ZURICH—The chairman of Switzerland’s largest bank received an urgent call last week. On the other end were three top Swiss officials who delivered an ultimatum dressed up as a proposal. UBS Group AG needed to rescue its failing rival, Credit Suisse Group AG.

For any country, it would be a financial emergency. For Switzerland, the stakes verged on existential. Its economic model and national identity, cultivated over centuries, were built on safeguarding the world’s wealth. It wasn’t just about a bank. Switzerland itself needed rescuing.

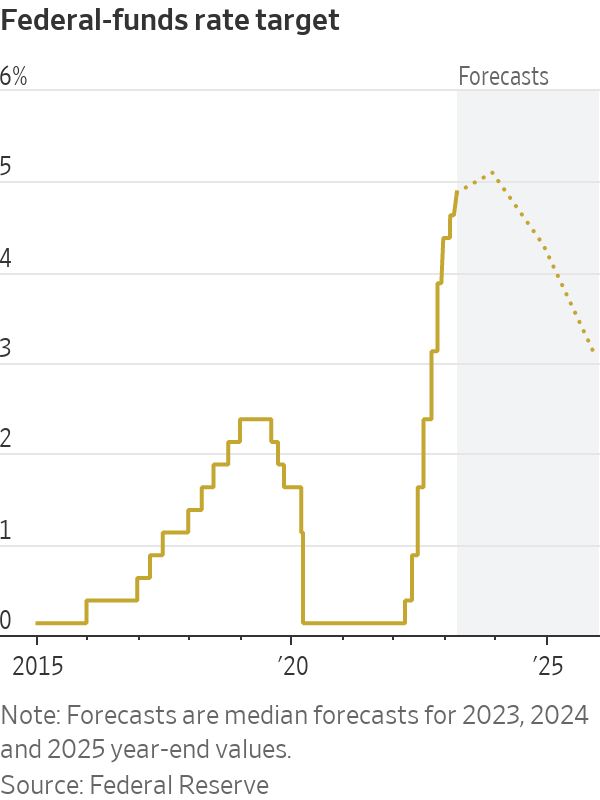

It was Thursday, barely 24 hours into an escalating banking crisis and Credit Suisse was haemorrhaging deposits. The 167-year-old national institution appeared days away from bankruptcy. To keep it alive until the weekend, the central bank was about to quadruple a credit line of more than $50 billion. U.S. and U.K. regulators called their Swiss counterparts to make sure they didn’t let Credit Suisse bring down global markets.

Finance Minister Karin Keller-Sutter, central bank head Thomas Jordan and financial regulator Marlene Amstad had dialled Colm Kelleher, the UBS chairman, to present two options that were really only one: Buy Credit Suisse without a chance to fully understand its vast and complicated balance sheet—or let it fold in a protracted unraveling that UBS’s own executives worried could shatter Switzerland’s credibility as a global banking center.

Over WhatsApp, Swiss diplomats asked each other nervously whether they should move their deposits from Credit Suisse.

After a series of frantic calls and government-orchestrated meetings in Bern, UBS agreed to swallow Credit Suisse for $3.2 billion. To seal the deal, the government, which had vowed after the 2008 crisis never again to use public money to save a bank, hastily used emergency laws to do exactly that.

“Credit Suisse is not only a Swiss company. It is part of the Swiss identity,” said Thierry Burkart, head of the right-wing Liberals party, the country’s third largest. “The bankruptcy of a global Swiss bank would have had an immediate effect everywhere. There would be long and hard reputational damage for Switzerland,” he said.

The swift demise of Switzerland’s second-largest lender has rattled financial markets, and added a global dimension to a banking crisis that broke out on the West coast of the U.S. with the failure of Silicon Valley Bank.

It is still far from clear whether the Swiss have fully contained the damage. Having two world-class banks was seen as a fail-safe to maintain Switzerland’s position in world markets. The forced marriage has left it with one and has shaken ordinary Swiss people and their faith in the country’s economic and political model.

“If Swiss banking means one huge bank, what if something goes wrong with that?” said Mark Pieth, a former head of the Organization for Economic Cooperation and Development’s bribery division who is now at the Basel Institute on Governance. “Then the entire country and its financial stability is at stake. It’s very un-Swiss.”

The central bank and finance ministry, as well as Finma, the top financial regulator in Switzerland, didn’t comment beyond their previous public statements. Bankers and Swiss officials involved in the talks, as well as Swiss and other Western diplomats, provided details of the rescue.

This Alpine nation has seen itself as a special case in Europe: a neutral broker and soberly governed democracy whose banks offer a discreet safe haven to far-flung investors and the world’s wealthy. Its banking system is five times the size of its gross domestic product and larger than in most economies. UBS combined with Credit Suisse has a balance sheet twice the size of the Swiss economy.

For years, Swiss exceptionalism has been chipped away. After 2008, the U.S. enacted laws requiring Swiss banks to transfer information about American clients to the Internal Revenue Service, a hammer blow to its banking secrecy.

Relations with the European Union, whose biggest powers surround the landlocked Alpine nation, are strained after Switzerland walked away from years long talks to bind it more closely to the trading bloc.

It is struggling to defend its 200-year-old policy of neutrality in the face of Russia’s war with Ukraine. Moscow last year put Switzerland on its “Unfriendly Countries List” after the landlocked nation, pressured by its larger neighbours and the Biden administration, joined European Union sanctions against Vladimir Putin and his closest allies.

By the same token, the country has refused to grant permission for Germany, Spain or Denmark to export Swiss military equipment into Ukraine, prompting a debate over whether Switzerland’s attachment to neutrality is damaging its reputation in Europe.

The country—once the indispensable meeting ground where great powers negotiated the end of conflicts—has been sidelined as a mediator in the Ukraine conflict by Turkey. Decades of economic and diplomatic ties to Russia have gone cold in Moscow yet become liabilities within the West.

“We have now a dilemma, a big challenge for Switzerland to be recognised as a strategic partner,” said former Swiss President Micheline Calmy-Rey. “For the time being it is not, and we are in shock.”

The U.S. ambassador last week said Switzerland was facing its most serious crisis since World War II. Foreign investors burned by Credit Suisse’s demise are rethinking their willingness to invest.

“Everything here was avoidable. We were told last week that everything was fine,” said Roger Köppel, editor of the weekly magazine Die Weltwoche and member of the right-wing Swiss People’s Party. “Reality is back and is hitting Switzerland very hard.”

Credit Suisse’s founder, Alfred Escher, was an industrial godfather of modern Switzerland. The businessman and politician used the lender to underwrite Switzerland’s rail lines, tunnelling through the Alps to connect the mountain-encircled nation with the rest of Europe.

Stretching back to Nazi gold, Credit Suisse had harboured money for suspect clients alongside an A-list roster of billionaires, sovereign-wealth funds and families. In a 2014 settlement with the U.S. Justice Department, the bank paid $2.6 billion and admitted its bankers had hand delivered cash and destroyed documents to help Americans hide untaxed wealth.

A banker in London took bribes to make loans in Mozambique. Another forged client signatures and lost them hundreds of millions of dollars. More recently, in 2021, Credit Suisse lost more than $5 billion when family office Archegos Capital Management collapsed, marking the start of its tumble into UBS.

Through the scandals, Swiss banks, and even Credit Suisse, still retained their image as fortresses for the rich.

The latest Credit Suisse management team included several who joined from UBS, including Chairman Axel Lehmann and Chief Executive Ulrich Körner. They made fresh pledges to clean up and saw returning Credit Suisse to health as a form of national service, people familiar with their thinking said.

Even after raising $4 billion capital late last year for a deeper restructuring, Credit Suisse traded at just 20% of its book value. Customers pulled $120 billion from the bank last fall during an internet frenzy over the bank’s health.

Not far from Credit Suisse in central Zurich, executives at UBS prepared just in case they were called on to help. For years, UBS executives and management consultants had mapped out scenarios and what UBS would require from the government, as a precaution.

UBS owed the government. It had been Switzerland’s problem child before.

The result of a merger in the late 1990s between Swiss Bank Corp. and Union Bank of Switzerland, UBS grew rapidly in the banking boom of the 2000s, opening a trading floor bigger than a football field in Stamford, Conn. It needed a Swiss government bailout in the 2008 financial crisis for losses on toxic securities. Chastened, it pulled back from trading and focused on managing wealth.

The Credit Suisse chairman and CEO had feared the call from Swiss authorities.

The bank’s stock had gone into free fall after the chairman of the bank’s biggest investor, Saudi National Bank, speaking in a television interview at a finance conference in Riyadh, said it wouldn’t invest more in Credit Suisse: “Absolutely not,” he said, citing rules on bank ownership, since Saudi National Bank already owned 9.9%.

What the market heard was that Credit Suisse’s largest shareholder wouldn’t back it. Mr. Lehmann, at the same Riyadh conference, rushed back to Zurich. Credit Suisse appealed to the Swiss National Bank and Finma to calm the markets with a message of support.

That Wednesday night, Credit Suisse received a more-than $50 billion liquidity line from the central bank, and the regulators said it met Swiss capital and liquidity requirements.

Credit Suisse customers kept pulling deposits Thursday. Authorities moved to make more than $150 billion in additional liquidity available to the bank, Ms. Keller-Sutter, the finance minister, said. The government didn’t disclose the move, hoping to keep Credit Suisse alive until the weekend, when a permanent solution could be found.

Stung by having to rescue UBS before, Swiss authorities had a plan to handle big banks if they fell under stress. To avoid tapping taxpayer money, the country’s financial regulator would swiftly impose losses as needed on shareholders and bondholders.

That solution was discarded for Credit Suisse, as authorities feared it would cause panic among bank investors around the world, Mr. Jordan, the central bank governor, said Sunday.

UBS Chairman Colm Kelleher got his call Thursday from the Swiss officials, a tripartite representing Finma, the Swiss National Bank and the finance minister. The message was clear: UBS would take over Credit Suisse, or the latter would go bankrupt, potentially bringing down UBS and other banks in the fallout.

Irish-born Mr. Kelleher joined UBS as chairman in April, after a long career at Morgan Stanley, including as chief financial officer in the 2008 financial crisis. His team swung into action, helped by a blueprint developed under former UBS Chairman Axel Weber on what a combined UBS-Credit Suisse could look like.

The UBS and Credit Suisse chairmen and CEOs had a quick meeting with the finance minister Friday at UBS, where they were told they would sign a deal by Sunday.

Credit Suisse’s large shareholders in the Gulf, including Saudi National Bank, worried they were about to lose their entire investment. They called Swiss officials, including the central bank governor and government ministers, and wrote letters, arguing that their rights were at risk of being trampled on, and that they might be able to come up with a better deal.

On Saturday evening, Mr. Kelleher took a break from dinner to call Mr. Lehmann with a $1 billion offer. It was less than Saudi National Bank’s investment for one-tenth of the bank in November, a deal Mr. Lehmann brokered.

On the Credit Suisse side, executives fretted whether they could get a deal through their shareholders. A quarter of the shares were held by a trio of Gulf investors. The government had a solution. It passed a law that allowed a deal to pass without a shareholder vote. A government official read out the new law to Credit Suisse executives, without giving them it in writing, according to people familiar with the matter.

Sunday morning, the Gulf shareholders Qatar Investment Authority and Olayan Group, and the Saudi Public Investment Fund, part-owner of Saudi National Bank, made a last-ditch proposal to Credit Suisse’s board. They would inject around $5 billion, keep the stable Swiss bank and sell off other parts over time.

Mr. Lehmann put a call into the Swiss finance minister. UBS is the only option, he was told, and the line went dead.

Swiss officials from the get-go would only consider a Swiss option to save Credit Suisse, people familiar with the matter said. They shot-down an informal approach from U.S. asset management giant BlackRock, Inc. to get involved, these people said.

Credit Suisse’s board dug in its heels on the low price. With the announcement hours away, Swiss officials told UBS to try harder.

Late Sunday afternoon, UBS agreed to lift its offer and pay a little over $3 billion—less than half Credit Suisse’s market value on Friday. Crucially, Swiss regulators would write off $17 billion on the riskiest type of Credit Suisse bonds. The market for these bonds, commonly issued by European banks, was severely hit Monday. UBS would also get a more than $200 billion liquidity line from the central bank, and a government guarantee of over $9 billion against some potential losses.

To get the deal done, the government waived antitrust laws on the grounds that financial stability was at stake.

“Any other solution would really have triggered a financial crisis,” said Ms. Keller-Sutter, the finance minister.

At a Sunday news conference announcing the deal, Mr. Kelleher said UBS buying Credit Suisse was in the best interest of Switzerland.

—Ben Dummett, Julie Steinberg and Summer Said contributed to this article.