While property values are rising strongly in mostmarkets across Australia, it’s a vastly different story in Victoria and Tasmania, new data from CoreLogic shows. Over the 12 months to May 31, the median house price lifted just 1.8 percent in Melbourne and fell0.6 percentin regional Victoria. The median dipped 0.1 percentin Hobart and ticked 0.4 percent higher in regional Tasmania. This is in stark contrast to Perth, where values are up 22 percent, and regional Western Australia, up 14.8 percent; as well as Brisbane, up 16.3 percent, and regional Queensland, up 11.8 percent.

CoreLogic Head of Research, Eliza Owen says an oversupply of homes for sale has weakened prices in Victoria and Tasmania, creating buyers’markets.

“On the supply side, there has been more of a build-up in new listings than usual across Victoria, even where home value performance has been relatively soft,” Ms Owen said. “Victoria has also had more dwellings completed than any other state and territory in the past 10 years, keeping a lid on price growth.The additional choice in stock … means vendors have to bring down their price expectations, and that brings values down.”

Melbourne dwelling values are now four percent below their record high and Hobart dwelling values are 11.5 percent below their record high. Both records were set more than two years ago in March 2022. The oversupply has also affected how long it takes to sell a property. The median days on market is currently 36 in Melbourne and 45 in Hobart compared to a combined capitals median of 27. It takes 55 days to sell in regional Victoria and 64 days in regional Tasmania compared to a combined regional median of 42 days.

Changes in population patterns have also contributed to higher numbers of homes for sale in recent years. Since COVID began in early 2020, thousands of families have left Melbourne because working from home meant they could buy a bigger propertyin more affordable areas. While many relocated to regional Victoria, a significant proportion left the state altogether, with South-East Queensland a favoured destination. Meantime, Tasmania’s surge in interstate migration during FY21 was short-lived. Data from the Australian Bureau of Statistics shows the island state has recorded a net loss of residents to other states and territories every quarter since June 2022.

Record overseas migration has more than offset interstate migration losses, thereby keeping Victoria’s and Tasmania’s populations growing. However, the impact of migrants on housing is largely seen in the rental market, so this segment of population gain has done little to support values. Growth in weekly rents has been far stronger than growth in home values over the past year, with rents up 9 percent in Melbourne and 4.8 percent in regional Victoria, and up 1 percent in Hobart and 2.7 percent in regional Tasmania.

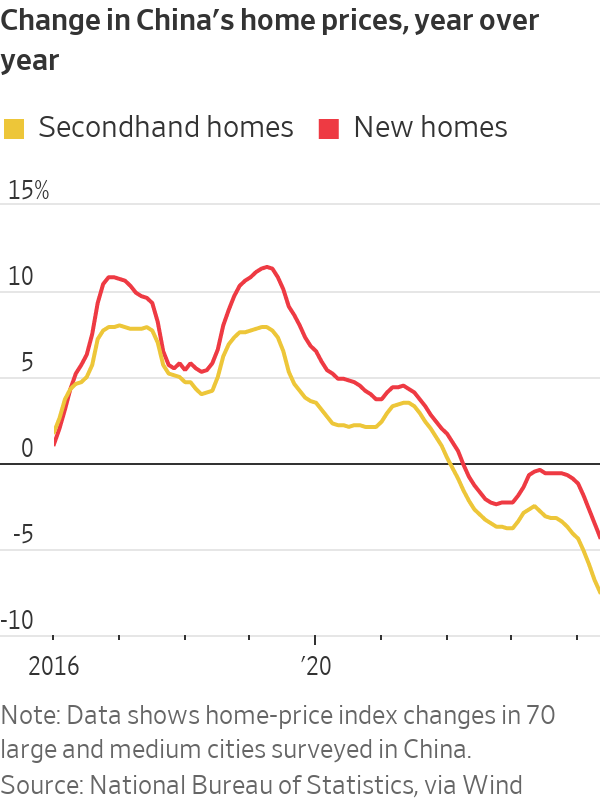

China’s broken housing market isn’t responding to some of the country’s boldest stimulus measures to date—at least not yet.

The Chinese government has been stepping up support for housing and other industries in recent months as it tries to revitalise an economy that has continued to disappoint since the early days of the pandemic.

But fresh data for May showed that businesses and consumers remain cautious. Home prices continue to fall at an accelerating rate, and fixed-asset investment and industrial production, while growing, lost some momentum.

“China’s May economic data suggest that policymakers have a lot to do to sustain the fragile recovery,” Yao Wei, chief China economist at Société Générale, wrote in a client note on Monday.

The worst pain is in the property sector, which has been struggling to deal with oversupply and weak buyer sentiment since 2021, when a multiyear housing boom ended . The market still doesn’t appear to have found a floor, even after Beijing rolled out its most aggressive stimulus measures so far in mid-May in hopes of restoring confidence.

In major cities, new-home prices fell 4.3% in May compared with a year earlier, worse than a 3.5% decline in April, according to data released Monday by China’s National Bureau of Statistics. Prices in China’s secondhand home market tumbled 7.5%, compared with a 6.8% drop in April.

Home sales by value tumbled 30.5% in the first five months of this year compared with the same months last year.

“This data was certainly on the disappointing side and may ring some alarm bells, as May’s policy support package has not yet translated to a slower decline of housing prices, let alone a stabilisation,” said Lynn Song, chief China economist at ING.

Economists had also been hoping to see a wider recovery this month after Beijing started rolling out a planned issuance of 1 trillion yuan, the equivalent of $138 billion, in ultra-long sovereign bonds in May. The funds are designed to help pay for infrastructure and property projects backed by the authorities. Investors gobbled up the first batch of these bonds.

Monday’s bundle of economic data, however, underlined how the country still isn’t firing on all cylinders.

Retail sales, a key metric of consumer spending, rose 3.7% in May from a year earlier, compared with 2.3% in April, according to the National Bureau of Statistics. While the trend is heading in the right direction, it is still a relatively subdued level of growth, and below what most economists believe is needed to kick-start a major revival in consumer spending.

The expansion in industrial production—5.6% in May compared with a year earlier—was down from April’s 6.7% increase. Fixed-asset investment growth, of which 40% came from property and infrastructure sectors, also decelerated, to 3.5% year-over-year growth in May from 3.6% in April.

Key to the sluggish economic activity data in May—and China’s outlook going forward—is the crisis in the property market, which has proven hard for policymakers to address.

The property rescue package in May included letting local governments buy up unsold homes, removing minimum interest rates on mortgages, and reducing payments for potential home buyers. It also included as its centrepiece a $41 billion so-called re-lending program launched by the People’s Bank of China, which would provide funding to Chinese banks to support home purchases by state-owned firms.

The hope was that by stepping in as a buyer of last resort for millions of properties, the government would manage to mop up unsold housing inventory and persuade wary home buyers to re-enter the market. In turn, Chinese consumers, who have most of their wealth tied up in real estate, would feel more confident about spending again, thereby lifting the overall economy.

But the size of the re-lending program wasn’t big enough to convince home buyers, said Larry Hu , chief China economist at Macquarie Group. “Meanwhile, their income outlook also stays weak given the current economic condition,” he said.

For the property market to bottom out and reach a new equilibrium, mortgage rates, which stand at around 3-4% in China, need to be as low as rental yields, which are currently below 2% in major cities, said Zhaopeng Xing, a senior China strategist at ANZ. He said that a large mortgage rate cut will need to happen eventually.

The other key part of China’s push to revive growth revolves around the manufacturing sector, with leaders funnelling more investment into factories to boost output and reduce the country’s reliance on foreign suppliers of key technologies.

The result has been a surge in production. But with domestic consumption not strong enough to absorb all those goods, many factories have been forced to cut prices and seek out more overseas buyers.

Data released earlier this month showed that Chinese exports rose faster in May than the month before.

However, the export push is butting into resistance as governments around the world worry about the impact of cheap Chinese competition on domestic jobs and industries. The European Union last week said it would impose new import tariffs on Chinese electric vehicles, describing China’s auto industry as heavily subsidised by the government, to the point where other countries’ automakers can’t fairly compete.

The U.S. has also hit Chinese cars and some other products with hefty duties, while countries including Brazil, India and Turkey have opened antidumping investigations into Chinese steel, chemicals and other goods.

Beijing says such moves are protectionist and that its industries compete fairly with global rivals.

Saudi Arabia’s fledgling advertising industry and continued growth in the sector in the United Arab Emirates are helping to make the marketing business in the Middle East the fastest-growing in the world.

Ad spending in the Middle East is projected to increase 8.1% to $6.6 billion this year, up from 3.5% last year, according to advertising research firm WARC.

That expansion is building from a much smaller base than in many other ad markets. The Netherlands alone will generate $6 billion in ad spending in 2024, up about 2.3%, WARC said. But it is also enough to outpace every other region in 2024, the firm said.

“It reminds me almost of the gold rush,” said Reda Raad , chief executive of TBWA\Raad Group, an ad agency based in Dubai, in the United Arab Emirates, that is part of the U.S.-based ad holding company Omnicom Group . “I don’t think we’re going to see this type of growth again in our lifetime.” TBWA\Raad has won eight new clients over the past year, with an increase in head count of 17% to accommodate the new work, Raad said.

Some international brands have long maintained a presence in the region. PepsiCo has considered the area a strategic market for decades, said Karim Elfiqi , senior vice president and chief marketing officer at PepsiCo Africa, Middle East and South Asia. Sponsorship deals with local stars such as Mohamed Salah , a soccer player from Egypt, “are a testimony of how over time, we have been part of the cultural fabric of the region,” Elfiqi said.

Other major brands have formed a more recent focus on the Middle East. The Lego Group opened a Middle East and Africa headquarters in Dubai in 2019, citing the size of the region’s young population. That office has developed work such as a Ramadan-themed campaign that ran in the U.A.E. and Saudi Arabia, among other locations.

‘Massive growth’

The Middle East’s ad market has lagged behind regions such as North America and Europe partly because of stricter cultural norms and regulations that affected business, as did a more limited media landscape and economic instability, according to Raad.

But marketing growth in the region is now being driven in part by newfound marketing interest in Saudi Arabia, where ad spending this year is expected to reach $2.1 billion, nearly double its level in 2019, according to WARC. Growth is also coming from the U.A.E., whose ad market is expected to reach $1.7 billion in 2024. Smaller contributors include Qatar and Kuwait.

The landscape has changed now because of economic diversification, increased connectivity and a move into the digital world, leading international brands to enter and invest in campaigns tailored to the region, Raad said.

Four years ago, Saudi Arabia made up a small proportion of business at Lightblue, a creative experience and tech agency based in Dubai. These days, 40% of its business comes from the country, says co-founder David Balfour , who opened an office in Riyadh last month as a result.

“The conversation used to be, ‘We’re going to do this in Dubai.’ Now, it’s ‘We’re going to do this in Dubai—and in Saudi.’” Balfour said. “We’re seeing massive growth in that region.”

There have been speed bumps. As government spending reaches huge levels , Saudi Arabia experienced a rare economic contraction in 2023.

But the country’s efforts to expand its economic pursuits beyond oil have led to the creation of new brands, which are seeking the help of marketing agencies to get the word out.

Marketers in the region are seeking help to stay on-trend in areas such as generative artificial intelligence and social media, said Greg Paull , principal of R3, a consulting firm that helps match advertisers with agencies.

“U.A.E. has been a magnet for the region for 20 years as more investment has come in—but with the new leadership in Saudi since 2017 [when Mohammed bin Salman was named crown prince ], this market has gone through remarkable growth,” Paull said.

Saudi Arabia has faced criticism for its human-rights record under the crown prince, the day-to-day ruler of the kingdom, especially over the 2018 killing of dissident journalist Jamal Khashoggi and the more recent jailing of women’s rights activists.

Mohammed has outlasted the international isolation that followed Khashoggi’s killing, however, and continues to pursue an economic diversification plan dubbed Vision 2030. The country last year unveiled plans for a new international airline called Riyadh Air, is investing billions of dollars to build its tourism and videogame industries, and in March hosted a golf tournament in Jeddah under the auspices of LIV Golf, the Saudi-backed league that has both challenged the PGA Tour and struck a deal to unify with it.

Changing tides

Vision 2030 also calls women’s empowerment a top social priority and seeks to increase the country’s employment rate of women.

Nada Hakeem , CEO and co-founder of Saudi creative agency Wetheloft, said the perceptions of hardships for women in the marketing and advertising industry are outdated and inaccurate.

“As a Saudi woman who founded my company in 2012, I’ve always felt supported by the creative community and the industry as a whole,” Hakeem said. “While every society may have its challenges, I can confidently say that these challenges have not hindered our growth.”

A progression of new laws, policies and incentives are making the industry in Saudi Arabia more inclusive and supportive for women, she added.

In certain parts of the Middle East, “absolutely, it’s still challenging, but they are making the right strides, and they have the right quotas and ambitions in place,” said Rebecca Bezzina , CEO for the EMEA region at R/GA, an agency owned by Interpublic Group of Cos.

“They’ve got wealth, they’ve got world-class ambition, world-class budget. They’re not shy of doing things in the right way,” Bezzina added, speaking of the region overall. “But they still have a talent shortage, especially from a creative and design and product point of view. So often what we’ve found our success has been that they’ve come to us and said, ‘Oh, we want a world-class agency to help us launch this new venture or do this new brand.’”

R/GA said it sees 69% more requests for agency work from marketers in the region today than it did five years ago. It recently handled a brand redesign for Banque Saudi Fransi, which wanted to reaffirm its Saudi roots with a modern identity, and created Weyay, the brand for a new digital bank from the National Bank of Kuwait.

The agency hasn’t notably increased its regional workforce, but it has made changes to facilitate working across Europe and the Middle East.

Other Western players are making moves to capture a piece of the growth. Advertising giant WPP has long worked in Saudi Arabia through units such as Ogilvy and GroupM, but in 2021 established a joint venture with a local company to create ICG Saudi Arabia, a communications and media company based in Saudi Arabia. Ad holding company Stagwell opened new offices for its media agency Assembly in Riyadh in 2021 and in Cairo in 2022.

Regional hospitality

Some executives said certain facets of business dealings in the Middle East are different than in other parts of the world.

Bertrand Morin, a group account director for R/GA who is based in London and works often with Middle Eastern clients, said he spends much more time speaking about personal lives and families with those clients than those in the U.K. or U.S. He has been invited to Middle Eastern clients’ homes to join their families for dinner, something that has never happened with clients elsewhere.

But others say it can feel surprisingly familiar.

Balfour, the Lightblue co-founder, said he was struck by the number of ad-agency workers recently having dinner at the Riyadh location of steakhouse chain Beefbar, and the scene’s similarity to far-off locations.

“The staff are from everywhere in the world. The service and the food is unbelievable. There’s a DJ playing,” Balfour said. “Apart from not having alcohol, you could be anywhere in the world.”

A versatile stool with a sense of fun took out the top prize at the Australia’s Next Top Designers awards at Design Show Australia last week.

The ‘Cheeky’ stool designed by Maryam Moghadam was the unanimous winner among the judging panel, which included Kanebridge Quarterly magazine Editor in Chief, Robyn Willis, Workshopped Creative Director Olaf Sialkowski, Design Show event organiser, Andrew Vaughan and Creative Director at Flexmirror Australia, Matt Angus.

Designed as an occasional stool or side table, the Cheeky stool comes in a range of skin tones. The judges applauded its commercial applications, its flexibility to work in a range of environments, and its sense of play.

In accepting the $10,000 prize, designer Maryam Moghadam quipped she was pleased to see ‘other people find bums as funny as I do’. A finalist at last year’s awards, Moghadam will put the prize money towards bringing her product to market.

Winner Maryam Moghadam said the $10,000 prize money would be put towards developing her product further for market.

Australia’s Next Top Designers is in its fourth year, but this is the first year a cash prize has been offered. Kanebridge Quarterly magazine has put up the prize money to support the next generation of emerging industrial design talent in Australia.

Editor in Chief Robyn Willis said the cash prize offered the winner the opportunity to put the money towards whatever aspect of their business it would most benefit.

“That might be prototyping their product further, spending on marketing, or simply paying for travel or even childcare expenses to allow the designer to focus on their work and take it to the next stage,” she said. “We’re thrilled to be supporting this design program and nurturing emerging design in a very practical way.”

The Coralescence lamps from the Tide Pool series by Suzy Syme and Andrew Costa had strong commercial applications, the judges said.The Mass lamp by Dirk Du Toit is crafted from FSC-certified oak or walnut.

Two finalists were also awarded ‘highly commended’ by the judges — Mass lamp by Dirk Du Toit and the Coralescence lights from Suzy Syme and Andrew Costa at Tide Pool Designs. The judges agreed both products were beautifully resolved from a design perspective, as well as having strong commercial applications in residential and hospitality design.

We don’t want to be friends with our co-workers . We don’t want to help out with that project. We don’t trust the CEO…or our boss…or that guy in accounting.

Have we taken our cynicism at work too far?

In some ways, our bad attitude makes sense. Many of us made work our church, only to end up laid off , burned out or underpaid. Now we check out, do less, gossip and snark.

It isn’t getting us anywhere good, according to Jamil Zaki , a Stanford University psychology professor who runs the school’s social neuroscience lab.

“Cynicism, if it were a pill, would really be a poison,” he says.

Zaki has spent years researching sunny concepts such as empathy and compassion. One of his studies, for example, found that giving away money activates a similar part of the brain as eating chocolate. His forthcoming book, “Hope for Cynics,” explores the rise of our darker sides, our belief that other people are selfish, greedy and dishonest.

Betrayed once, we practice what Zaki calls “pre-disappointment,” always assuming others will let us down. The mindset feels productive and cunning, like we’ll be able to protect ourselves. But Zaki says it can actually stunt our careers in the long run, and hurt our mental and physical health.

“By never trusting, cynics never lose,” he writes. “They also never win.”

He assures that you don’t have to become the company cheerleader, or even an optimist, to grow your faith in other people. You do have to take a chance on them, examining your own assumptions and suspending your conviction that you already know how this is going to turn out (not well).

While the approach might initially seem blasphemous to the more negative, sarcastic and skeptical among us—like, say, me—anyone can become less cynical , he says.

You might even find you like it.

How we got here

Once upon a time, Americans were less cynical, Zaki says. A longstanding survey from research organisation NORC at the University of Chicago, which has examined American attitudes since 1972, shows we used to trust each other more. Around the middle of the last century, many hummed along on the rosy glow of plum benefits, robust job security and the knowledge that the chief executive was making, say, 20 times a worker’s pay, instead of 200.

It isn’t that we never complained about work, but Zaki says we repaid our companies’ loyalty with commitment, as part of an unspoken covenant.

Today, that employee-employer pact can feel like a relic of a bygone era. Workers have swapped pensions and equity in their companies for more meagre benefits that put the risk and onus on individuals. Instead of reporting to paternalistic employers, many people now operate under tenuous contracts and gig work.

Some of us work from home in isolation or spend lonely days in the office trapped on back-to-back video calls. There’s less chitchat, less interaction.

“We don’t like people when they’re abstracted,” Zaki says, “but we love people who we actually know.”

Zaki understands why, given all this, we might scoff at the notion that our company is a family, or roll our eyes at the prospect of joining in forced fun at the office happy hour.

Sometimes, I suspect, we also adopt a toughness because we don’t want to look like we’re trying too hard, only to fail or be rejected. Maybe it stems from perfectionism, or anxiety, or insecurity after being exposed to everyone else’s highlight reel on social media for the past 15 years.

Fighting our own worst tendencies

It might seem like all the office snakes are scaling the ladder, but Zaki says studies show cynics’ earnings and leadership potential level off with time. To do good work and attain success, you have to build alliances and share information. Translation: You have to trust someone.

Cynics are prone to poor health, from depression to heart disease, he says, adding that at an organisational level, cynicism can lead to pervasive backstabbing, higher turnover and even corporate corruption.

Cynicism is also a self-fulfilling prophecy, he says. People often mirror how we treat them. Micromanage your team—surveilling them and wresting away their ability to make decisions—and they’ll become the slackers you think they are, doing the bare minimum and buying mouse jigglers to mask time away from their home computers.

“Cynics tell a story full of villains and end up living in it,” he writes.

Resisting cynicism’s pull starts with being open-minded. Examine the data of your life like a scientist would, he says, instead of jumping to conclusions, positive or negative. Think everyone at your job is out for themselves? Ask 10 colleagues for a favour, and see if anyone agrees to help. Convinced every conversation with a co-worker will be painful? Spend a day rating your interactions with them on a scale from 1 to 10.

Challenging your assumptions will leave you pleasantly surprised, Zaki promises, because people often rise to the occasion when we let them. You can start by doling out what you hope to receive. Try engaging in “positive gossip,” speaking highly of others. Take a leap of faith in someone, and do it obviously.

“I trust you,” a manager might say to her direct report. “I really think you can do this.”

Calibrating our hope

Could all this make us too soft? Rejecting cynicism doesn’t mean you can’t hold workers to high standards, Zaki says. Just don’t pit them against each other, with practices like stack rankings, where collaboration is discouraged as workers try to claw above each other on a scoreboard.

Your humour can still be irreverent, even biting, he adds, but jokes should ultimately bring people together or improve something.

“Snark, in the absence of any hope, kind of curdles,” he says.

And don’t be blindly optimistic, he adds. If leadership isn’t giving you any reason to have faith in them, don’t. Find another group to trust—maybe your small team or a union. Band together to provide a buffer to the daily stress of working in your organisation, or enact change by fighting for something better.

“We often underestimate how much influence we have,” he says. “Own that power.”

Apparel retailers are discovering that weight loss is their gain.

While blockbuster drugs like Ozempic that lead to significant weight loss have dented demand for diet plans and caused food companies to prepare for people eating less, clothing sellers are finding that millions of slimmed-down Americans want to buy new clothes.

The newly svelte aren’t just restocking their wardrobes, many are also gravitating to more body-hugging shapes and risqué designs, according to industry executives and shoppers. Some brands are responding by replacing zippers with adjustable corsets and adding more sheer looks.

The nascent downsizing is happening across brands and types of garments. Industry executives said that they can’t be certain weight-loss medicine is the cause, but added that the shift is unlike anything they have seen. It is also an about-face from recent years, when many retailers rushed to add larger sizes to accommodate Americans’ growing girth.

About 5% of Lafayette 148’s customers are buying new outfits because they have lost weight, often replacing their size 12 clothes with size 6 or 8, according to Deirdre Quinn , the brand’s chief executive. The benefit is twofold; in addition to boosting sales, Lafayette 148 is saving money because smaller sizes use less fabric, Quinn said.

More customers of clothing rental company Rent the Runway are switching to smaller sizes than at any time in the past 15 years, said Jennifer Hyman , co-founder and CEO. These customers are also showing more of a willingness to experiment with different styles such as cutouts and other body-baring features. “When you are more comfortable in your skin, you are more willing to try edgier looks,” she said.

For Maggie Rezek, getting dressed used to be about hiding her extra weight in oversize shirts and baggy pants. Since she lost 60 pounds on semaglutide, the active ingredient in Ozempic, the 32-year-old, who handles marketing for a beauty salon, has splurged on a new wardrobe. Now, her staples consist of crop tops and jean shorts. She has traded in her sneakers for kitten heels. She even documents her outfits on social media.

“Before, I was insecure about my body,” said Rezek, who lives in Indianapolis. “Now, I feel like I fit better in clothes. That gives me the confidence to dress up and be more stylish.”

Some 15.5 million people, or 6% of U.S. adults, say they have tried injectable weight loss drugs to slim down, according to a survey of more than 5,500 Americans conducted in March by polling company Gallup. Nearly three-quarters of current users said the drugs—a class known as GLP-1 that were originally developed to treat diabetes—are effective or extremely effective in helping them shed pounds.

Weight-loss drugs don’t work for everyone and the cost can sometimes exceed $1,000 a month, limiting the market. The full price isn’t always covered by insurance. Moreover, people struggle to keep the weight off once they stop using the drugs.

Still, some companies expect the market for these drugs will be big enough that they are shifting course. WW International , formerly known as Weight Watchers, acquired a subscription service that offers telehealth visits with doctors who can prescribe drugs like Ozempic. Nestlé is introducing a new food line this year designed for people taking weight-loss medication.

Clothing companies could use a boost. Apparel sales fell 4% in the 12 months that ended in April compared with the same period a year earlier, according to market research firm Circana, as people give priority to their spending on necessities.

Coming out of the Covid-19 pandemic, Amarra, which sells evening gowns and other formal wear in 800 retailers in the U.S., Canada and Australia, saw increased demand for larger sizes. Now, that trend has reversed.

“Over the past year, our retailers have been telling us they need smaller sizes,” said Abhi Madan, Amarra’s co-founder and creative director. Amarra, which is based in Freehold, N.J., has added sizes as small as 000. He says he is also selling more sizes in the 0-8 range and fewer in the plus-size range of 18-24.

Madan said the shift is changing the way Amarra designs dresses. It is replacing zippers with lace-up corsets, which can more easily accommodate shifting weights because the laces can be tightened or loosened. It is also adding more sheer side panels that give a figure-hugging look.

AllStar Logo, which sells polo shirts, fleece jackets and other gear to large companies, has seen demand for its largest sizes fall by half over the past year, according to Edmond Moss , its sales director.

“We used to sell a lot of fleece jackets in extra, extra large,” Moss said. “Now everything has gone down by at least one size.”

Sales of the three largest sizes of women’s button-down shirts fell 10.9% in the first three months of 2024 compared with the same period in 2022 at a dozen brands, according to Impact Analytics, which helps retailers manage their inventory and size allocations.

Sales of those same button-down shirts in the three smallest sizes grew 12.1% over that period. Impact Analytics analysed purchases in physical stores located on Manhattan’s Upper East Side. It focused its research on this area because it has the highest concentration of individuals in New York City taking these drugs specifically for weight loss, according to market research firm Trilliant Health.

A similar trend played out for women’s dresses and sweaters, as well as men’s polo shirts, sweatshirts and T-shirts, according to Impact Analytics.

Prashant Agrawal , Impact Analytics’ founder and CEO, said it wasn’t possible to know if the size changes resulted from people losing weight or a shift in clothing styles, but added that such a pronounced shift is unusual. “It’s not something we’ve seen before,” he said.

Some executives are worried that the shift could reduce demand for plus-size clothes.

“I’m trying to figure out what we have to worry about in the future,” said Doug Wood , the chief executive of clothing retailer Tommy Bahama, noting that as more people lose weight it could hurt sales of its “Big & Tall” collection designed for very large men.

Jillian Sterba went from a size 6 to a size 10 after the birth of her child. When the weight didn’t come off with diet and exercise, she started injections of semaglutide in October. Since then, Sterba, who is 36 and lives in Austin, has lost 35 pounds. She is now a size 4. “Almost half my clothes are not wearable,” she said.

She bought new jeans, tops, bras and underwear. “I had been wearing flowy tops before but now I’m wearing fitted shirts,” she said. Still, Sterba said she is keeping 80% of her old clothes just in case she gains back the weight.

My memory of when I first learned about stocks is fuzzy. I was in my early 20s, and my mother sat me down at our kitchen table, helped me open a brokerage account, and showed me how to buy and sell on the platform. The lesson I walked away with: Tread carefully, invest only “play money,” not money you need to survive, and only target companies that sell resources.

I also thought: This is too risky; I’ll never touch this account.

Years later, I still approach stocks with trepidation—no doubt coloured by that 30-minute conversation with my mom.

As I’ve talked to my family and friends, I realize that so much of what we know about personal finance—how we invest, how we spend—comes from our parents.

“We get our money personalities from our childhood,” says financial planner Angela Dorsey of Dorsey Wealth Management. “So if in our childhood there was a lot of hesitancy around it, then that shapes how you feel about money and taking calculated risks.”

Learning by watching

Sometimes, these lessons are learned through specific conversations, like the one I had with my mother. But more often than not, they come simply through observing. In fact, Dorsey says that many of her clients don’t have any money conversations with their parents. “It comes from seeing what happened to their parents, seeing what happened to their uncle,” she says. “A lot of times, they’re not even aware of it.”

But that lack of awareness comes with a price: When people don’t know where their money habits come from, they can often undermine good intentions. You may want to invest and spend wisely, but these unconscious, ingrained tendencies can create financial problems down the road. So it’s useful to uncover those unspoken lessons, and figure out which ones serve us well—and which ones don’t.

To expose those habits, Dorsey offers her clients a money-personality quiz, which can unveil attitudes about money developed from childhood. So I decided to take one. For good measure, I had my sister take it as well.

Both of us ended up falling into the “Bon vivant” pool—with traits like “Workaholics with long hours” and “Spends money on anything that saves them time.” Our issues? “Ad hoc investments,” “Panic with market ups and downs,” and “Confuse hobbies with investments.” (We both really felt that last one.)

Looking back, the traits that mark my financial personality are pretty much the same traits that my parents had. They worked long hours. They did give priority to spending on things that saved them time. They were happy to buy me new books or help me tackle a new hobby or skill. New clothes or makeup? Not so much.

Unlearning some lessons

Friends I spoke with mostly echoed what my sister and I experienced. While their parents might not have given them specific advice, they did influence their spending and budgeting tendencies just by being who they were.

“I didn’t get any money lessons from my parents, but I certainly picked up habits,” a former co-worker told me. “I saw my dad pack lunch every day for work, so I pack lunch every day for work now.” This friend was particularly thrifty in my years working with her, primarily using a debit card so as to not carry debt and eating her packed lunches as the rest of us spent $15 on salads and sandwiches.

She now has a credit card, but to this day she’d rather cobble together a lunch of office snacks than go out to buy lunch. “It has helped me in the long run because it keeps a baseline of healthy spending habits,” she says. She prefers meals out as a conscious choice for special occasions, rather than a standard practice.

Another friend watched how his parents, who were small-business owners, scrimped and saved at home. He summed up what he learned from that in three bullet points:

He says he is now trying to loosen up and feel comfortable spending some of his hard-earned money to improve his quality of life, especially as he has become more successful in his career.

This is a common lesson Dorsey says she teaches her clients to unlearn. “It’s really interesting how frequently I run into situations where they have enough, but when it comes time to spending, they’re terrified,” she says. “And so I have to tell them, ‘You have my permission to spend your money.’ ”

On the brink of burnout

For my part, I’ve certainly benefited from watching my parents’ work ethic over the years. Doing so gave me the drive to establish my own career goals. Seeing their productivity inspired my own. But in the past few years, I’ve found myself on the brink of burnout—both at work and with all my extracurricular activities.

That has led me to the realization that my work and personal lives could actually benefit more from me enjoying my weekends, and not always packing them full of events or extra work. I now know that it’s just as important to step back from things and take a moment to recharge as it is to charge ahead. And my wallet would certainly appreciate buying less crochet yarn and concert tickets.

Mostly, though, I’ve had to work to get over my stock-market fears. My mother sitting down to explain how the market works was more than what some of my friends learned from their parents. But while it was a well-intentioned lesson, it didn’t have the desired effect at the time.

As a more fully-formed adult, I began to rethink that conversation. And thanks to my colleagues and my friends, I’ve started to put money into something beyond a basic savings account. I began contributing to a Roth IRA after a friend explained the tax benefits. A former boss clued me into high-yield savings accounts. A colleague encouraged me to invest—but in more-diversified ways, such as ETFs.

And I finally logged into that brokerage account my mother helped me open. While I still veer toward the more risk-averse side, following my mother’s cautious footsteps, learning more on my own has allowed me to think of investing as a way to make my savings grow, not just a way to experiment with “play money.”

In the end, sometimes the most well-intentioned parental lessons backfire. One friend invested in specific mutual funds that his father recommended. But those mutual funds didn’t do well and started dropping in value. So when my friend was later eligible to contribute to his employer-sponsored retirement account, he chose not to—feeling burned by those earlier losses. Instead, he used his extra money to be able to live without a roommate.

While my friend eventually ended up contributing to a retirement plan, he says the earlier experience taught him that sometimes you just need to “reject the things your parents tell you to do.”

The DBX, in base or 707 form, is certainly practical for everyday activities.

It’s a two-row SUV whose rear passengers enjoy plenty of legroom, separate climate controls, and heated seating. Although the carbon ceramic brakes are standard, lifestyle options include accessories for transporting pets and “event seating” to enjoy tailgate parties. The latter are amenities once seen only in the popular Range Rover—a car that now has a lot of competition.

“The average mileage driven in our SUVs is two to three times that of the sports cars we sell,” says Alex Long, a product and strategy executive at Aston Martin, which was presenting its upgraded 2025 DBX 707 in Edinburgh earlier this month. “It’s a huge ‘conquest’ car, meaning that three-quarters of the initial buyers were new to the brand. Previously they might have said, ‘I love Aston Martin, but the cars aren’t practical for me.’”

The DBX 707s at Scotland’s famed Gleneagles golf resort. Jim Motavalli

The redesigned interior on the test car was a riot of red leather, even on the hand holds. Carbon fibre, in a process co-developed by Aston, is mostly decorative on the interior, though it’s employed for lightness in the tailgate and tailgate surround. The car lacks a head-up display, but it has just about every other modern amenity, including Apple CarPlay and an (optional) 23-speaker, 1,600-watt Bowers & Wilkins sound system that is new in the 2025 model. There is a 12.3-inch instrument cluster and a 10.25-inch central display. The bottom line for the 707 is US$249,000, putting it considerably below Rolls-Royce Cullinan territory (that one starts at US$392,000). Deliveries began in the second quarter of this year.

At the wheel of the DBX 707 in right-hand drive form Aston Martin photo

The power comes from a four-litre, twin-turbo V8 obtained from Mercedes-AMG. The output is 697 horsepower and 663 pound-feet of torque, shifted by an also-Mercedes-derived nine-speed wet-clutch automatic. The bulk of the time you’re in rear-wheel drive, but power is directed to the front axle as needed, and the DBX is a capable off-road performer. Americans will also want to know that despite being derived from a long line of two-seat sports cars, the DBX can haul nearly 6,000 pounds.

Big V8s can move a lot of weight, and despite its 4,949 pounds the DBX 707 can reach 60 miles per hour in 3.1 seconds and attain 193 mph.

More than half of Aston’s current sales are of the DBX SUV, and even in Scotland—where the small car used to reign supreme—it’s apparent that the SUV is taking over the roads, Long says. North America is Aston’s biggest market, accounting for 35% of sales.

Inside the DBX 707. Jim Motavalli photo

The DBX was launched in 2020 and the upmarket 707 in 2022. The platform is not used on any other car. Andy Tokley, chief engineer for the DBX, says the chassis layout of the refreshed model has been modestly redefined for better passenger comfort. There’s ample rear legroom, and fully adaptive shock absorbers, air suspension, and active roll bars deliver a smooth ride. But not too smooth. The tweaks to the DBX included exhaust note tuning so that passengers hear more of that distinctive V8 rumble, Tokley says.

The DBX could be seen as Aston Martin’s best bet for an electric drivetrain, although the company is actively working with American brand Lucid on EVs and plans are somewhat delayed. Aston was to have launched an EV in 2025 but chairman Lawrence Stroll recently told Autocar that “consumer demand is not what we thought it was two years ago.” Four EVs have reportedly been designed, but it will likely be at least 2026 before we see one of them.

The DBX group on the trail Jim Motavalli

Aston Martin’s portfolio includes accessible, almost mainstream, models like the DBX and exotics like the US$3 million Valkyrie supercar, of which 150 coupes and 85 Spyders have so far been built. Only 40 are left to be constructed. And in addition to the cars, well, there’s real estate. In the wake of Porsche and Bentley, the company developed the Aston Martin Residences in Miami, which had its grand opening in April.

By that time, 99% of the 391 luxury condominiums, located where the Miami River meets Biscayne Bay, had already been sold. But the US$59 million triplex penthouse with 27,191 square feet of living space is available, an Aston spokeswoman says. The 66-storey building is constantly reminding occupants of the Aston brand, whose cues adorn door handles, room number signs, and door tabs.

More property investors are seeking to buy in cheaper capital city markets amid high interest rates and inflationary pressures on holding costs such as insurance, repairs, utilities and strata levies. This is a key finding of Australian Property Investor (API) magazine’s Q1 2024 Sentiment Report, which canvassed the views of more than 600 Australians over the first three weeks of April.

The report also found that just three states are dominating investors’ interest, with 75 percent of survey respondents squarely focused on Queensland, Western Australia and New South Wales, which they say offer the best prospects for capital growth. Queensland is the favoured market, followed by Western Australia, which is soaring in popularity. Interest in Western Australia has doubled with 25 percent of respondents identifying it as the best growth market in 2024.

“Perth is not showing any signs of a slowdown, with population growth, housing supplyshortages and high rents driving the capital growth,” said Julie Kelley, Global Sales and Marketing Manager ataussieproperty.com.

“The east coast investor contingent isalso hungrily purchasing property at rates we haven’t seen since the mining boom of the2000s. Buyers recognise Perth is extremely affordable, offers high rental yields, sub-1 percentvacancy rates, has a strong economy, and the fastest housing value growth nationally.”

While Queensland and Western Australia offer relative affordability, investors remain interested in Australia’s most expensive market, New South Wales. It appears Sydney’s ongoing price growth is attracting wealthier investors who have the capacity to pay the highest median house and apartment prices in the country.

Interest rates, access to finance, affordability and rental yields are the four key elements influencing investors’ decisions this year,and likely contributing to the popularity of Queensland and Western Australia.With rents racing higher around the country, there is an opportunity in cheaper markets to purchase properties that are not only rising in value but are positively geared. This means the landlord receives rental income exceeding the costs of holding the property.

Meantime, it seems Victoria has lost its appeal among investors due to weak capital growth over the past year and a perception that government policy is weighted againstlandlords.Victoria has introduced higher land taxes, enhanced tenants’ rights, and is now considering new minimum energy efficiency standards which may require costly upgrades to insulation and appliances.

Mike Mortlock, Managing Director of MCG Quantity Surveyors, said based on investment loan data, Victoria was likely to lose more than a net 5,000 rental properties (or 1 percent of the state’s rental stock) over the next 12 months as investors sell up and new buyers look elsewhere.

“Landlords are increasingly cautious about entering the Victorian market,” Mr Mortlock said. “It’s not just about those who are leaving. Many potential investors are now avoiding Victoria altogether, seeking opportunities in other states with more favourable conditions.”

Despite high interest rates and inflation making investment holding costs such as insurance, strata levies and repairs higher, more than one in five survey respondents intend to buy an investment property over the next 12 months. This was the most popular investment goalat 22 percent, followed by positioning for retirement at 18 percent, reducing loan debts at 14 percent and benefitting from capital growth and passive income at 8 percent.

High interest rates remain the primary concern of investors. More than half of respondents saida single 25-basis point rate rise would alter their buying and selling intentions.

API says affordability constraints have driven more people to the unit market than ever before. However, 39 percent of survey respondents say they are targeting houses for investments, with 23 percent targeting units and 18 percent seeking to buy a townhouse. Investors are also preferring capital cities to regional areas, even though the regions are outperforming over the year to date.

It appears investors are thinking more strategically over the long term, given their preference for houses in capital cities. Houses typically record higher capital growth than apartments over the long term because of their land value, and capital cities tend to outperform over the long term, too.

More than eight in 10 respondents believe property prices overall will continue to increase. CoreLogic Research Director Tim Lawless says more price rises in most markets are likely due to a lack of stock for sale to meet the strong demand.

“Inventory levels in these markets remain well below average despite vendor activity lifting relative to this time last year,” he said. “Fresh listings are being absorbed rapidly by market demand, keeping stock levels low and upwards pressure on prices.”

Standout golfers who aren’t quite PGA Tour material now have somewhere else to play professionally: Corporate America.

People who can smash 300-yard drives and sink birdie putts are sought-after hires in finance, consulting, sales and other industries, recruiters say. In the hybrid work era, the business golf outing is back in a big way.

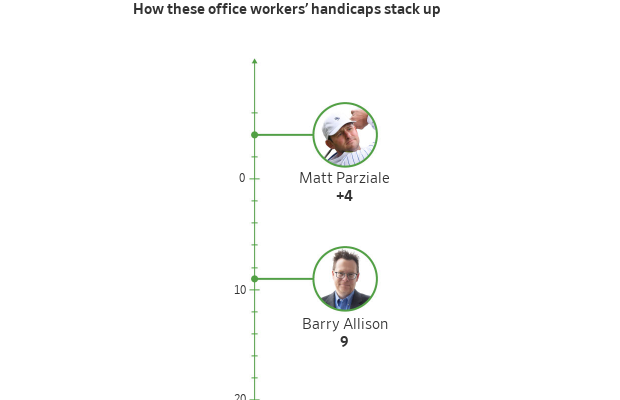

Executive recruiter Shawn Cole says he gets so many requests to find ace golfers that he records candidates’ handicaps, an index based on average number of strokes over par, in the information packets he submits to clients. Golf alone can’t get you a plum job, he says—but not playing could cost you one.

“I know a guy that literally flies around the world in a private jet loaded with French wine, and he golfs and lands hundred-million-dollar deals,” Cole says.

Tee times and networking sessions have long gone hand-in-golf-glove. Despite criticism that doing business on the course undermines diversity, equity and inclusion efforts—and the fact that golf clubs haven’t always been open to women and minorities —people who mix golf and work say the outings are one of the last reprieves from 30-minute calendar blocks

Stars like Tiger Woods and Michelle Wie West helped expand participation in the sport. Still, just 22% of golfers are nonwhite and 26% are women, according to the National Golf Foundation.

To lure more people, clubs have relaxed rules against mobile-phone use on the course, embracing white-collar professionals who want to entertain clients on the links without disconnecting from the office. It’s no longer taboo to check email from your cart or take a quick call at the halfway turn.

With so much other business conducted virtually, shaking hands on the green and schmoozing over clubhouse beers is now seen as making an extra effort, not slacking off.

Americans played a record 531 million rounds last year. Weekday play has nearly doubled since 2019, with much of the action during business hours , according to research by Stanford University economist Nicholas Bloom .

“It would’ve been scandalous in 2019 to be having multiple meetings a week on the golf course,” Bloom says. “In 2024, if you’re producing results, no one’s going to see anything wrong with it.”

A financial adviser at a major Wall Street bank who competes on the amateur circuit told me he completes 90% of his tasks by 10 a.m. because he manages long-term investment plans that change infrequently. The rest of his workday often involves golfing with clients and prospects. He’s a member of a private club with a multiyear waiting list, and people jump at the chance to join him on a course they normally can’t access.

There is an art to bringing in business this way. He never initiates shoptalk, telling his playing partners the round is about having fun and getting to know each other. They can’t resist asking about investment strategies by the back nine, he says.

Work hard, play hard

Matt Parziale golfed professionally on minor-league tours for several years, but when his dream of making the big time ended, he had to get a regular job. He became a firefighter, like his dad.

A few years later he won one of the biggest amateur tournaments in the country, earning spots in the 2018 Masters and U.S. Open, where he tied for first among non-pros.

The brush with celebrity brought introductions to business types that Parziale, 35 years old, says he wouldn’t have met otherwise. One connection led to a job with a large insurance broker. In 2022 he jumped to Deland, Gibson Insurance Associates in Wellesley, Mass., which recognised his golf game as a tool to help win large accounts.

He rescheduled our interview because he was hosting clients at a private club on Cape Cod, and squeezed me in the next morning, before teeing off with a business group in Newport, R.I.

A short time ago, Parziale couldn’t imagine making a living this way. Now he’s the norm in elite amateur golf circles.

“I look around at the guys at the events I play, and they all have these jobs ,” he says.

His boss, Chief Executive Chip Gibson, says Parziale is good at bringing in business because he puts as much effort into building relationships as honing his game. A golf outing is merely an opportunity to build trust that can eventually lead to a deal, and it’s a misconception that people who golf during work hours don’t work hard, he says.

Barry Allison’s single-digit handicap is an asset in his role as a management consultant at Accenture , where he specialises in travel and hospitality. He splits time between Washington, D.C., and The Villages, Fla., a golf mecca that boasts more than 50 courses.

It can be hard to get to know people in distributed work environments, he says. Go golfing and you’ll learn a lot about someone’s temperament—especially after a bad shot.

“If you see a guy snap a club over his knee, you don’t know what he’s going to snap next,” Allison says.

Special access

On a recent afternoon I was a lunch guest at Brae Burn Country Club, a private enclave outside Boston that was the site of U.S. Golf Association championships won by legends like Walter Hagen and Bobby Jones. I parked in the second lot because the first one was full—on a Wednesday.

My host was Cullen Onstott, managing director of the Onstott Group executive search firm and a former collegiate golfer at Fairfield University. He explained one reason companies prize excellent golfers is they can put well-practiced swings on autopilot and devote most of their attention to chitchat.

It’s hard to talk with potential customers about their needs and interests when you’re hunting for errant shots in the woods. It’s also challenging if you show off.

The first hole at Brae Burn is a 318-yard par 4 that slopes down, enabling big hitters like Onstott to reach the putting green in a single stroke. But to stay close to his playing partners and keep the conversation flowing, he sometimes hits a shorter shot.

Having an “in” at an exclusive club can make you a catch. Bo Burch, an executive recruiter in North Carolina, says clubs in his region tend to attract members according to their business sectors. One might be chock-full of real-estate investors while another has potential buyers of industrial manufacturing equipment.

Burch looks for candidates who are members of clubs that align with his clients’ industries, though he stresses that business acumen comes first when filling positions.

Tami McQueen, a former Division I tennis player and current chief marketing officer at Atlanta investment firm BIP Capital, signed up for private golf lessons this year. She had noticed colleagues were wearing polos with course logos and bringing their clubs to work. She wanted in.

McQueen joined business associates on the golf course for the first time in March at the PGA National Resort in Palm Beach Gardens, Fla. She has lowered her handicap to a respectable 26 and says her new skill lends a professional edge.

“To be able to say, ‘I can play with you and we can have those business meetings on the course’ definitely opens a lot more doors,” she says.

Glenhaven in Sydney’s Hills District is one of those areas that locals tend to keep to themselves. Leafy with large blocks on offer, the suburb takes its name from its valley location, with the northern end originally known as the Glen and the southern end called the Haven.

En route from Parramatta to the Hunter, Glenhaven has become an ideal place for growing families in search of a little more space, or even room to house several generations under one roof.

The challenge is finding properties that tick all the right boxes.

As demand for trades and supply chain issues continue to ease, now could be the right time for a knockdown/rebuild project for would-be buyers looking to create their dream home.

Fairmont Homes specialises in knockdown/rebuild projects in Sydney. General manager at Fairmont Homes, Daniel Logue, said there are key features to look for when choosing a knockdown/rebuild site.

“The key items we look for are the site falling to the street, not to the rear, to help with stormwater drainage as well as access to the site,” he said. “Neighbouring property front setbacks are also important. In some older areas, the older houses are set closer to the street, meaning your new home will have to be set to suit.

“Value for money and the return on the end sale price of the home is another issue.”

If possible, he said designing a home that meets the criteria of the Complying Development legislation will speed up approvals considerably.

While suitable knockdown/rebuild sites can be hard to find in Glenhaven, there are still hidden opportunities if you know where to look.

One block at 158 Gilbert Road, Glenhaven is ideally suited for rejuvenation. With almost 850sqm to play with, it slopes down to the street and sits between neighbouring properties that have already been stylishly updated.

An existing basketball court at the rear could provide the perfect teen backdrop to a family home, or it could make way for a larger house with landscaped gardens and pool. Alternatively, it could be the perfect position for a cabana or granny flat to serve as in-law accommodation or a source of secondary income.

With recent sales of completed homes in nearby streets reaching well above $5 million, it’s a great opportunity to make a slam dunk of a buy into one of Sydney’s best kept secrets.

Two female Apple employees filed a proposed class-action lawsuit Thursday alleging the company pays women lower salaries than men for similar work.

The suit, filed in a San Francisco state court, targets Apple’s hiring practices used to set compensation, as well as the company’s performance-review policies. It is the latest in a series of pay equity lawsuits against major corporations, including large tech giants, that allege they underpay women and minorities .

The lawsuit seeks to represent a class of 12,000 women employed at Apple across several departments who have worked there since 2020. The plaintiffs allege that the company is violating the California equal pay, employment and unfair business practice laws. The business practice law limits claims to a four-year period.

An Apple spokesman said the company has achieved and maintained gender pay equity since 2017. Apple works with an independent third-party expert to examine team members’ total compensation and makes adjustments where necessary, he said.

Google and Oracle settled similar claims in California in recent years, pushing similar arguments about pay policies for new hires. Google agreed to pay 15,500 women $118 million to settle its case in 2022 and Oracle agreed to pay $25 million for 4,000 female workers earlier this year. The companies didn’t admit wrongdoing.

One of the lead attorneys on those cases is also representing the plaintiffs against Apple.

Central to the new lawsuit is how Apple sets a new hire’s compensation. Before 2018, Apple asked applicants to provide their previous salaries to determine pay, the suit says.

When California passed a 2018 law that banned employers from considering prior pay to set compensation, Apple asked applicants about pay expectations instead, the suit says. The plaintiffs’ lawyers argue that the practice of asking about pay expectations perpetuates gender discrimination because women have historically been paid less than men.

“If you do pay women less, you can’t defend it by saying they were willing to take less money,” said James Finberg , one of the plaintiffs’ attorneys.

One of the plaintiffs, Justina Jong, said she discovered a male co-worker’s W2 left behind on a printer in Apple’s Sunnyvale, Calif., branch. Though she had the same responsibilities as her male co-worker, she saw his base salary in the tax filing was $10,000 more than what she made, she said. She discovered the discrepancy several years ago, about midway through her decade-plus career at Apple, where she held several roles in sales, training and marketing.

“I felt terrible and was shocked as well. I saw myself as a hardworking person, and collaborative, providing a lot of solutions for the team,” Jong said in an interview. “I thought to myself, ‘Maybe if I work harder, they will see that I’m worth just as much or more.’”

The lawsuit alleges that when Apple hired Jong in 2013, it paid her the same base salary she earned at her previous job. In the years following, the company never gave her the kind of raise that put her on equal footing with her male peers, the suit says.

Jong said it took her years to decide to challenge the discrepancy and sign onto the lawsuit. She said she was spurred by stories about unequal pay from other women at the company.

During the Covid-19 pandemic, Apple faced a rise in employee activism. Apple workers organized to form a group called Apple Too to mirror the #MeToo movement, which gathered stories of discrimination and pushed the company to change its pay practices. The movement led to some retail stores forming unions.

“At Apple we are deeply committed to inclusion and we have a longstanding commitment to pay equity, which is embedded in our approach to compensating our valued team members,” a spokesman for Apple said.

The other named plaintiff, Amina Salgado, has worked at Apple since 2012 in various roles, including as a manager in the AppleCare division in the company’s office near Sacramento. She discovered she was paid less than men in similar roles, and she complained several times about the discrepancy, according to the lawsuit. Apple hired a third party to investigate, and after the report concluded she was right, the company increased her pay. She didn’t get back pay, the lawsuit says.

The suit also claims that Apple uses biased criteria in its performance-review system. Men routinely receive higher ratings for the discretionary categories of leadership and teamwork, leading to better reviews for men, the plaintiffs’ lawyers argue.

Australia has a community of 4.2 million retirees, with another 710,000 intending to retire over the next five years and 226,000 of them planning to do so over the next two years, according to the Australian Bureau of Statistics (ABS).One of the biggest generations in Australia’s history – the baby boomers – is in the midst of its retirement years today. The baby boom began after WWII, with boomers beingborn between 1945 and 1964, making the youngest of this group 60 years old today.

The average age at which today’s workers intend to retireis 65.4 years. However, the long-term historical average is more than eight years earlier, with the average age at which existing retirees left the workforce being 56.9 years.People working in agriculture, forestry and fishing have the latest intended retirement age of68.3 years. This is followed by workers in property at 67.1 years and manufacturing at66.1 years.Workers in the mining sector have the earliest intended retirement age of 63.7 years, followed by workers in ITat 64 years and financial services at 64.3 years.

One factor that may be prompting people to retire earlier than planned is unforeseen circumstances, such as job loss, personal sickness or injury, or the need to provide care for someone else. Among existing retirees, an ABS survey found 13 percent retired because of sickness, injury or disability. Another 5 percent retired because they were retrenched, dismissed, or unable to find employment. Three percent retired to care for an ill, disabled or elderly person.

For 31 percent of retirees, gaining access to financial support was the main reason they retired. The age pension is the biggest source of income for most retirees today, followed by superannuation. The age at which baby boomers can receive the pension has increased over time from 65 to 67 years. However, they canaccess their superannuation earlier, once they reach preservation age.

Preservation ages vary depending on birth dates. Australians born before 1 July 1960 have a preservation age of 55 years. The preservation age increases by one year for every financial year from FY61 to FY64. For those born after 30 June 1964, the preservation age is 60 years. This means the youngest boomers will all gain access to their superannuation this year, which mayprompt them to retire. Otherwise, they have seven more years to wait for eligibility for the age pension at 67.

Bjorn Jarvis, ABS head of labour statistics said: “In 2022-23, a Government pension or allowance was still the main source of personal income at retirement for 43 percent of retirees. This was followed by Superannuation, an annuity or private pension at 27 percent.”The full age pension is currently $43,752.80 per annum for couples and $29,023.80 for singles.The average superannuation balance for Australians aged 60 to 64 years is just over $360,000, according to the latest tax office data.

The impact of one of our largest generations retiring is reflected in surging superannuation payouts. New figures from the Australian Prudential Regulation Authority show an 18.1% increase inpayouts over the 12 months to 31 March. The payouts, taken as lump sums or pension streams,totalled $112.9 billion.

Halfway through the building process of Kyle Loucks’s new five-bedroom, 5,800-square-foot house in Vancouver, Wash., his wife decided she wanted to add a sports court.

At first he panicked. “One seemingly small decision, like ‘let’s put a hoop here,’ has a ripple effect,” says Loucks, 37, a former Meta engineer who founded a joint-rolling technology company called RollPros.

Using new AI software called Digs on his laptop, he put a box into the house plans, first in the backyard. Then, seeing that it wouldn’t fit well, he moved it to the driveway. Within minutes, his contractor, notified by Digs of the change, confirmed that the dimensions would work and messaged the concrete guys to let them know before they did the pour and to see if they had any input on holes for a pickleball net. The landscape designer weighed in, suggesting a couple of trees nearby to help it blend in, and the lighting subcontractor advised them on how a flood light would affect the high-voltage plan.

Kyle Loucks is using AI software called Digs to look at the architectural renderings of his new home. PHOTO: AMIE SANTAVICCA FOR THE WALL STREET JOURNAL

“It helped bypass the possibility of human error and miscommunication,” says Loucks, whose home is slated to cost around $2.2 million and to be finished in October.

Homeowners are experimenting with an explosion of new artificial intelligence applications to quickly visualise an array of layout and style ideas, coordinate with builders and designers and estimate costs. These new tools say they can help save time and money in the building and renovation process, which has traditionally been filled with seemingly endless decisions and an avalanche of paperwork that often result in longer projects and ballooning costs.

There are now dozens of AI apps related to home construction, design and renovation—most of which have sprung up in the past two years.

“There seems to be a new one every day,” says Patrick O’Toole , publisher of Qualified Remodeler, which did a survey in March 2023 of its 83,000 readers and found that about half have tried generative AI tools.

Some apps, like Renovate AI, focus on visualisation. Users can generate images to see how different design ideas might look by uploading photos or drawings of their rooms. Then they can choose styles like “rustic farmhouse” or tell the tool to adjust specific elements like paint colors, lighting, furniture or the style of the cabinets.

Other platforms, like Digs, use AI to create 3-D “dollhouse” floor plans and manage the logistics of a project, room by room. Digs can layer in the location of specs like the load-bearing beams, plumbing lines and lighting plans to show where walls can be knocked down, and users can query it to get the make and model of an appliance or the dimensions of the wall, all sourced from the original documents.

Analysts say the demand for new tools is driven in part by the state of the housing market. The decline in construction of new houses, combined with a rapid run-up in interest rates over the past two years that sent mortgage rates soaring, has resulted in many people choosing to stay and fix or add on to homes they already own. Spending on DIY projects soared 44% from 2019 to 2021, the latest stats available, according to Harvard’s Joint Center for Housing Studies.

The new apps offer homeowners a way of gaining control over what can be a dizzyingly complicated and opaque process, though not without their own risks.

Jess Sandlin asked ChatGPT to generate an image of a modern living room with a black fireplace and a large brass mantle, but she couldn’t get the app to give her a brass mantle. ILLUSTRATION: DALL·E 3/OPENAI

Jess Sandlin, 38, is working with an architect and designer to renovate a 9,000-square-foot home she and her boyfriend bought in Austin, Texas, for $2.5 million. But she is also using an app called Remodel AI as well as ChatGPT to help her get a sense of the possibilities and to empower her with images she can show since her vocabulary doesn’t include technical architectural terms.

“I wanted to get a sense of my own style and be a little more knowledgeable so I didn’t just get their style,” says Sandlin, executive director of Word Playground, a nonprofit for teaching children literacy.

As she tested out different prompts to home in on her own design sensibilities, Remodel AI generated hundreds of options—including some with furniture on the ceiling and the walls. She wanted an indoor play area for her four sons, aged 5 through 13, to include multiple layers of hammocks, a zip line and netting. The app couldn’t handle it. “It had no idea what I was talking about. It could not compute,” she says.

Dirk Morris, founder and CEO Reimage AI, the maker of the Remodel AI app, which costs $10 a month or $50 a year, says Sandlin may have been using the wrong tool: Sometimes people try to use the standard interior remodel tool to make extensive structural changes, he says.

Even when Sandlin was able to generate exactly what she wanted, she ran into human roadblocks. When she showed her architect AI-generated photos of a bronze fireplace with a brass mantle, “they rolled their eyes at me,” she says. Eventually, her designer agreed to the bronze.

While traditionally AI tools were aimed at professionals, the newer apps are letting laypeople in on the game, says Michael Anschel , a principal at Minneapolis-based OA Design and Build Architecture.

Jess Sandlin is shown here with her four sons. PHOTO: ALLIE LEEPSON + JESSE MCCLARY FOR THE WALL STREET JOURNAL

However, he says the tools aren’t sharp enough yet. For example, when Anschel asked Renovate AI to generate a kitchen with hand-scraped stone counters and paisley wallpaper, he got an image with stainless steel counters and paisley wallpaper on the cabinets and the ceiling.

Other pros have expressed concern about having to address design ideas that might not be possible from clients armed with AI-generated images. “It could be extremely annoying,” says Daniel Kaven of Portland, Ore.-based William Kaven Architecture.

Laura Bindloss, 38, who owns a social media and public relations agency, has renovated several homes, but she had never used AI to help until her most recent project: a 2,000-square-foot house she bought in March for $575,000 in Bellport, N.Y. Bindloss, who plans to live in the house on weekends as well as rent it out, was looking to spend a total of around $200,000, with $55,000 on the kitchen alone. She wanted to get the project done quickly so she could start renting it out this summer.

“I’d heard about it as a visualisation tool but it didn’t seem that useful,” she says. When she hired cabinetmaker Isla Porter to design the kitchen, she found that the company was using AI provider Skipp, which can make a scan from a phone into detailed renovation plans, complete with renderings, materials lists and construction-ready documents. The first step was to take a 3-D scan of the space with her iPad. She then answered a 40-question survey, with questions like “where do most meals happen” and “what do you like most and least about your current kitchen.”

The AI used her scan and survey responses to generate hundreds of floor plan options within minutes. Isla Porter’s designers then manually edited them, significantly reducing the time it would have taken if the designers had to go through the survey results without the technology, says Sharon Dranko, Isla Porter’s founder. Bindloss then picked from the three options Isla Porter recommended, choosing materials and finishes in the program to see how everything would look. The design plans for the kitchen were finalized in two weeks, says Bindloss.

Dranko says that even though the AI’s measurements tend to be 98% accurate, it’s still crucial to have a human designer double check everything. AI is also off sometimes when it comes to understanding living patterns, meaning how the way a person uses their kitchen should impact the design, she says. Dranko says she is constantly feeding it new information like colors and fabrics to make it more useful when it comes to finding the right style and look for her clients.

The idea of using AI in his home renovations came to Kade Boverhof when he was looking at possible floor plans for the renovation of a 1,900-square-foot house he bought in Grand Rapids, Mich., for $150,000.

Boverhof, 31, wanted to create a floor plan for the house that took into account all the iterations he’d devised in previous renovation projects using a computer-aided design (CAD) software program. There must be an AI program that could do this, he thought.

After searching Google and going on Reddit to ask others what they were using, Boverhof came across an app in development called A-Space, which let him use its tools for free as an early adopter in exchange for his feedback. He downloaded his existing blueprints, which included information on the location of walls that were necessary to hold up the structure, added some instructions and hit generate. From the four options, Boverhof locked in the kitchen location he liked best and again pushed the generate button to see the options for the other rooms around that decision.

Boverhof says the results weren’t perfect. It didn’t know the local building codes for the city of Grand Rapids, such as the percentage of space required to be windows or doors. But he says he saved many hours and got back new layout ideas that he could tailor.

“It’s at a primitive stage, but the possibilities are there,” he says.

Ryan Fink, CEO and co-founder of Digs, says that of the some 6,000 homes currently on its platform, half have homeowners participating. Builders currently pay $69 per user per month, but the contractors, vendors and homeowners involved in the projects participate for free, he says.

Sid Sarasvati founded Renovate AI because of the difficulties he encountered with staging homes for sale. He says the app will continue to improve, such as offering users the option to click on products to buy online, create budgets and connect with vendors. Launched in January 2023, it has some 15,000 subscribers now, 40% of whom are on a $10-a-week plan and 60% of whom are on a $40 annual plan.

Many of the AI apps are aimed at improving the speed and communication for homeowners working with an architect or designer. But some, including A-Space, hope to democratise the process and reduce the need for architects by automating tasks like filling in planning applications.

“We want to give every person access to architectural expertise,” says Ziyad Mourad, CEO and co-founder of A-Space, which plans on offering the app free to homeowners for a single project and for $50 a month to architects for unlimited use.

WSJ Tests an AI Remodelling Tool

Rashad Fakhouri, an architect at London-based Pilbrow & Partners, who is currently using A-Space on the side but not for work projects, says he doesn’t foresee a time when AI will replace architects because of the need for the architect’s aesthetics and their ability to troubleshoot throughout the process.

“We will still be necessary,” he says.

In five years, AI tools for home remodelling and construction will become more integrated, says Jose Luis Blanco, senior partner at McKinsey who leads the firm’s engineering and construction work in North America. “We are in the early innings,” he says.

Mike Rowe, of “Dirty Jobs” TV fame and a spokesman for AI provider Digs, agrees that the continued expansion of AI will democratise the home-building process. “It will put a lot more power in the consumers’ hands,” he says.

Some homeowners say the tools are already offering a newfound leg up in managing their projects with the pros.

It’s either the stuff of nightmares—or a normal, everyday part of life. Financial advisors who cater to wealthy clients say a loan to another family member can be the answer to a lot of problems, but caution that they can raise just as many issues as they aim to solve.

“When money’s involved, family isn’t always family. Sometimes money trumps family,” says Jon Ekoniak, a partner at Bordeaux Wealth Advisors, based in Silicon Valley.

Loans between family members—usually, but not always, from an older person to their children or grandchildren—may be best ventured with the help of financial advisors who have experience setting them up. Professional guidance can make the situation more comfortable for family members unaccustomed to transacting business with each other. It’s also safer, as intra-family loans may have implications ranging from taxes to legal issues.

Ekoniak describes one example of parents with a grown daughter who’d married someone who “bounced” from job to job. The young couple wanted to have children, but could only afford a small rental apartment. After nearly a year of agonising over different ways to help the couple, the parents finally decided to simply offer them a loan to buy a house.

“They set up a trust fund and 50% of the income from the trust would be used to pay back the loan,” Ekoniak says. The loan repayments were interest only, at the government’s prevailing “applicable federal rate,” which is the lowest rate the IRS allows for private loans.

It seems straightforward—the “Bank of Mom and Dad” has long been a normal part of young adulthood in America, after all. But there are plenty of possible pitfalls to keep in mind.