments include in Turntide, a company based in Sunnyvale, Calif. that installs electric motors coupled with small computers which learn from patterns to more precisely control heating and cooling, and Envio Systems, a Berlin-based company that develops sensors to track a building’s use, occupancy and other factors to adjust lighting, cooling and similar energy-related activities.

“Do I need to keep the lights on? Do I need to turn off the air conditioning on floor three because the entire company is working from home this week?,” Ravichandar said. “If you have a system, it is relentless and constantly processing this information.”

Generally, AI building systems learn from historical patterns and the daily habits of occupants to predict and power things on and off. For instance, software and hardware that automatically manages lights, heating and cooling can help buildings cut 20% or more of their yearly energy use.

Nevertheless, hurdles remain to installing more AI systems, including gathering data from a wide range of sources in buildings, such as sensors, which often aren’t interconnected enough. “Retrofitting existing buildings with such sensors and infrastructure, as well as ensuring consistent data quality, can be resource intensive,” Ravichandar said.

Not enough data

AI has big potential to cut the emissions of buildings, but it is only as good as the data it learns from. Only 10% to 15% of buildings have the equipment or systems in place to gather the data needed to support AI, said Thomas Kiessling, chief technology officer of Siemens Smart Infrastructure. “AI in buildings works if you have the data,” he said. “Bad data means you can’t do any kind of schedules, rules or more sophisticated use cases around artificial intelligence. You have to have the data.”

Siemens uses AI to compare one building to a thousand similar buildings to predict what the energy savings could be after an upgrade to a smart-energy management system.

“Even if you just know the address of that commercial building, and maybe you have the energy bill, and maybe you have some high level information of what kind of HVAC brand the building uses, that is these days enough to compile a profile of the building with respect to what is likely you could reap,” Kiessling said.

Otherwise, lower-cost sensors, such as for lighting and cooling, can help save energy for companies that don’t have a sophisticated management system.

Venture-capital firm Fifth Wall’s $500 million fund is focused on decarbonising buildings and invests roughly a third of its money in startups with some kind of AI offering, both in software and hardware, the fund’s co-manager Greg Smithies said. A bigger focus is using more sustainable materials, such as concrete and steel made with renewable energy.

Smithies says AI can help with quickly and cheaply identifying where it makes economic sense to upgrade buildings, fill out permits that vary between countries, draw up mock-ups of designs and come up with chemistry for sustainable materials.

“The main message overall is we’re not going to save the planet with software, and AI is software,” Smithies said. “But AI is an interesting piece of the puzzle.”

IKEA’s experiments with new store layouts produced a surprising result: Shoppers prefer its mazes. The Swedish furniture retailer over the past five years opened new urban stores that diverged from the typical IKEA store experience that guides customers on a winding course through showrooms devoted to different parts of the home. The new locations, located in downtowns of cities across the globe, originally looked more like standard department stores. Shoppers could take any route they pleased through the store and products from different rooms of the home were displayed together. Because the locations stock items more suited for small-space living, selected to appeal to casual shoppers and office workers, IKEA executives thought customers would want to pop in and out without having to take a long path through multiple room sets. In reality, customer interviews and feedback surveys found that many shoppers craved the guiding hand of store design, said Tolga Öncü, head of retail at Ingka Group, which operates the majority of IKEA’s stores . IKEA is consequently redesigning the floor plans and signage of its downtown locations to make them more like those of its out-of-town stores. “We thought we didn’t need to guide the customers because [we thought] the stores are so small we thought they would see everything,” Öncü said. “But it became very clear that [customers thought] ‘No, no, no, this is a big shop!’ ” IKEA declined to discuss sales results at its downtown choose-your-own path stores, but it closed early versions in Madrid, Shanghai and Warsaw, and shut its first U.S. downtown-format store, in the New York borough of Queens, in December, less than two years after it opened, attributing the closure to low visitor numbers. Customers may go to IKEA to buy one thing, Öncü said, but its traditional layout reminds them to buy items they “talked about three weeks ago, but forgot.”

The enduring pathway

IKEA opened its first permanent showroom in Älmhult, Sweden, in 1953, and in 1965 cut the ribbon on its 500,000-square-foot flagship store outside of Stockholm, the largest furniture store in Northern Europe at the time. The Stockholm building’s looping design was partly modeled on New York’s Guggenheim museum and inspired the large, meandering out-of-town stores that IKEA would go on to open around the globe. The stores’ throughway systems that make customers walk around showroom after showroom were originally designed to usher customers through a real-life version of the IKEA catalog, which was introduced before the showrooms. That design principle holds true today, said architectural historian Jeff Hardwick. “The maze ends up being appealing because you’re walking through perfectly crafted 3-D advertisements of your better life, completely immersing yourself in those spaces,” Hardwick said. The layout isn’t universally appreciated . Some shoppers say it takes too long to navigate, and others accuse IKEA of making the route so convoluted that it becomes less of a pathway and more of a trap. IKEA has tried different strategies over the years to remedy these criticisms, with varying results. It began adding shortcuts early in its international expansion so customers could jump ahead faster. Those were well-received by customers, Öncü said. IKEA then tested widening those shortcuts so they looked more like alternative routes. The feedback wasn’t so positive: Wider cut-throughs led customers to accidentally skip whole sections. The standard, narrower versions were reinstated.

Rectifying mistakes

Still, the company thought a maze wouldn’t be necessary when it came to its downtown stores. But it turned out that customers viewed the locations differently than IKEA did. “The first mistake we made was calling them ‘small stores,’” internally, Öncü said. “To [me], they are very small,” but in the eyes of a customer, not so much, he said. IKEA’s new downtown store in San Francisco, for example, covers 52,000 square feet. The average Starbucks , by comparison, is around 1,700 square feet. IKEA realised shoppers missed the maze after speaking with them via stores’ customer feedback programs. The company takes satisfaction surveys, places customer-feedback machines around stores and requires managers to speak to at least 100 customers a week, Öncü said. The overarching sentiment was “This is a big store and I want support” to shop in it, he said. A whittled-down version of the maze was introduced to IKEA’s Vienna and Paris stores in fall 2022 and early 2021, respectively. IKEA said sales are rising across reconfigured downtown stores like those in Vienna and Paris, declining to provide figures. The company is planning for similar adaptations in other existing downtown stores, including those in Mumbai and Stockholm. Its newer downtown stores, such as the one in San Francisco, have been designed with pathways from the start. IKEA doesn’t have to temporarily close stores to add in a walkway, which minimises the costs of rethinking a floor plan, Öncü said. The maze-less experiment also reinforced IKEA’s conviction that people buy more when they are shown more. “I often hear people say, ‘Why is it typical in IKEA that you leave with more than what you had planned to buy?’” Öncü said. “This is the answer to that.”